If you own a free standing home in Svensson Heights, QLD 4670, you're likely no stranger to the challenge of finding affordable home insurance. This leafy suburb in the Bundaberg region sits in a part of Queensland where property characteristics, local weather history, and building age can all push premiums in unexpected directions. In this article, we analyse a real home and contents insurance quote for a 3-bedroom, 2-bathroom free standing home in Svensson Heights — and put the numbers in context so you can decide whether your own policy is working hard enough for you.

---

Is This Quote Fair?

The quote in question comes in at $3,042 per year (or $292/month) for combined home and contents cover, with a building sum insured of $534,000 and contents valued at $92,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — above average for the suburb.

To understand why, it helps to look at what other homeowners in Svensson Heights are paying. The suburb average premium sits at $1,940/yr, with a median of $1,852/yr. This quote lands well above both figures — and even clears the 75th percentile of $2,551/yr, meaning it's more expensive than roughly three-quarters of quotes collected in the area.

That said, "expensive" doesn't automatically mean "wrong." A higher sum insured, older construction, elevated stumped foundations, and specific building materials all contribute to a higher assessed risk — and therefore a higher premium. The key question is whether the coverage reflects the property's genuine replacement value, and whether there's room to shop around for a better rate.

---

How Svensson Heights Compares

Zooming out gives a useful perspective on where this quote sits in the broader market.

| Benchmark | Premium |

|---|---|

| This quote | $3,042/yr |

| Svensson Heights average | $1,940/yr |

| Svensson Heights median | $1,852/yr |

| Svensson Heights 75th percentile | $2,551/yr |

| QLD state median | $3,903/yr |

| National median | $2,764/yr |

A few things stand out here. While this quote is above average locally, it actually sits below the Queensland state median of $3,903/yr — a reminder of just how expensive home insurance has become across Queensland as a whole. The QLD state average is a staggering $9,129/yr, heavily skewed by high-risk cyclone and flood zones in North Queensland.

Compared to the national median of $2,764/yr, this quote is modestly above average — roughly 10% higher. For a property with a $534,000 building sum insured, that's not an outrageous figure, but it does suggest there may be room to negotiate or switch providers.

It's also worth noting that the suburb sample size here is 19 quotes, which is a reasonably small dataset. Local averages can shift meaningfully as more data comes in, so treat suburb benchmarks as a useful guide rather than an exact science.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium — some pushing it higher, others potentially keeping it in check.

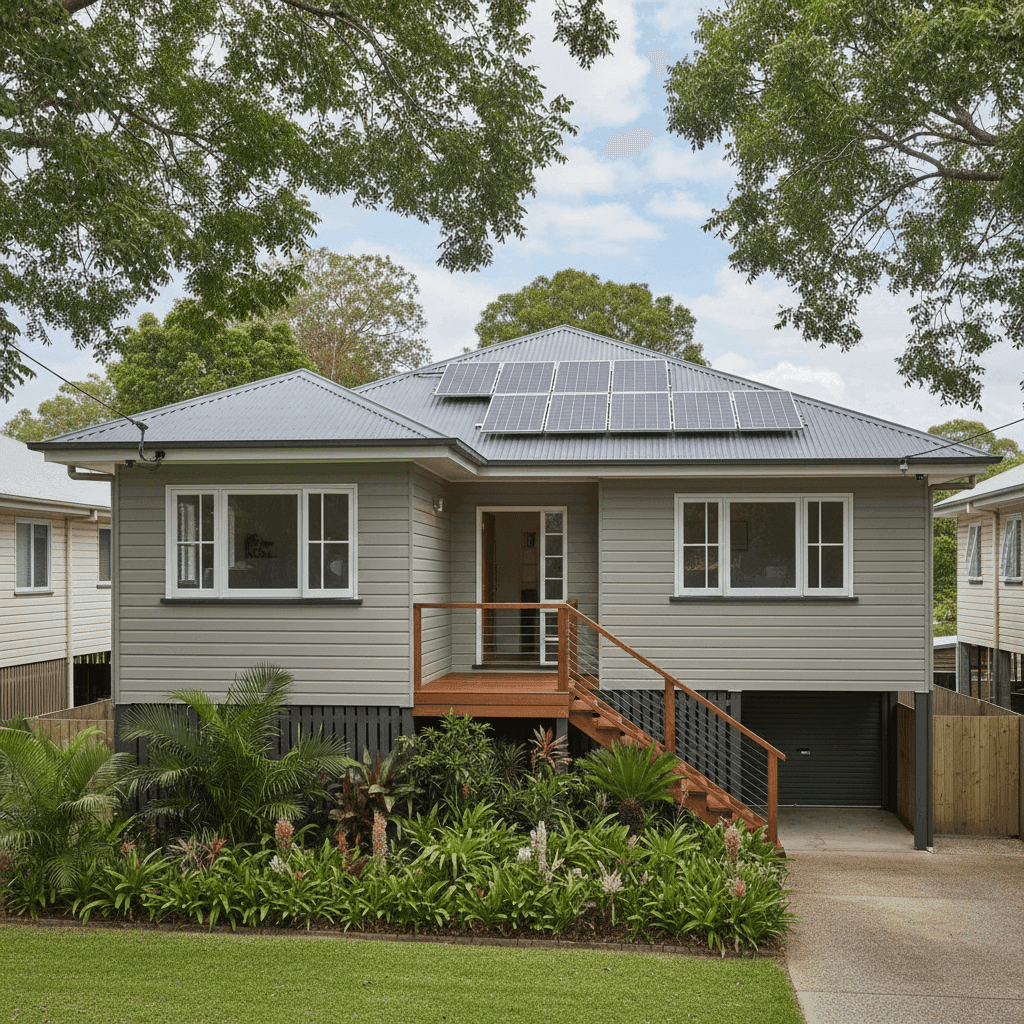

Age of Construction (1960)

At over 60 years old, this home falls into a category that many insurers treat with caution. Older homes can have ageing plumbing, wiring, and structural elements that increase the likelihood of a claim. Insurers often apply loadings to pre-1980s properties, particularly in Queensland where building standards have evolved significantly since then.

Hardiplank/Hardiflex Exterior Walls

Fibre cement cladding like Hardiplank is generally viewed favourably by insurers — it's durable, fire-resistant, and low-maintenance compared to weatherboard or brick veneer. This material choice may actually be working in the homeowner's favour from a risk-assessment perspective.

Steel/Colorbond Roof

Colorbond roofing is widely regarded as one of the more insurer-friendly roof types in Australia. It's resistant to fire, pests, and general weathering, and tends to have a long lifespan. This is a positive factor for the premium.

Elevated on Stumps (at Least 1m)

This is a classic Queenslander-style feature — and it cuts both ways. On one hand, elevation can reduce flood risk by keeping the living areas above ground level. On the other hand, stumped foundations introduce their own risks (subfloor access, potential for movement, pest ingress), and elevated homes can be more vulnerable to wind damage. Insurers weigh these factors carefully.

Timber and Laminate Flooring

Timber floors in an older elevated home can be a cost driver at claims time — replacement and repair costs for hardwood or quality laminate flooring are not insignificant. This may be a contributing factor to the building sum insured of $534,000.

Solar Panels

The property has solar panels installed. These add replacement value to the building sum insured and can also introduce electrical risk. Most insurers cover solar panels under building cover, but it's worth confirming this is included — and that the sum insured accounts for their replacement cost.

Ducted Climate Control

Ducted air conditioning systems are expensive to replace and can be a source of water damage claims if not properly maintained. Their presence adds to the overall insured value of the home.

---

Tips for Homeowners in Svensson Heights

1. Review your sum insured carefully A building sum insured of $534,000 for a 169 sqm home built in 1960 is substantial. Make sure this figure reflects the actual cost to rebuild — not the market value of the property. Overcovering can inflate your premium unnecessarily, while undercovering leaves you exposed. Use a building cost calculator or speak to a local builder to get a realistic estimate.

2. Compare at least three quotes before renewing The gap between the cheapest and most expensive quotes in Svensson Heights spans from around $1,281/yr (25th percentile) to over $2,551/yr (75th percentile). That's a significant range. Spending 20 minutes comparing quotes at CoverClub could save you hundreds of dollars annually.

3. Ask about discounts for security and maintenance Some insurers offer premium reductions for homes with monitored security systems, smoke alarms, or documented maintenance records. For an older home on stumps, demonstrating that the subfloor and structure are in good condition may also support a more favourable assessment.

4. Check your solar panel and ducted AC coverage Confirm with your insurer that both the solar system and ducted climate control are explicitly covered under your building policy — and that the sum insured is sufficient to replace them at today's prices. Solar panel replacement costs have changed significantly in recent years, and it's easy for coverage to fall out of step with current market rates.

---

Ready to Find a Better Rate?

Whether you're renewing soon or just curious about what else is out there, comparing quotes is the fastest way to know if you're getting value. At CoverClub, you can see real quotes for properties like yours in Svensson Heights — and make an informed decision rather than simply rolling over your existing policy. It takes just a few minutes, and the savings can be well worth it.