If you own a free standing home in Taggerty, VIC 3714, you already know this picturesque Upper Yarra Valley town comes with its own unique set of insurance considerations. Nestled in the Murrindindi Shire, Taggerty is surrounded by stunning bushland — but that natural beauty also brings elevated risk factors that insurers take seriously. In this article, we break down a real home and contents insurance quote for a 3-bedroom property in the area, compare it against local, state, and national benchmarks, and share practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question sits at $4,782 per year (or $458/month) for a combined home and contents policy, covering a building sum insured of $801,000 and contents valued at $135,000. Both the building and contents excess are set at $1,000.

Our rating for this quote is FAIR — Around Average, and when you dig into the numbers, that assessment holds up well.

The suburb average for Taggerty sits at $5,706/year, with a median of $6,036/year. This quote comes in roughly $924 below the suburb average and over $1,250 below the local median — a meaningful saving. It also falls comfortably within the 25th–75th percentile range of $4,463 to $6,783, placing it solidly in the middle of the market rather than at either extreme.

So while "fair" might sound underwhelming, in the context of Taggerty's local insurance market, this quote is actually performing better than most. The property owner is not overpaying relative to their neighbours, and there's a reasonable spread of cover in place.

---

How Taggerty Compares

To put this quote in proper context, it helps to zoom out and look at the broader picture.

| Benchmark | Premium |

|---|---|

| This Quote | $4,782/yr |

| Taggerty Suburb Average | $5,706/yr |

| Taggerty Suburb Median | $6,036/yr |

| Murrindindi LGA Average | $4,184/yr |

| VIC State Average | $3,000/yr |

| VIC State Median | $2,718/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. First, Taggerty premiums are significantly higher than the Victorian state average of $3,000/year — nearly double, in fact. This reflects the region's bushfire exposure and the higher rebuild costs associated with rural properties. Second, this quote is actually below the national average of $5,347/year, which is a positive sign given the property's location and features.

The VIC state stats show that metropolitan and lower-risk Victorian properties pull the state average down considerably. Rural and bushfire-prone areas like Taggerty naturally attract higher premiums. When compared to national data, the quote looks quite reasonable — particularly given the $801,000 building sum insured, which is on the higher end.

It's also worth noting the Murrindindi LGA average of $4,184/year. This quote is slightly above that LGA benchmark, which likely reflects the specific features of this property — more on that below.

---

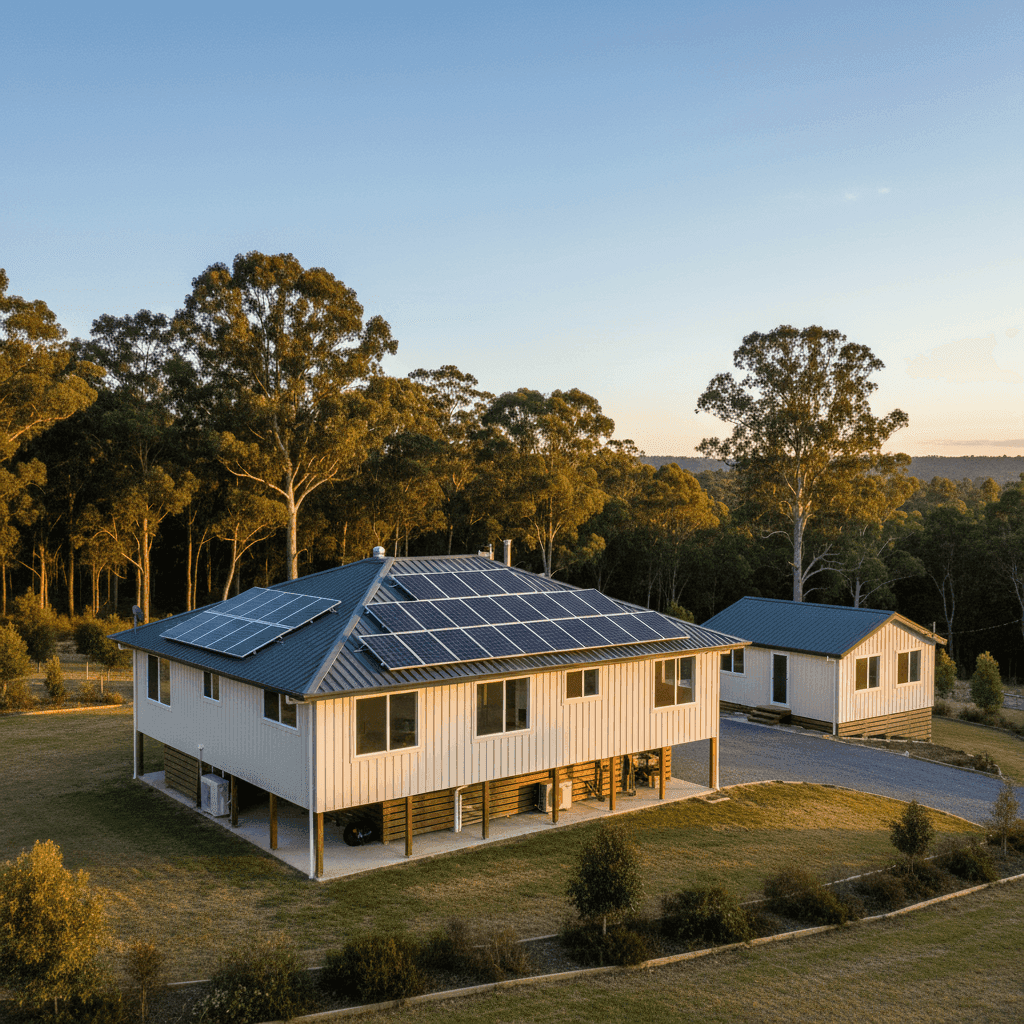

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium, both positively and negatively.

Features That May Increase the Premium

- Location in Taggerty, Murrindindi Shire: This region has a well-documented bushfire risk history, including the devastating 2009 Black Saturday fires. Insurers price this risk accordingly, and it's the single biggest driver of elevated premiums in this area.

- Elevated on stumps: While a stump foundation is common in regional Victoria and offers practical advantages, it can be associated with slightly higher rebuild complexity and exposure to certain weather events.

- Timber and laminate flooring: Natural timber flooring is a fire risk consideration and can also be more costly to replace than tiles or carpet, contributing to higher contents and building valuations.

- Above average fittings quality: Higher-quality fixtures and finishes increase the cost to rebuild or repair, which is reflected in the $801,000 sum insured and the premium.

- Granny flat on the property: An additional dwelling adds to the overall replacement value and insurable risk, which insurers factor into their pricing.

- Solar panels and ducted climate control: These are valuable inclusions that add to the replacement cost of the home. Solar systems in particular can be expensive to replace and are increasingly being priced into building sums insured.

Features That May Help Keep the Premium Down

- Hardiplank/Hardiflex external walls: This fibre cement cladding is considered more fire-resistant than traditional timber weatherboard, which can work in your favour with some insurers when assessing bushfire risk.

- Steel/Colorbond roof: Metal roofing is generally viewed favourably by insurers — it's durable, fire-resistant, and less prone to storm damage than tiles.

- Built in 2023: A newly constructed home benefits from modern building codes, which include improved fire safety standards, structural resilience, and energy efficiency. Newer homes typically attract lower premiums than older, potentially deteriorating properties.

- No pool: Swimming pools can introduce liability risks and add to the insurable value of a property, so not having one simplifies the risk profile.

- No cyclone risk area: Taggerty is not in a designated cyclone zone, removing one category of risk that can significantly inflate premiums in northern parts of Australia.

---

Tips for Homeowners in Taggerty

1. Review Your Bushfire Preparedness Annually

Some insurers offer discounts or more favourable terms when you can demonstrate active bushfire mitigation — such as maintaining a cleared defendable space, installing ember guards, and having a written bushfire survival plan. Check with your insurer whether these measures are recognised in your policy terms.

2. Make Sure Your Building Sum Insured Reflects Current Rebuild Costs

Construction costs have risen sharply in recent years. A $801,000 sum insured may be appropriate now, but it's worth reassessing each year using an independent building cost estimator. Being underinsured in a high-risk area like Taggerty can have devastating consequences if you ever need to make a major claim.

3. Bundle Your Home and Contents Cover

This quote already combines home and contents, which is often the most cost-effective approach. If you're currently holding separate policies with different providers, consolidating them could reduce your total outlay and simplify the claims process.

4. Compare Quotes at Renewal — Every Year

Insurance pricing changes constantly, and loyalty doesn't always pay. With a suburb median of $6,036/year, there's clearly a wide spread of premiums in Taggerty. Shopping around at renewal could save you hundreds of dollars without sacrificing cover quality.

---

Compare Your Own Quote

Whether you're a new homeowner in Taggerty or coming up for renewal, it pays to know where your premium sits relative to the market. CoverClub makes it easy to compare home and contents insurance quotes from a range of Australian insurers — all in one place. Get a quote today and find out if you could be paying less for the same level of protection. You can also explore detailed Taggerty insurance data to benchmark your own policy.