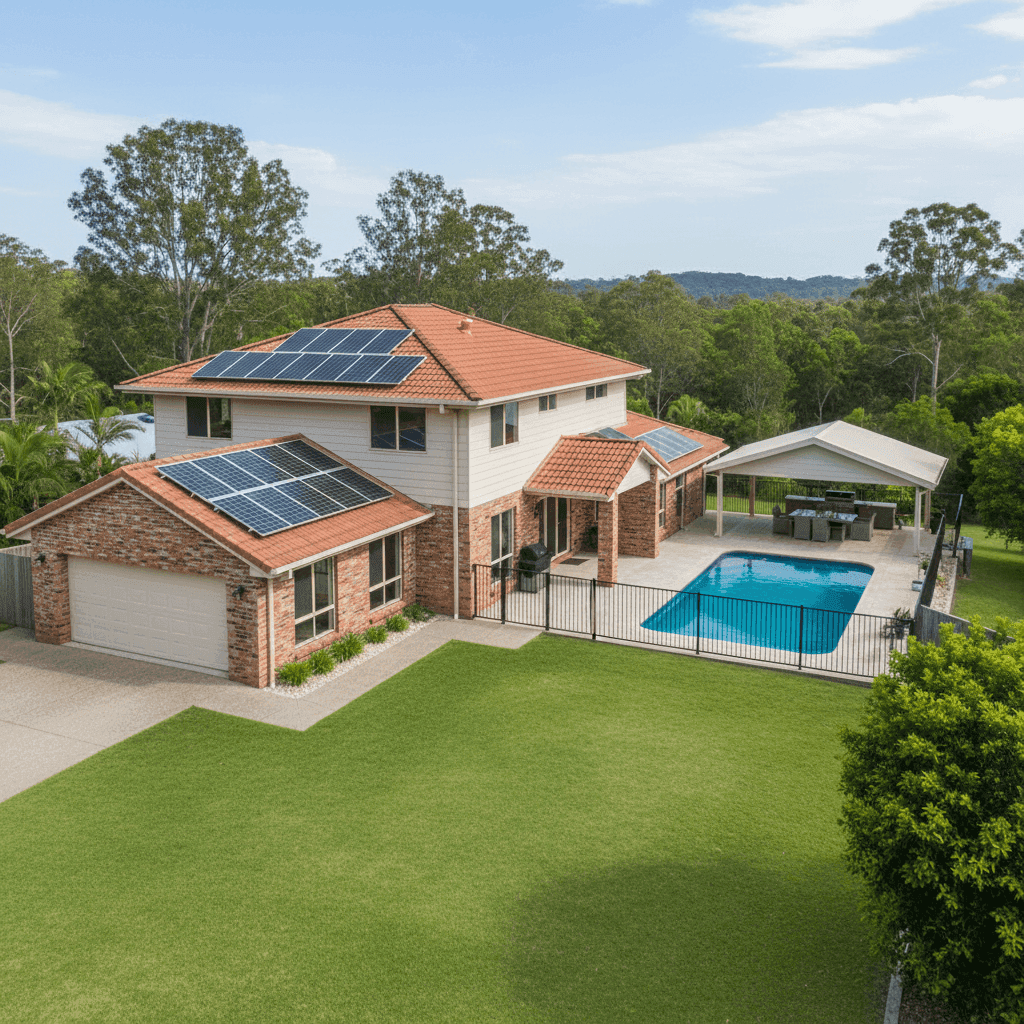

Tallai is a quiet, leafy suburb nestled in the hinterland of the Gold Coast, known for its acreage properties, elevated terrain, and relaxed semi-rural lifestyle. If you own a free standing home in this sought-after pocket of Queensland, understanding what you should be paying for home and contents insurance — and why — is an important part of protecting one of your most significant assets. This article breaks down a real insurance quote for a four-bedroom, three-bathroom home in Tallai, and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $3,061 per year (or $293 per month) for combined home and contents cover, with a building sum insured of $741,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Based on CoverClub's pricing data, this quote is rated CHEAP — sitting below the average for the Tallai area. That's a meaningful result. In a suburb where premiums can vary enormously depending on the insurer, the property's characteristics, and the level of cover selected, landing below the local average is a genuine win for the homeowner.

To put it plainly: this quote is well below what many comparable properties in the same postcode are paying, and it's significantly under the broader Gold Coast LGA average of $8,161 per year. For a property with a solid rebuild value and a reasonable contents sum, that's an encouraging sign that the right insurer has been matched to the right risk profile.

---

How Tallai Compares

Tallai sits within postcode 4213, and local insurance data for this suburb tells an interesting story. Based on a sample of 36 quotes collected for this area:

| Benchmark | Premium |

|---|---|

| This Quote | $3,061/yr |

| Suburb 25th Percentile | $4,777/yr |

| Suburb Median | $5,305/yr |

| Suburb Average | $6,447/yr |

| Suburb 75th Percentile | $7,793/yr |

This quote doesn't just beat the suburb median — it comes in $1,716 below the 25th percentile, meaning it's cheaper than at least 75% of quotes collected in the area. That's a standout result.

Zooming out to the state level, Queensland home insurance premiums reflect the significant risk diversity across the state. The QLD average sits at a hefty $9,129 per year, driven upward by high-risk cyclone and flood zones in North Queensland. The state median is a more moderate $3,903 per year — and this quote still comes in comfortably below that figure.

At the national level, the average Australian home insurance premium is $5,347 per year, with a national median of $2,764. This quote lands between the national median and average, which is a reasonable position for a well-appointed four-bedroom home with a pool and solar panels in a desirable Queensland suburb.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence how insurers assess and price the risk. Here's what's at play:

Construction (Brick Veneer, Tiled Roof, Slab Foundation)

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability, which can help moderate premiums compared to timber-framed or clad homes. A tiled roof similarly signals longevity and lower vulnerability to storm damage than corrugated iron in many scenarios. A concrete slab foundation is a stable base that reduces the risk of subsidence-related claims.

Age of the Property (Built 1987)

At approximately 38 years old, this home is well past the high-risk new-build phase but also old enough that insurers may factor in the potential for ageing plumbing, wiring, or roofing components. Keeping these systems well-maintained and up to current standards is important both for claim outcomes and for keeping premiums competitive.

Swimming Pool

A pool adds to the replacement cost of the property and introduces some liability considerations. It's reflected in the sum insured and can nudge premiums slightly higher, though its impact here appears modest given the overall competitive pricing achieved.

Solar Panels

Solar panels are increasingly common on Australian homes, and most insurers now include them as part of standard building cover — but it's worth confirming this with your insurer. Panels add to the rebuild value and can be expensive to replace, so ensuring they're adequately covered under the building sum insured is essential.

Ducted Climate Control

Ducted air conditioning is a high-value fixed asset that forms part of the building sum insured. At 214 sqm, this is a well-sized home, and the inclusion of ducted climate control is consistent with the $741,000 building sum insured — a figure that should reflect full replacement cost, not market value.

No Cyclone Risk

Tallai is not classified as a cyclone risk area, which is a meaningful factor in keeping this premium competitive. Properties in North Queensland can face cyclone-related loadings that push premiums dramatically higher. Tallai's hinterland location spares homeowners from this particular cost driver.

---

Tips for Homeowners in Tallai

Whether you're reviewing an existing policy or shopping for new cover, here are four practical steps worth taking:

- Review your sum insured annually. Building costs in Queensland have risen sharply in recent years due to labour shortages and material price increases. A sum insured that was adequate three years ago may no longer cover a full rebuild. Use a building cost calculator or speak with a quantity surveyor to sense-check your figure.

- Confirm solar panels and pool equipment are covered. Ask your insurer specifically whether solar panels, inverters, and pool pumps or heating systems are included under your building policy — and up to what limit. These items can be costly to replace and are sometimes subject to sub-limits.

- Consider your excess carefully. A $1,000 excess is fairly standard, but opting for a higher voluntary excess can reduce your annual premium. Conversely, if cash flow is a concern, a lower excess means less out-of-pocket cost at claim time. Find the balance that suits your financial situation.

- Don't auto-renew without comparing. Insurers frequently increase premiums at renewal, sometimes significantly. Given that this quote is already well below the local average, it's worth benchmarking your renewal premium each year to ensure you're still getting a competitive rate. Compare home insurance quotes at CoverClub to see what else is available for your property.

---

Get a Quote for Your Tallai Home

If you own a home in Tallai or anywhere across the Gold Coast region, it pays to compare. The spread of premiums in postcode 4213 is wide — from under $3,000 to nearly $8,000 per year for broadly similar properties — which means the insurer you choose matters enormously. CoverClub makes it easy to see what multiple insurers would charge for your specific property. Get a home insurance quote today and find out whether you're paying a fair price — or more than you need to.