Tallai is a leafy, semi-rural suburb tucked into the hinterland of the Gold Coast, known for its generous block sizes, elevated terrain, and high-quality residential properties. If you own a large free standing home in this pocket of Queensland, understanding what you should be paying for home and contents insurance — and why — can save you hundreds of dollars a year. In this article, we analyse a real insurance quote for a five-bedroom property in Tallai (QLD 4213) and put it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $6,088 per year (or $583/month) for combined home and contents cover, with a building sum insured of $1,500,000 and contents valued at $95,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up.

When compared against other quotes in the Tallai area, the $6,088 annual premium sits comfortably between the suburb's 25th percentile ($4,777/yr) and 75th percentile ($7,793/yr). It's slightly below the suburb average of $6,447/yr and a touch above the suburb median of $5,305/yr — placing it squarely in the middle of the pack for this postcode.

That said, "fair" doesn't necessarily mean "the best available." Given the high building sum insured ($1.5M) and the range of premium-influencing features on this property, there may still be room to shop around. A quote that's average for the suburb could still be beaten by switching insurers or adjusting your cover settings.

---

How Tallai Compares

To truly understand whether this premium represents good value, it helps to zoom out and look at the broader picture.

| Benchmark | Premium |

|---|---|

| This quote | $6,088/yr |

| Tallai suburb average | $6,447/yr |

| Tallai suburb median | $5,305/yr |

| Gold Coast LGA average | $8,161/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, the Queensland state average of $9,129/yr is notably high — largely driven by cyclone-prone regions in Far North Queensland, where premiums can be extreme. Since Tallai is not in a cyclone risk area, homeowners here benefit from significantly lower base rates than many other parts of the state.

Second, the Gold Coast LGA average of $8,161/yr is well above this quote, suggesting that properties elsewhere on the Gold Coast — particularly those closer to the coast with flood, storm surge, or cyclone exposure — attract considerably steeper premiums.

Compared to the national average of $5,347/yr, this quote is modestly higher, which is expected given the size and value of the property. A 286 sqm home with a $1.5M building sum insured is well above the typical Australian dwelling, so paying above the national average is entirely reasonable.

Based on a sample of 36 quotes in the Tallai area, this premium is a solid, mid-range result. Explore the full Tallai suburb insurance stats to see how your property compares in more detail.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the insurance premium. Here's how each one plays a role:

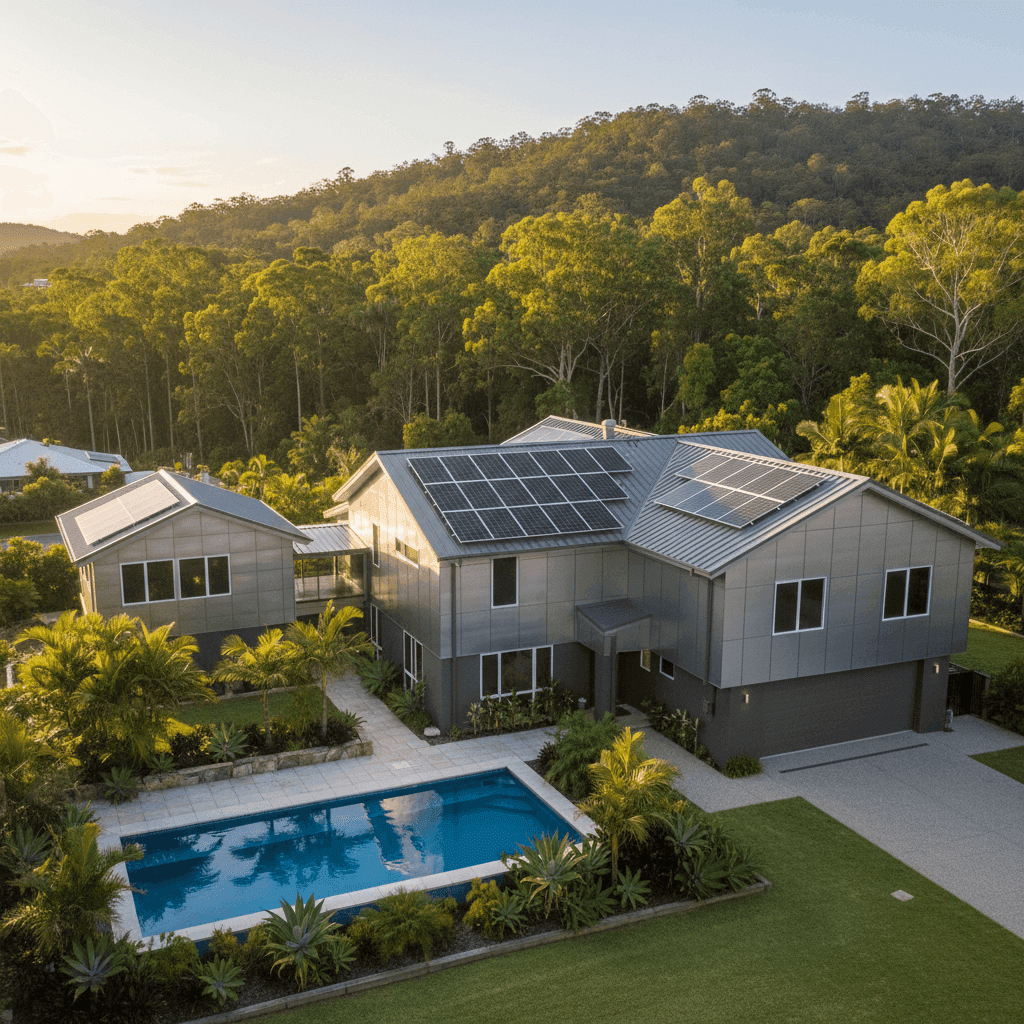

Size and bedrooms: At 286 sqm with five bedrooms and four bathrooms, this is a substantial home. Larger homes cost more to rebuild, which pushes the building sum insured — and therefore the premium — upward.

Construction materials: The home features aluminium external walls and a steel/Colorbond roof, both of which are considered durable, low-maintenance materials by insurers. Colorbond in particular is highly regarded for its resistance to fire, corrosion, and extreme weather, which can have a moderating effect on premiums.

Slab foundation: A concrete slab foundation is a standard, well-understood construction method that generally poses fewer risks than raised or suspended floors in terms of moisture and structural movement.

Above-average fittings: The above-average quality of internal fittings — think stone benchtops, quality appliances, and premium fixtures — increases the cost to repair or rebuild to the same standard, which is factored into both the building sum insured and the contents valuation.

Swimming pool: A pool adds replacement value to the property and can introduce liability considerations. Insurers typically account for pool infrastructure when calculating building cover.

Solar panels: Solar systems are increasingly common, but they do add to the rebuild cost and can be a target for storm damage. Ensuring your solar panels are adequately covered under your building policy is important.

Granny flat: A self-contained granny flat on the same property adds additional insurable structures, which contributes to the higher building sum insured.

Ducted climate control: Ducted air conditioning is a significant fixed asset. If damaged, it can be costly to repair or replace, and this is reflected in the overall building valuation.

No cyclone risk: Being outside a designated cyclone risk zone is a meaningful premium advantage for this property. Many Queensland homeowners pay a cyclone loading on top of their base premium — this property avoids that entirely.

---

Tips for Homeowners in Tallai

1. Review your building sum insured regularly With a sum insured of $1.5M, it's essential this figure reflects current construction costs. Building costs in South East Queensland have risen significantly in recent years. Underinsurance is a real risk — if your home is destroyed and the rebuild cost exceeds your sum insured, you'll be out of pocket for the difference. Consider getting a professional building valuation every two to three years.

2. Check your granny flat is fully covered Not all policies automatically include secondary dwellings under the main building cover. Confirm with your insurer that the granny flat — including its fixtures and any contents — is explicitly covered under your policy.

3. Don't overlook your solar system Solar panels are typically covered under building insurance, but the extent of cover (including inverters and battery storage, if applicable) varies between policies. Read the product disclosure statement carefully and ask your insurer to confirm exactly what's included.

4. Consider a higher excess to reduce your premium With both building and contents excesses currently set at $1,000, you may be able to lower your annual premium by opting for a higher excess — say $2,000 or $2,500 — if you're comfortable covering smaller claims out of pocket. This is particularly worth considering for a property of this value, where you're unlikely to claim for minor incidents.

---

Compare Quotes and Find Better Value

Whether you're renewing your existing policy or shopping for cover for the first time, it pays to compare. CoverClub makes it easy to see how your quote stacks up against real data from properties in your area. Get a home insurance quote today and find out if you're getting the best deal available for your Tallai home.