Tallai is a quiet, leafy suburb nestled in the Gold Coast hinterland — known for its acreage-style blocks, elevated outlooks, and relaxed lifestyle. It's the kind of place where a well-built, free-standing family home is the norm, and protecting that asset with the right insurance matters. This article breaks down a real home and contents insurance quote for a four-bedroom free-standing home in Tallai (QLD 4213), comparing it against local, state, and national benchmarks to help you understand whether you're getting a fair deal.

---

Is This Quote Fair?

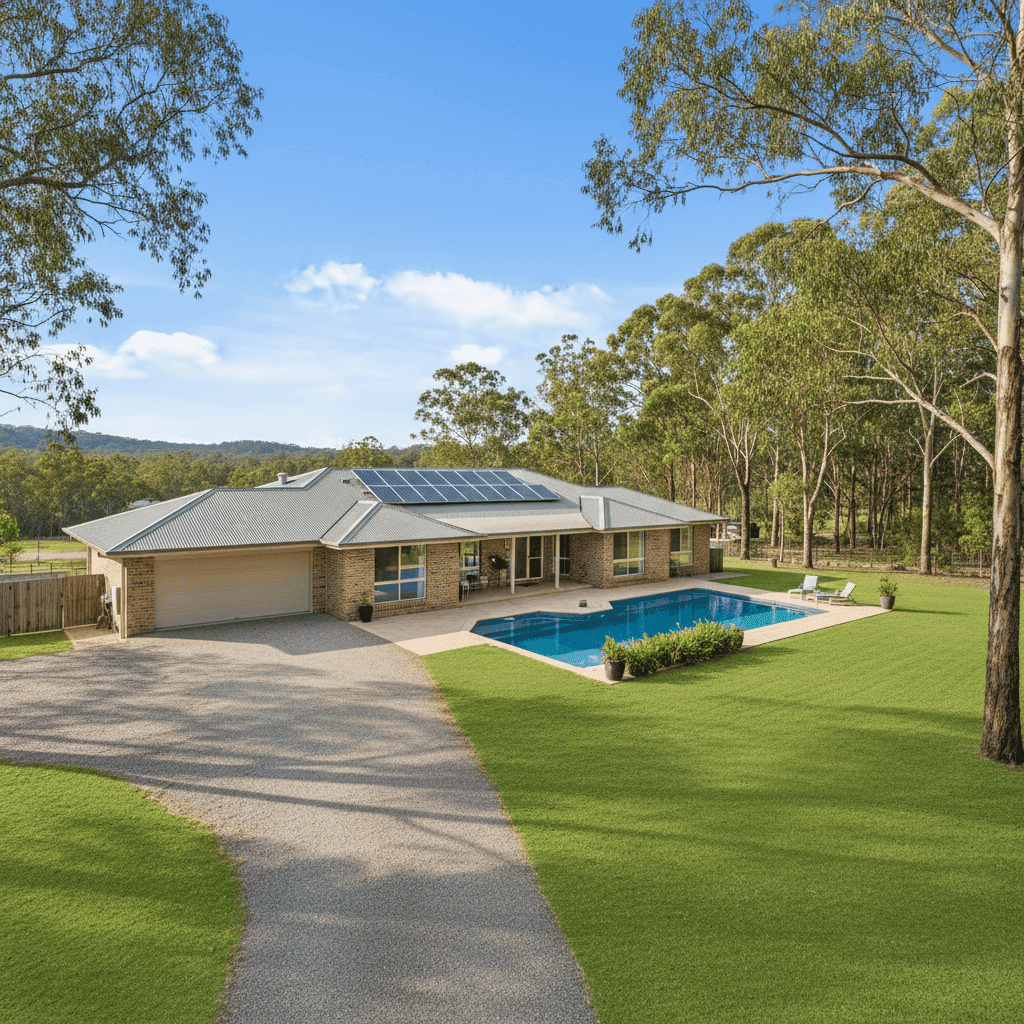

The quote in question comes in at $3,744 per year (or $354 per month) for combined home and contents cover, with a building sum insured of $900,000 and contents valued at $251,000. Both the building and contents excess are set at $2,000.

Our pricing engine has rated this quote as CHEAP — below average for the area. That's a meaningful finding. When you consider that the suburb average premium in Tallai sits at $6,447 per year and the median is $5,305 per year, this quote comes in well below both markers — saving the homeowner roughly $2,700 compared to the average and over $1,500 compared to the median.

Even measured against the 25th percentile of quotes in the suburb (meaning 75% of comparable quotes are more expensive), the Tallai benchmark is $4,777 per year — still notably higher than this quote. In other words, this is genuinely one of the more competitive prices available in the area, not just marginally below average.

For a property of this size and specification — 235 sqm, brick veneer construction, Colorbond roof, with a pool, solar panels, and ducted climate control — this represents solid value. Homeowners in Tallai should feel confident that a quote at this level is worth taking seriously.

---

How Tallai Compares

To put this quote in proper context, it helps to look at the broader pricing landscape across different geographies.

| Benchmark | Premium |

|---|---|

| This Quote | $3,744/yr |

| Tallai (suburb average) | $6,447/yr |

| Tallai (suburb median) | $5,305/yr |

| Gold Coast LGA average | $8,161/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. The Gold Coast LGA average of $8,161 is strikingly high — a reflection of the region's exposure to severe weather events, storm surge risk in coastal pockets, and the generally high property values across the Gold Coast. Tallai, being inland and elevated, tends to attract lower premiums than beachside or low-lying Gold Coast suburbs, which helps explain why the suburb median ($5,305) is more moderate than the LGA figure.

The QLD state average of $9,129 is one of the highest in the country, driven largely by cyclone-prone northern Queensland regions and flood-affected inland areas. This particular property sits outside a designated cyclone risk zone, which is a significant premium advantage.

Compared to the national average of $5,347, this quote is still well below the mark — and against the national median of $2,764, it sits in a reasonable mid-range position when accounting for the high sum insured and contents value.

You can explore more local pricing data on the Tallai suburb stats page, the QLD state insurance overview, or the national home insurance statistics.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers price the risk — some favourably, others less so.

Brick Veneer Walls & Colorbond Roof Brick veneer is generally viewed positively by insurers. It's durable, fire-resistant, and performs well in storms. Combined with a steel Colorbond roof — which is lightweight, resistant to corrosion, and well-suited to Queensland's climate — this construction profile typically attracts more competitive premiums than, say, weatherboard or fibrous cement cladding.

Concrete Slab Foundation A slab foundation is a stable, low-maintenance base that insurers tend to favour over raised timber stumps, which can be more susceptible to moisture damage and movement over time. It's a quiet but genuine premium benefit.

Swimming Pool A pool adds liability exposure to any home insurance policy. If a guest or visitor is injured in or around the pool, the homeowner may face a public liability claim — and insurers factor this into their pricing. It's worth checking that your policy includes adequate liability cover, typically $20 million or more.

Solar Panels Solar panels are increasingly common in Queensland, and most home insurance policies will cover them as a fixed fixture of the building. However, it's worth confirming with your insurer exactly what's covered — particularly for storm damage, hail impact, or inverter failure — as coverage can vary between providers.

Ducted Climate Control Ducted air conditioning systems are expensive to repair or replace. At 235 sqm across four bedrooms and three bathrooms, a full ducted system represents a meaningful portion of the building's value. Ensuring your sum insured accounts for this is important.

Timber & Laminate Flooring Timber and laminate floors can be costly to repair after water ingress events — a real consideration in Queensland. Some policies have specific conditions around water damage to flooring, so it pays to read the Product Disclosure Statement carefully.

---

Tips for Homeowners in Tallai

1. Review your sum insured annually Construction costs in South East Queensland have risen sharply in recent years. A $900,000 building sum insured may be appropriate now, but it's worth recalculating your rebuild cost each year — particularly if you've done renovations or if local building costs have shifted. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Check your contents figure is realistic $251,000 in contents cover sounds substantial, but it can be easy to underestimate. Walk through your home and consider furniture, appliances, clothing, jewellery, outdoor equipment, and anything in your garage. A detailed home inventory — even a simple photo record — can help you arrive at a more accurate figure and support any future claims.

3. Understand what your pool liability covers Queensland has strict pool safety regulations, and any non-compliance could complicate a liability claim. Ensure your pool fence and safety equipment meet current Gold Coast City Council requirements, and confirm that your policy's liability section specifically covers pool-related incidents.

4. Compare before you renew Even if your current premium looks competitive, insurers regularly adjust their pricing models. What's cheap today may not be next year. Set a reminder to compare quotes at least 30 days before your renewal date — you may find a better deal or use a competing quote to negotiate with your existing insurer.

---

Ready to Compare?

Whether you're a first-time buyer in the Gold Coast hinterland or a long-term Tallai resident reviewing your cover, comparing quotes is the single most effective way to ensure you're not overpaying. Get a home insurance quote at CoverClub and see how your premium stacks up against the market in minutes.