Nestled in the hinterland fringe of the Gold Coast, Tallai is a sought-after suburb known for its leafy acreage blocks, elevated terrain, and prestige residential properties. If you own a large free standing home in this postcode, you're likely paying a premium for the privilege — and your home insurance bill may reflect that too. This article breaks down a real home and contents insurance quote for a five-bedroom property in Tallai (QLD 4213), putting the numbers in context so you can judge whether you're getting a fair deal.

---

Is This Quote Fair?

The quote in question comes in at $8,897 per year (or $853/month) for combined home and contents cover, with a $2,400,000 building sum insured and $125,000 in contents. Our price rating for this quote is Expensive — Above Average.

That rating isn't arbitrary. Based on 36 quotes collected for Tallai, the suburb average sits at $6,447/yr and the median at $5,305/yr. This quote lands well above both benchmarks — roughly 38% above the suburb average and 68% above the median. It also sits above the suburb's 75th percentile of $7,793/yr, meaning it's more expensive than at least three-quarters of comparable quotes in the area.

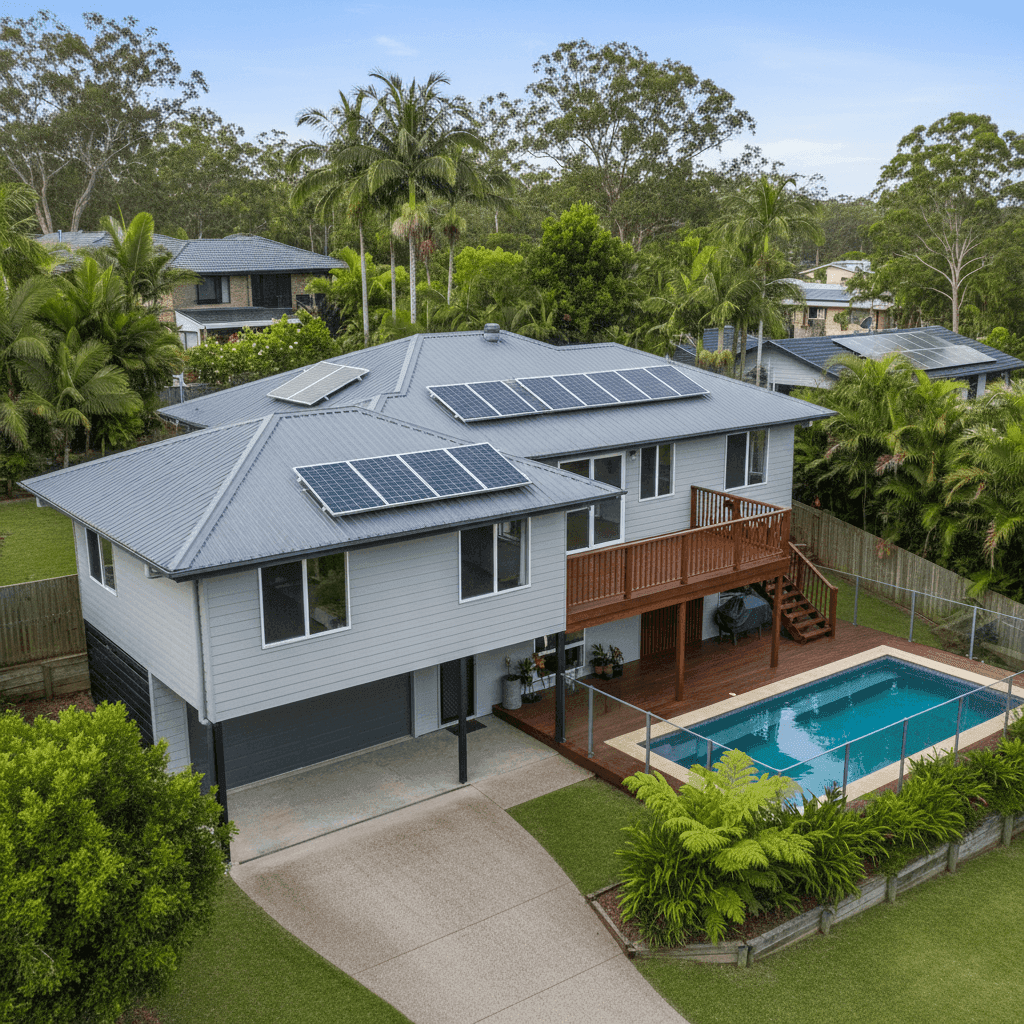

That said, context matters. This is a large, high-value property — 367 sqm, five bedrooms, three bathrooms, elevated construction, a pool, solar panels, and above-average fittings. Insurers price risk based on the cost to rebuild, not the land value, and a home of this specification carries a genuinely high replacement cost. A $2.4 million sum insured is substantial, and that figure alone will push the premium into a higher bracket regardless of location.

So while the quote is on the expensive side relative to Tallai peers, the property's characteristics go a long way toward explaining the gap.

---

How Tallai Compares

To understand whether Tallai is simply an expensive suburb to insure, it helps to zoom out and look at the broader data.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Tallai (QLD 4213) | $6,447/yr | $5,305/yr |

| Gold Coast LGA | $8,161/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

You can explore the full Queensland insurance data and national benchmarks on CoverClub.

A few things stand out here. First, the QLD state average of $9,129/yr is actually higher than this quote — so relative to Queensland as a whole, $8,897 is slightly below average. This reflects the outsized influence of high-risk coastal and cyclone-prone areas in North Queensland, which drag the state average upward significantly.

Second, the wide gap between the QLD average ($9,129) and median ($3,903) tells an important story: Queensland's insurance market is heavily skewed by extreme outliers. The median is a more reliable indicator of what a typical Queensland homeowner pays, and at $3,903, it's well below this quote.

Third, Tallai's own suburb average ($6,447) is above the national average ($5,347), confirming that the Gold Coast hinterland is a moderately expensive area to insure — even before factoring in property-specific features.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence the insurance premium, and it's worth understanding each one.

High sum insured. A $2.4 million building sum insured is the single biggest driver of cost here. Larger homes with premium fittings cost significantly more to rebuild, and insurers price accordingly. Above-average fittings — think high-end kitchens, quality flooring, and premium fixtures — increase the per-square-metre rebuild cost beyond standard estimates.

Elevated construction. The property is elevated by at least one metre. While this can reduce flood risk in some scenarios, elevated homes can be more complex and expensive to repair or rebuild, which may be reflected in the premium.

Hardiplank/Hardiflex cladding. This fibre cement cladding is a popular and durable choice, generally regarded favourably by insurers compared to older weatherboard or asbestos-based materials. It's relatively fire-resistant and low-maintenance, which can work in your favour at renewal time.

Colorbond steel roof. Steel roofing is considered a lower-risk profile than terracotta tiles in storm-prone areas, as it's less likely to crack or dislodge. In a Gold Coast context — where severe storms and hail are not uncommon — this is a meaningful factor.

Swimming pool. A pool adds to the insured value of the property and introduces additional liability considerations, both of which can nudge the premium upward.

Solar panels. Rooftop solar systems are increasingly common but represent a real replacement cost if damaged by hail, storm, or fire. Insurers factor this into the building sum insured, so it's important to ensure your nominated sum insured accounts for the system's replacement value.

Ducted climate control. Ducted air conditioning is a significant fixed asset. Like solar panels, it contributes to the overall replacement cost of the home and should be included in your sum insured calculation.

No cyclone risk. Tallai falls outside designated cyclone risk zones, which is a meaningful cost saving compared to properties in Far North Queensland. This helps keep the premium lower than it might otherwise be for a home of this size in a higher-risk postcode.

---

Tips for Homeowners in Tallai

1. Review your sum insured carefully. A $2.4 million sum insured is a significant figure. Make sure it genuinely reflects the cost to rebuild your home from scratch — including demolition, site clearance, professional fees, and the current cost of materials and labour. Underinsurance is a real risk, but overinsurance means you're paying more premium than necessary. Consider getting a professional building valuation every few years.

2. Shop around at renewal. The gap between Tallai's 25th percentile ($4,777/yr) and 75th percentile ($7,793/yr) is substantial — over $3,000 per year for broadly similar properties. That spread shows there's real variation between insurers. Use a comparison tool like CoverClub to see multiple quotes side by side before automatically renewing.

3. Check what's included for your pool and solar. Not all policies treat pools and solar panels the same way. Some policies include them as standard under building cover; others require specific endorsements or have sub-limits. Read your Product Disclosure Statement carefully and confirm with your insurer that both are adequately covered.

4. Maintain your property to support claims. Insurers can reduce or decline claims if damage is attributed to poor maintenance rather than a sudden event. Keeping your roof, gutters, cladding, and pool area in good condition not only protects your home but also protects your ability to claim when it matters most.

---

Compare Your Quote Today

Whether you're reviewing an existing policy or shopping for cover on a new property, it pays to compare. CoverClub makes it easy to benchmark your premium against real quotes from across your suburb, the Gold Coast, and Queensland as a whole. Get a quote now and see how your current insurer stacks up — you might be surprised by how much room there is to save.