Tallai is a quiet, leafy suburb nestled in the Gold Coast hinterland, known for its acreage properties and relaxed semi-rural lifestyle. If you own a large free standing home in this postcode, you already know that insuring it is no small expense — but how do you know if what you're paying is actually fair? In this article, we break down a real home and contents insurance quote for a six-bedroom property in Tallai (QLD 4213) and put it under the microscope against local, state, and national benchmarks.

---

Is This Quote Fair?

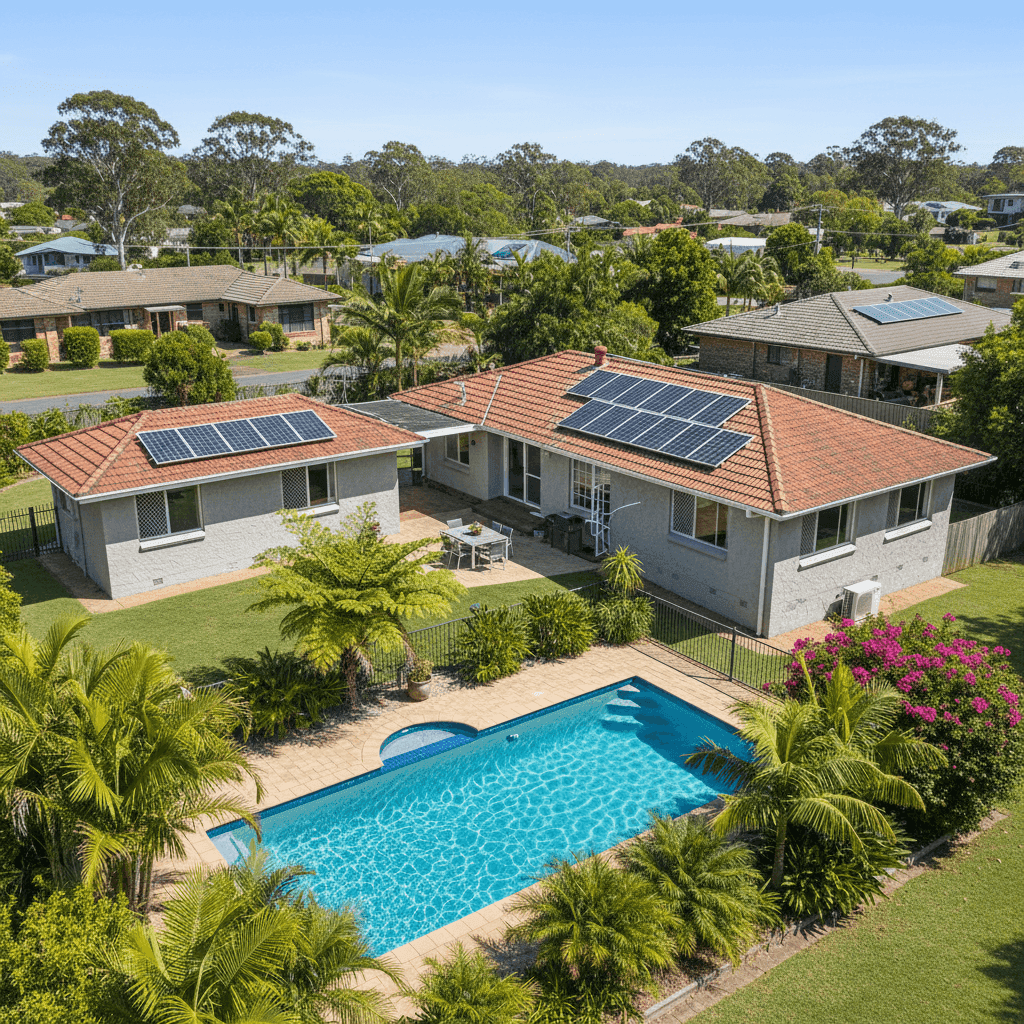

The quote in question comes in at $7,842 per year (or $752 per month) for a combined home and contents policy, covering a building sum insured of $1,341,000 and $50,000 in contents. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive (Above Average) — and the data backs that up. At $7,842 annually, this premium sits above the suburb average of $6,447 and comfortably above the suburb median of $5,305. It does fall just above the 75th percentile for Tallai ($7,793), meaning roughly three-quarters of comparable quotes in the area come in cheaper.

That said, "expensive" doesn't automatically mean "wrong." A 411 sqm home with a $1.34 million building sum insured, a pool, solar panels, ducted climate control, and a granny flat is a far more complex risk to insure than a standard suburban dwelling. The premium reflects genuine complexity — but there's still a reasonable case that a better price could be found by shopping around.

---

How Tallai Compares

To put this quote in proper context, it helps to look at the numbers across multiple levels. You can explore the full data on the Tallai suburb stats page, the QLD state stats page, and the national stats page.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Tallai (QLD 4213) | $6,447/yr | $5,305/yr |

| Gold Coast LGA | $8,161/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Queensland's average premium of $9,129 is notably higher than the national average of $5,347 — a gap largely driven by the state's exposure to extreme weather events, including floods, storms, and hail. Tallai itself, sitting in the hinterland rather than coastal flats, benefits from a lower cyclone risk classification, which helps keep premiums more manageable than many other QLD postcodes.

Interestingly, the Gold Coast LGA average of $8,161 actually exceeds the quote in question, suggesting that for the region as a whole, $7,842 is not out of step. The wide gap between Queensland's mean ($9,129) and median ($3,903) also tells an important story — a relatively small number of high-risk or high-value properties are pulling the average upward significantly. This property, with its large footprint and high sum insured, naturally sits in that upper tier.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding them helps you have a more informed conversation when comparing policies.

Fibro Asbestos Walls

This is one of the most significant premium drivers. Fibro asbestos (fibrous cement sheeting containing asbestos) requires specialist handling during any repair or rebuild, which substantially increases the cost of claims. Insurers price this risk accordingly, and some may apply exclusions or sub-limits. It's worth checking your policy wording carefully to understand exactly how asbestos-related repairs are covered.

Large Building Size & High Sum Insured

At 411 sqm and a sum insured of $1,341,000, this is a substantial property. The sum insured is the single biggest driver of building premium — the more it costs to rebuild, the more your insurer charges. It's worth periodically reviewing your sum insured with a quantity surveyor to ensure it's accurate: being over-insured costs you money, while being under-insured can leave you exposed at claim time.

Pool, Solar Panels & Ducted Climate Control

Each of these adds incremental value and risk. Swimming pools introduce liability considerations and can be costly to repair or replace. Solar panel systems — particularly older or larger arrays — can be a source of fire risk and add to the rebuild cost. Ducted climate control systems are expensive to repair and are typically included in the building sum insured. Together, these features justify a higher premium than a bare-bones property.

Granny Flat

The presence of a granny flat adds both building value and potential liability, particularly if it is or could be rented out. Some insurers treat granny flats differently depending on whether they're used for family accommodation or as a rental, so it's important to disclose this clearly and confirm coverage extends to the secondary dwelling.

Tiled Roof & Slab Foundation

Tiled roofs are generally viewed favourably by insurers compared to older metal or flat roofing, as they tend to perform well in storms. A concrete slab foundation is similarly considered low-risk, with minimal exposure to subsidence or moisture-related damage. These features work in the homeowner's favour.

---

Tips for Homeowners in Tallai

1. Get multiple quotes — especially with fibro asbestos walls Not all insurers are comfortable with fibro asbestos construction, and those that are may price it very differently. Using a comparison platform like CoverClub to run multiple quotes side by side is the most efficient way to find competitive pricing without sacrificing coverage.

2. Review your sum insured with a professional A $1.34 million sum insured on a 411 sqm home is significant. Engage a quantity surveyor or use an online building cost calculator to verify this figure. An accurate sum insured protects you from being underinsured while potentially reducing your premium if the current figure is higher than necessary.

3. Check your granny flat is explicitly covered Don't assume your policy automatically extends to a secondary dwelling. Contact your insurer directly to confirm the granny flat is included in your building cover, and ask whether any rental activity (current or future) affects your policy terms.

4. Consider a higher excess to reduce your premium With a $1,000 excess currently in place, there may be room to increase this — particularly for contents — in exchange for a lower annual premium. If you have a healthy emergency fund and are unlikely to make small claims, a higher excess can be a cost-effective trade-off.

---

Compare Your Home Insurance Today

Whether you're renewing your policy or shopping around for the first time, it pays to compare. CoverClub makes it easy to see multiple home insurance quotes for your Tallai property in one place — so you can make a confident, informed decision. Get a quote at CoverClub and find out if you could be paying less for the same level of protection.