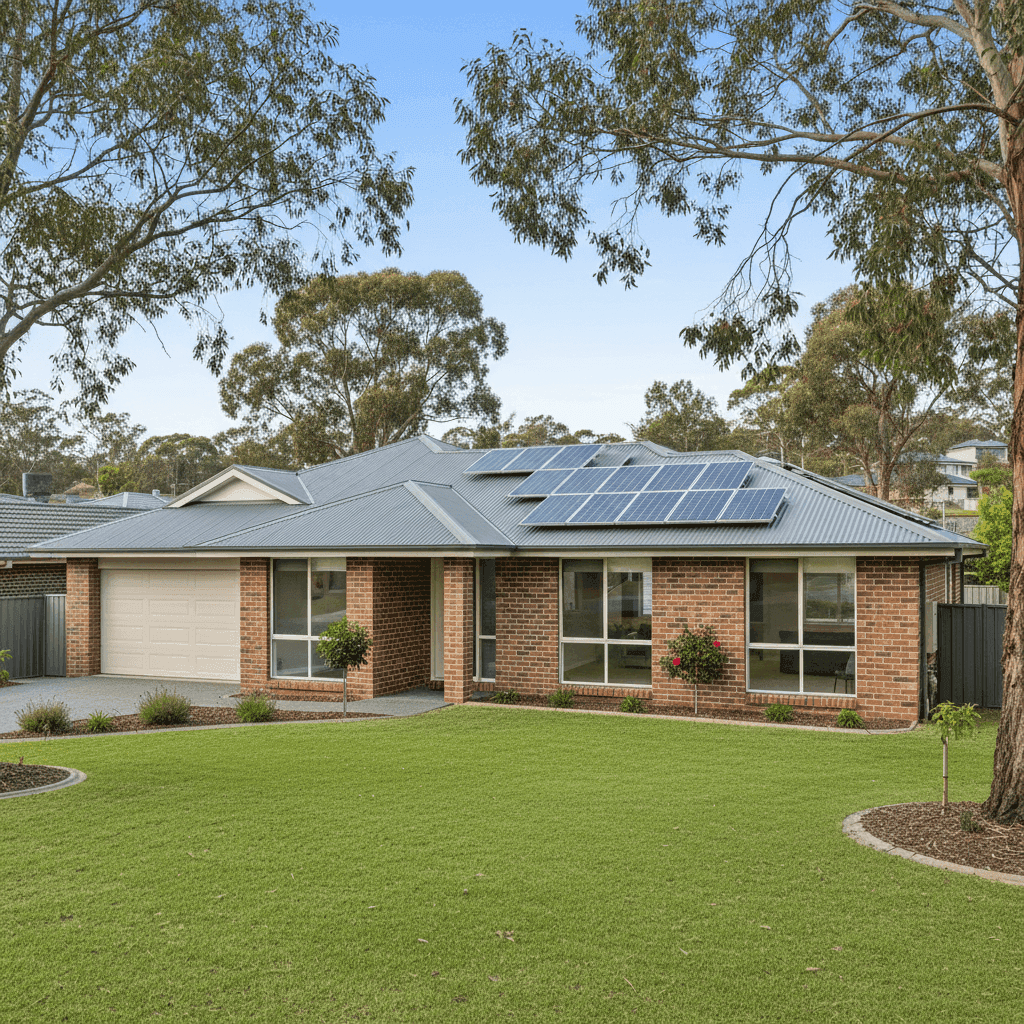

Tallwoods Village is a quiet, leafy residential community nestled near Forster on the NSW Mid-Coast. It attracts families and retirees alike with its golf course surrounds and relaxed coastal lifestyle. But owning a free standing home here — like anywhere in Australia — means making sure you have the right insurance in place. This article breaks down a recent home and contents insurance quote for a four-bedroom property in Tallwoods Village, examines whether the price stacks up, and shares practical tips to help local homeowners get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $3,803 per year (or $364/month) for combined home and contents insurance, covering a building sum insured of $1,011,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our pricing analysis rates this quote as Fair — Around Average. That's a reasonable outcome for a property of this size and specification. It's not the cheapest on the market, but it's also well within a normal range for a well-appointed four-bedroom home with above-average fittings, solar panels, and ducted climate control.

A "Fair" rating means the premium sits close to what most comparable properties in the area are paying — you're not being overcharged, but there may still be room to shop around and find a more competitive rate without sacrificing cover quality.

---

How Tallwoods Village Compares

To put this quote in context, here's how the $3,803 annual premium measures up against local, state, and national benchmarks:

| Benchmark | Premium |

|---|---|

| This quote | $3,803/yr |

| Tallwoods Village (suburb average) | $3,518/yr |

| Tallwoods Village (suburb median) | $3,528/yr |

| Tallwoods Village (25th percentile) | $2,387/yr |

| Tallwoods Village (75th percentile) | $4,598/yr |

| Mid-Coast LGA average | $5,840/yr |

| NSW average | $9,528/yr |

| NSW median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, this quote sits just slightly above the Tallwoods Village suburb average of $3,518 — a difference of roughly $285 per year. That's modest and well within the normal spread of quotes for this type of property.

Second, the quote is meaningfully below the Mid-Coast LGA average of $5,840 and well below the NSW state average of $9,528. It's worth noting that NSW state averages are heavily influenced by high-risk coastal and flood-prone areas, which can skew the numbers significantly upward. The median is a more reliable guide, and at $3,770, the NSW median is actually slightly higher than this quote — a positive sign.

Compared to national figures, this premium sits above the national median of $2,764 but below the national average of $5,347. Again, national averages are pulled upward by high-risk properties in Queensland and other cyclone-prone or flood-affected regions.

The suburb sample size of 13 quotes is relatively small, so treat local averages as a guide rather than a definitive benchmark. That said, the data paints a consistent picture: this is a fair, mid-range premium for the area.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding them can help you make sense of your quote — and potentially negotiate a better one.

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability compared to timber-framed cladding. Combined with a steel/Colorbond roof, which is highly resistant to fire, wind, and corrosion, this home presents a relatively low-risk profile from a construction standpoint.

Slab foundation is standard for homes built in this era and region, and it carries no particular premium loading. Similarly, timber and laminate flooring is common and doesn't significantly affect pricing either way.

The above-average fittings quality is worth noting. Kitchens and bathrooms with premium fixtures, stone benchtops, or high-end appliances cost more to repair or replace — and insurers price accordingly. This is likely contributing to the higher building sum insured of just over $1 million, which is substantial but appropriate for a 235 sqm home with quality finishes.

Solar panels add modest complexity to a home insurance policy. They represent an additional asset to insure and can complicate roof repairs. Most standard policies cover fixed solar panels as part of the building, but it's worth confirming this with your insurer.

Ducted climate control is another feature that increases rebuild costs and is reflected in the sum insured. These systems are expensive to replace and are factored into the overall building valuation.

Importantly, this property is not in a cyclone risk area, which is a meaningful cost advantage compared to properties further north along the Queensland coast. This helps keep the premium in a manageable range.

---

Tips for Homeowners in Tallwoods Village

1. Review your sum insured regularly With a building sum insured of $1,011,000, it's important to ensure this figure keeps pace with rising construction costs. Building costs in regional NSW have increased significantly in recent years. Use an independent building cost calculator annually to confirm your coverage remains adequate — underinsurance is one of the most common and costly mistakes homeowners make.

2. Shop around at renewal time Even a "Fair" rated quote has room for improvement. Insurers don't reward loyalty the way they once did, and premiums can vary by hundreds of dollars for essentially the same cover. Use a comparison service like CoverClub to run multiple quotes before your renewal date.

3. Check what's included for your solar panels Not all policies treat solar panels the same way. Some include them automatically as part of the building; others require a separate endorsement or have specific exclusions around inverter damage. Ask your insurer directly and get it in writing.

4. Consider your contents valuation carefully A contents value of $50,000 is on the lower end for a four-bedroom home with above-average fittings. Do a room-by-room inventory to make sure your electronics, furniture, appliances, clothing, and valuables are fully accounted for. Being underinsured on contents can leave you significantly out of pocket after a claim.

---

Compare Your Options with CoverClub

Whether you're renewing your existing policy or shopping for cover for the first time, it pays to compare. CoverClub makes it easy to see how your quote stacks up against real data from properties just like yours. Get a home insurance quote today and find out if you're getting the best deal available in Tallwoods Village.