Tamborine Mountain is one of South East Queensland's most picturesque addresses — a lush, elevated community in the Scenic Rim that attracts families and tree-changers alike. But living among the hinterland beauty comes with its own set of insurance considerations. This article breaks down a recent home and contents insurance quote for a four-bedroom free-standing home in Tamborine Mountain (QLD 4272), and puts the numbers into context so you can judge whether your own policy is working hard enough for you.

---

Is This Quote Fair?

The quote in question comes in at $2,821 per year (or $270 per month), covering a building sum insured of $917,000 and $50,000 in contents — with a $5,000 excess applied to both building and contents claims.

Our price rating for this quote is FAIR (Around Average), which means it sits comfortably within the normal range for the area — neither a standout bargain nor an overpriced outlier. To understand what "around average" really means here, it helps to look at where this premium sits within the broader distribution of quotes we've collected for Tamborine Mountain (QLD 4272).

Based on 85 quotes from the suburb:

- 25th percentile: $2,531/yr

- Suburb average: $3,632/yr

- Suburb median: $3,478/yr

- 75th percentile: $4,279/yr

At $2,821, this quote sits below both the suburb average and median, and only modestly above the 25th percentile. That's a solid result. Homeowners paying closer to the suburb average are spending over $800 more per year for comparable cover — so while there may be room to shop around for a better deal, this is by no means an inflated premium.

---

How Tamborine Mountain Compares

One of the most striking things about this quote is how it compares to broader benchmarks. Queensland is one of Australia's most expensive states for home insurance, driven largely by cyclone-prone regions in the north and flood-affected areas across the state.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Tamborine Mountain (suburb) | $3,632/yr | $3,478/yr |

| Scenic Rim LGA | $8,744/yr | — |

| Queensland (state) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

The QLD state average of $9,129/yr is heavily skewed by high-risk postcodes in Far North Queensland, which is why the median of $3,903/yr is a more representative figure for most Queensland homeowners. Even so, this quote at $2,821 comes in below the state median — a meaningful saving.

Compared to the national picture, the quote also sits comfortably below the national average of $5,347/yr, and only slightly above the national median of $2,764/yr. For a property of this size and value in a hinterland suburb, that's a reasonable outcome.

The Scenic Rim LGA average of $8,744/yr is particularly eye-catching. This figure is likely pulled upward by higher-risk properties elsewhere in the LGA — including flood-prone valleys and more remote rural holdings — which can carry significantly higher premiums than an established residential suburb like Tamborine Mountain.

---

Property Features That Affect Your Premium

Several characteristics of this property play a meaningful role in how insurers price the risk.

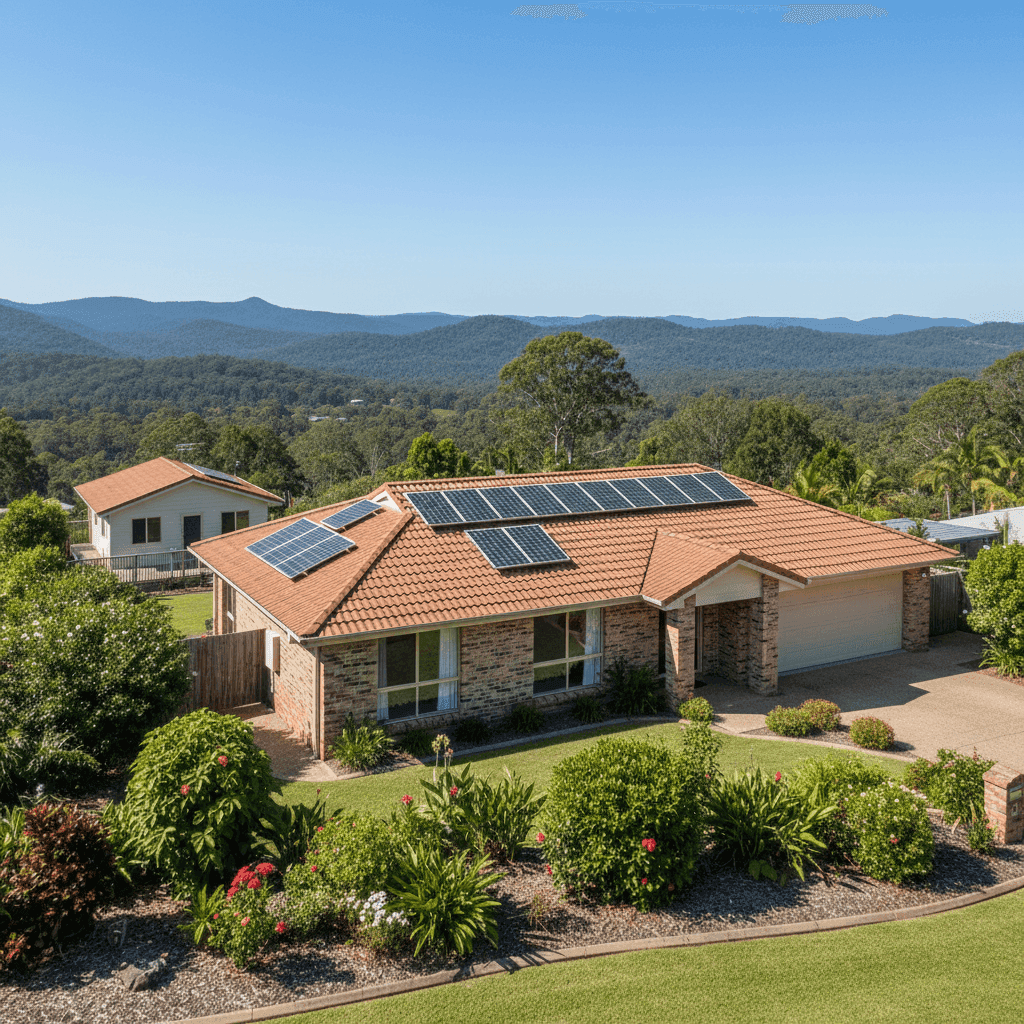

Brick veneer construction and tiled roof are generally viewed favourably by insurers. Brick veneer walls offer solid fire resistance and structural durability, while concrete tiles are more resilient than metal or fibrous cement in many weather scenarios. Together, these features tend to attract more competitive premiums compared to timber-framed or Colorbond-roofed homes.

Slab foundation is another positive signal for insurers — slab homes are typically less susceptible to certain types of subsidence and pest-related structural damage than homes on stumps or piers.

Solar panels add a layer of complexity to home insurance. They represent a capital asset on the roof that needs to be covered, and some insurers include them under building cover while others treat them separately. It's worth confirming with your insurer exactly how your solar system is covered — particularly for damage from storms or hail.

Ducted climate control is a high-value fixture that contributes to the building sum insured. At $917,000, the insured value accounts for the full cost of rebuilding a 139 sqm home with quality fittings, including systems like ducted air conditioning, which can be expensive to replace.

The granny flat is a significant factor. Secondary dwellings on the same property need to be explicitly included in your building cover. If the granny flat is used for rental income, some insurers may require a landlord endorsement or a separate policy altogether — it's worth clarifying this with your provider.

No cyclone risk is a notable advantage for this property. Tamborine Mountain sits outside the designated cyclone risk zone, which spares homeowners from the substantial cyclone-related premium loadings that affect properties further north in Queensland.

---

Tips for Homeowners in Tamborine Mountain

1. Check your granny flat is fully covered Secondary dwellings are a common source of underinsurance. Make sure your policy explicitly covers the granny flat as part of the building sum insured — and if it's tenanted, speak to your insurer about whether a landlord policy or endorsement is required.

2. Review your solar panel coverage Solar systems are increasingly valuable and increasingly targeted by thieves, and they're also vulnerable to storm and hail damage. Confirm whether your panels are covered under building or contents, what the sub-limit is, and whether accidental damage is included.

3. Reassess your sum insured regularly Building costs in regional Queensland have risen sharply in recent years. A 1988-built home with standard fittings may cost significantly more to rebuild today than it would have even three years ago. Use an independent building cost calculator or speak with a quantity surveyor to ensure your $917,000 sum insured still reflects true replacement cost.

4. Consider your excess carefully A $5,000 excess on both building and contents is on the higher end. While a higher excess does reduce your annual premium, it means you'll need to fund a significant portion of any claim yourself. If a $5,000 out-of-pocket cost would be a financial strain, it may be worth modelling the premium difference at a lower excess level.

---

Compare Your Options with CoverClub

Whether you're renewing your policy or shopping around for the first time, it pays to see what the market has to offer. CoverClub makes it easy to compare home and contents insurance quotes for properties across Tamborine Mountain and the broader Scenic Rim. Get a quote today and find out whether your current premium is truly competitive — or whether there's a better deal waiting for you.