Nestled in the hinterland of South East Queensland, Tamborine Mountain is one of the region's most sought-after lifestyle addresses. With its lush rainforest surrounds, elevated terrain, and well-established residential streets, it attracts homeowners who value character and tranquillity. But living in a scenic, semi-rural setting also comes with its own insurance considerations — and understanding what you're paying for matters.

This article breaks down a recent home and contents insurance quote for a four-bedroom, three-bathroom free-standing home in Tamborine Mountain (postcode 4272), examining whether the premium stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The quoted annual premium of $4,120 (or $388/month) covers both building (sum insured: $1,048,000) and contents ($203,000), with a $2,000 excess on each. Our analysis rates this quote as FAIR — Around Average.

That rating reflects a premium that sits comfortably within the normal range for the suburb. Based on 85 quotes collected for Tamborine Mountain, the suburb's average annual premium is $3,632, with a median of $3,478. The 75th percentile sits at $4,279, meaning this quote is in the upper-middle band — higher than most, but not an outlier.

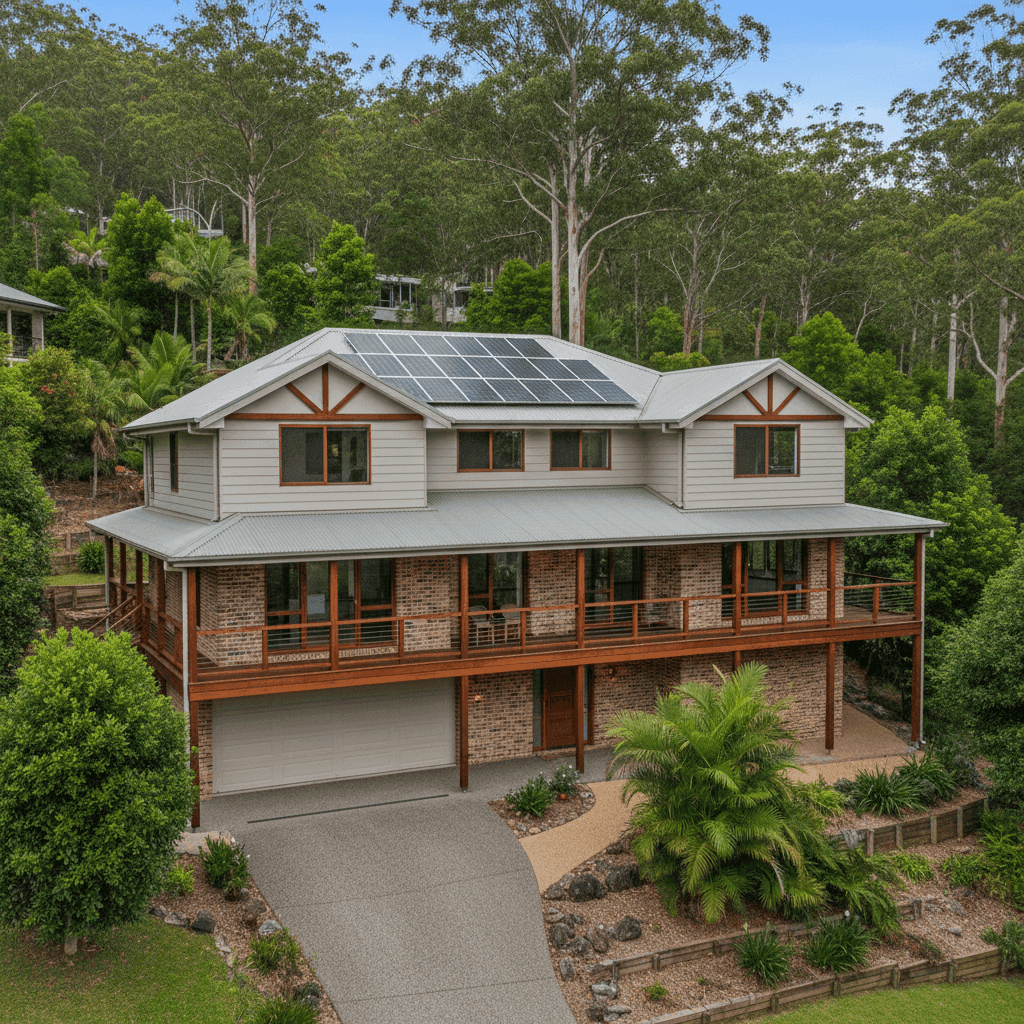

Given the property's size (186 sqm), age (built 1985), and features like solar panels and ducted climate control — all of which add to replacement cost — a premium near the top quartile is not unreasonable. The building sum insured of just over $1 million also reflects a thorough replacement cost estimate for a well-appointed home of this size and construction type.

In short: this isn't a bargain, but it's not excessive either. There may be room to shop around, but the figure is broadly defensible.

---

How Tamborine Mountain Compares

To put this quote in context, it helps to zoom out and look at the broader picture.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Tamborine Mountain (4272) | $3,632/yr | $3,478/yr |

| Scenic Rim LGA | $8,744/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, the Queensland state average of $9,129 is dramatically higher than the Tamborine Mountain suburb average — a gap largely driven by high-risk coastal and cyclone-prone postcodes across Far North Queensland pushing the mean upward. The state median of $3,903 is a more useful comparison, and the quote of $4,120 sits just above that figure.

Similarly, the national average of $5,347 is skewed by expensive markets in cyclone zones and flood-prone areas. The national median of $2,764 is lower than Tamborine Mountain's suburb median, which reflects the elevated risk profile of hinterland properties — including bushfire exposure and the potential for storm and rainwater damage in this elevated, heavily vegetated area.

Interestingly, the Scenic Rim LGA average of $8,744 is significantly higher than the Tamborine Mountain suburb average. This suggests that while Tamborine Mountain sits within the Scenic Rim council area, its specific risk profile is more favourable than many other parts of the LGA — a meaningful distinction worth keeping in mind when comparing quotes.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated.

Double brick construction is generally viewed favourably by insurers. It offers strong resistance to fire, wind, and impact damage compared to timber-framed or weatherboard homes, which can translate to lower rebuild risk and, in some cases, lower premiums.

Steel/Colorbond roofing is another positive. Colorbond is durable, lightweight, and performs well in both high-wind and bushfire-prone environments. It's a common and well-regarded roofing choice for Queensland properties.

Stump foundations are worth noting. Homes built on stumps — particularly older ones like this 1985 build — can be more vulnerable to underfloor moisture, pest activity, and movement over time. Insurers may factor this into their risk assessment, particularly for a property of this age.

Timber and laminate flooring adds to the contents and fixtures value, and can be more costly to repair or replace following water or fire damage than concrete slab flooring.

Solar panels increase the insured value of the property. Panels are typically covered under building insurance, and their replacement cost contributes to the overall sum insured. With solar increasingly common on Queensland homes, most insurers now price this in as standard.

Ducted climate control is another higher-value fixture that lifts the replacement cost estimate. Systems of this kind can cost tens of thousands of dollars to reinstall, and their inclusion in the building sum insured is appropriate.

Finally, the 1985 construction year means this home is now 40 years old. Older homes can carry higher reinstatement costs due to the need to bring electrical, plumbing, and structural elements up to current building codes during a rebuild — something that's baked into a well-calculated sum insured.

---

Tips for Homeowners in Tamborine Mountain

1. Review your sum insured regularly. Building costs in Queensland have risen sharply in recent years. A sum insured of $1,048,000 for a 186 sqm home works out to roughly $5,634 per square metre — which is on the higher end but may be appropriate given the age, construction type, and fixtures. Review this figure annually and use a building cost calculator to confirm it reflects current rebuild costs.

2. Consider your bushfire and storm risk. Tamborine Mountain's elevated, heavily vegetated environment means bushfire and severe storm exposure are genuine considerations. Ensure your policy includes adequate coverage for these events and check whether any exclusions or sub-limits apply to outbuildings, fences, or landscaping.

3. Don't set and forget your contents value. At $203,000, the contents sum insured is substantial. It's worth periodically auditing your belongings — particularly electronics, furniture, appliances, and valuables — to ensure this figure remains accurate. Underinsurance is one of the most common and costly mistakes homeowners make.

4. Shop around at renewal. Even a "fair" quote can be beaten. Insurers reprice risk differently, and loyalty doesn't always pay. Use a comparison platform like CoverClub to benchmark your renewal quote before you accept it — especially if your circumstances have changed.

---

Compare Your Options with CoverClub

Whether you're buying, renewing, or simply curious about what your home should cost to insure, CoverClub makes it easy to see how your quote stacks up. Get a home insurance quote today and compare it against real data from your suburb, your state, and across Australia — so you can make a confident, informed decision.