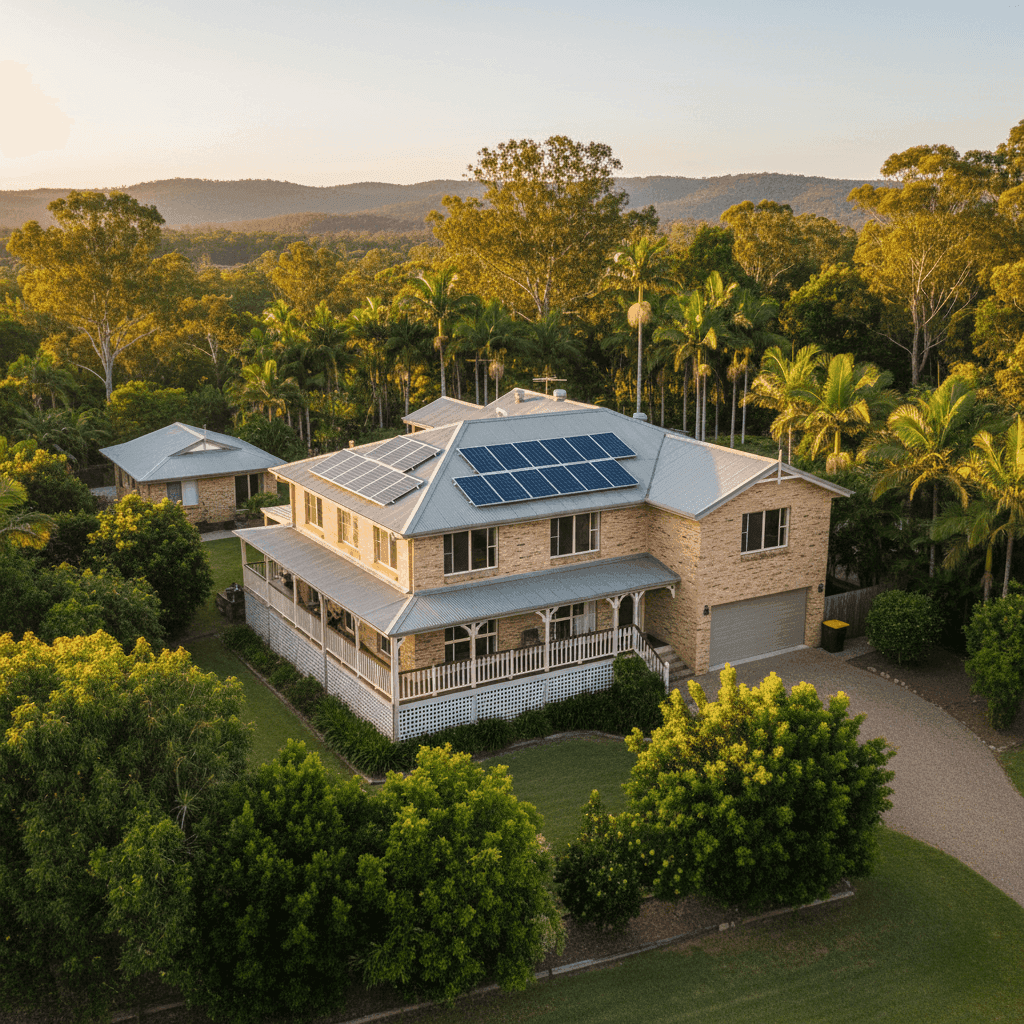

Tanawha is a leafy, semi-rural suburb nestled in the Sunshine Coast hinterland — known for its large blocks, established homes, and relaxed lifestyle. If you own a free standing home here, you're likely paying close attention to the cost of protecting it. This article breaks down a recent home and contents insurance quote for a five-bedroom, double brick property in Tanawha (postcode 4556), rated Fair (Around Average), and puts it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium on this quote comes in at $5,422 per year (or $530 per month), covering both building and contents. The building is insured for $1,178,000 and contents for $99,000, with a $1,000 excess applying to both.

Our pricing engine has rated this quote as Fair — Around Average, which means it sits comfortably within the typical range for comparable properties in Tanawha. It's not the cheapest quote on the market, but it's also well clear of the top end of the pricing spectrum for the suburb.

For a 277 sqm double brick home built in 1989 with a granny flat, solar panels, and ducted climate control, this premium reflects a property with above-average replacement complexity. Double brick construction and a large footprint push rebuild costs higher, which in turn lifts the sum insured — and ultimately, the premium.

At $5,422, you're paying slightly above the suburb median of $4,893 but below the suburb average of $5,666. That's a reasonable position to be in, especially given the elevated sum insured and the additional structures and features on the property.

---

How Tanawha Compares

Understanding how your premium stacks up regionally is one of the most useful exercises a homeowner can do. Here's a snapshot of where this quote sits across different benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $5,422/yr |

| Tanawha Suburb Average | $5,666/yr |

| Tanawha Suburb Median | $4,893/yr |

| Tanawha 25th Percentile | $4,433/yr |

| Tanawha 75th Percentile | $6,388/yr |

| Sunshine Coast LGA Average | $7,249/yr |

| QLD State Average | $9,129/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

Based on [Tanawha suburb data](https://coverclub.com.au/stats/QLD/4556/tanawha) from 17 quotes in our dataset.

A few things stand out here. First, the QLD state average of $9,129 per year is dramatically higher than this quote — but that figure is heavily skewed by high-risk coastal and cyclone-prone regions in Far North Queensland. Tanawha, fortunately, is not classified as a cyclone risk area, which keeps premiums significantly more manageable.

Second, the national average of $5,347 is actually very close to this quote, suggesting it's broadly in line with what Australians across the country are paying. The national median of $2,764, however, is far lower — a reminder that medians reflect the middle of the market, which often includes smaller properties with lower sums insured.

The Sunshine Coast LGA average of $7,249 is worth noting. Tanawha's suburb-level averages are notably lower than the broader LGA figure, likely because the suburb skews towards solid, well-built homes on larger blocks, without the flood or storm surge exposure that affects coastal Sunshine Coast suburbs.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on what insurers charge:

Double Brick Construction Double brick is one of the more durable — and more expensive — wall types to rebuild. Insurers price this in, as the cost per square metre for brick reconstruction is higher than, say, timber or clad homes. It does, however, offer excellent resilience against fire and wind damage, which can work in your favour at claims time.

Steel/Colorbond Roof Colorbond roofing is widely regarded as a low-maintenance, durable option. Insurers generally view it favourably compared to older tile roofs, which can crack or allow water ingress. It also performs well in hail events, which are not uncommon in South East Queensland.

Granny Flat The presence of a granny flat adds to the overall replacement value of the property. If the granny flat is included in the building sum insured (as it should be), this contributes to the higher-than-average $1,178,000 building cover figure. Make sure your policy explicitly covers any secondary dwellings on the property.

Solar Panels Solar panels are increasingly common on Australian homes, but they're often misunderstood from an insurance perspective. Most home insurance policies cover solar panels as a fixed fixture of the building — but it's worth confirming this with your insurer, particularly for panels that may be damaged in storms or hail.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset and add to the replacement cost of the home. They're typically covered under building insurance as a permanently installed fixture.

Slab Foundation & Tile Flooring A concrete slab foundation is standard in this era of Queensland construction and presents no unusual risk factors. Tile flooring is similarly straightforward — durable and relatively inexpensive to replace compared to hardwood or engineered timber.

Slightly Elevated (Less Than 1m) The property is noted as slightly elevated, which can offer a degree of passive flood protection. While Tanawha is not a high-flood-risk area, any elevation above natural ground level is a minor positive from a risk perspective.

---

Tips for Homeowners in Tanawha

1. Review Your Granny Flat Coverage If you have a granny flat on your property, confirm with your insurer that it's explicitly included in your building sum insured. Some policies treat secondary dwellings as separate structures with limited cover, while others include them fully. Don't assume — ask.

2. Check Your Solar Panel Policy Wording Solar panels can be damaged by hail, storms, or falling debris. Review your policy's Product Disclosure Statement (PDS) to confirm panels are covered and understand any sub-limits that may apply. If you've recently added panels or upgraded your system, notify your insurer so the sum insured remains accurate.

3. Reassess Your Building Sum Insured Regularly Construction costs in South East Queensland have risen significantly over recent years. A 277 sqm double brick home with a granny flat is expensive to rebuild — and underinsurance is a real risk if your sum insured hasn't kept pace with rising labour and material costs. Use a building calculator or speak with a quantity surveyor to validate your figure.

4. Compare Quotes Before Renewal Home insurance premiums can vary considerably between insurers for the same property. With this quote rated as Fair (Around Average), there may be room to find a more competitive price without sacrificing cover quality. CoverClub makes it easy to compare multiple quotes side by side so you can make an informed decision at renewal time.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for new cover, comparing quotes is the smartest first step. Get a home insurance quote at CoverClub and see how your premium stacks up against the market — it only takes a few minutes and could save you hundreds each year.

You can also explore detailed pricing data for Tanawha (4556), the broader QLD market, or national home insurance trends to better understand where your premium sits.