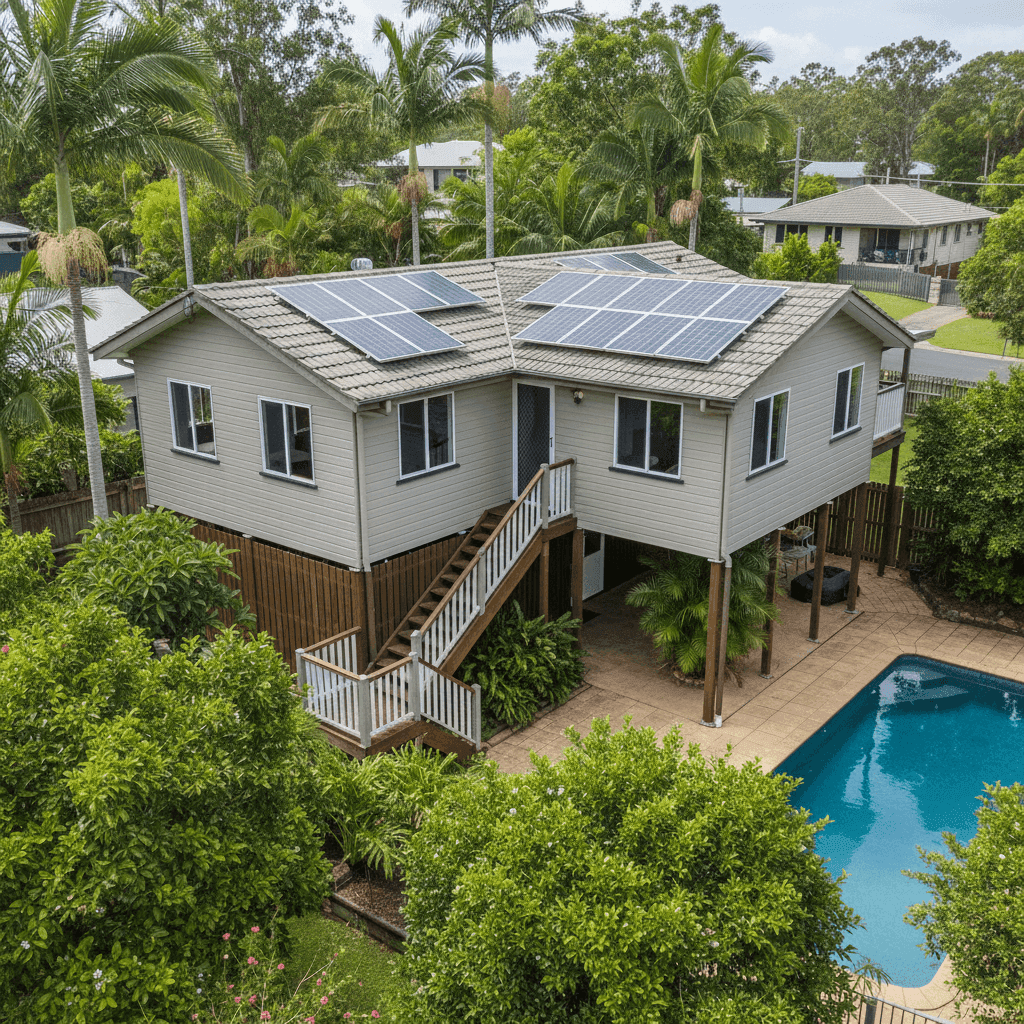

If you own a free standing home in Taranganba, QLD 4703, you already know that insuring a property in coastal Central Queensland comes with its own set of considerations. From cyclone exposure to the unique construction styles common in the region, home insurance premiums here can vary significantly depending on your property's features and the level of cover you choose. This article takes a close look at a recent Home and Contents insurance quote of $3,685 per year for a four-bedroom, two-bathroom weatherboard home in Taranganba — and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The short answer: yes, broadly speaking. This quote has been rated Fair (Around Average), and the data backs that up.

At $3,685 per year (or $361 per month), this premium sits comfortably above the suburb median of $2,124/yr but well below the suburb's 75th percentile of $4,184/yr. That means roughly three-quarters of comparable quotes in the area come in at a similar price or higher — which is a reasonable position to be in given the property's features and risk profile.

It's also worth noting that this quote covers a $750,000 building sum insured alongside $100,000 in contents, which is a fairly comprehensive level of cover. The building excess is set at $2,000 and the contents excess at $500 — both reasonable figures for a property of this type in a cyclone-designated area.

When you factor in the cyclone risk, the pool, solar panels, and the elevated pole construction, a premium in this range is not unexpected. Insurers price these features into their models, and Taranganba's location near Yeppoon on the Capricorn Coast means cyclone loading is a real and consistent cost driver.

---

How Taranganba Compares

Understanding where your premium sits relative to others is one of the most useful things you can do as a homeowner. Here's how this quote stacks up:

| Benchmark | Premium |

|---|---|

| This Quote | $3,685/yr |

| Taranganba Suburb Average | $2,855/yr |

| Taranganba Suburb Median | $2,124/yr |

| Taranganba 25th Percentile | $1,624/yr |

| Taranganba 75th Percentile | $4,184/yr |

| Livingstone LGA Average | $3,949/yr |

| QLD State Average | $4,547/yr |

| QLD State Median | $3,931/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

A few things stand out here. First, this quote is below both the QLD state average ($4,547/yr) and the Livingstone LGA average ($3,949/yr) — which is encouraging. Queensland consistently ranks as one of the most expensive states for home insurance in Australia, largely due to cyclone, flood, and storm risk, so coming in under the state average is a meaningful result.

Second, while the quote is above the Taranganba suburb average of $2,855/yr, it's important to remember that averages can be skewed by properties with lower sum insured values or fewer risk features. A 235 sqm home with a pool, solar panels, and a $750,000 building sum insured will naturally attract a higher premium than a smaller, simpler property.

You can explore more local data on the Taranganba suburb stats page, compare it against Queensland-wide figures, or see how it measures up against national benchmarks.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct influence on the premium quoted. Understanding these can help you make sense of the cost — and potentially identify areas where adjustments could be made.

Cyclone Risk Area

This is the single biggest factor. Taranganba falls within a designated cyclone risk zone, which means insurers apply a cyclone loading to premiums. This is non-negotiable for properties in the region and accounts for a significant portion of the cost differential between QLD and the national average.

Weatherboard Timber Construction

Weatherboard wood external walls are considered a higher-risk construction material compared to brick veneer or double brick. Timber is more susceptible to fire, termite damage, and storm impact, all of which influence how insurers assess the rebuilding risk.

Tile Roof

Tiled roofs are generally viewed favourably by insurers — they're durable and perform well in most weather conditions. However, in cyclone-prone areas, tiles can become projectiles during severe wind events, which is factored into the risk assessment.

Pole Foundation

Homes built on poles (stumps) are common in Queensland and are well-suited to the local environment, offering ventilation and some flood resilience. However, they can also present additional rebuilding complexity, which may slightly influence the sum insured calculation.

Swimming Pool

Pools add to the insurable value of a property and can also introduce liability considerations under a home insurance policy. Expect this to contribute modestly to the overall premium.

Solar Panels

Solar systems are increasingly common on Queensland rooftops, and most insurers now include them as part of the building sum insured. Ensuring your $750,000 building cover adequately accounts for the replacement cost of your solar system is important.

Timber and Laminate Flooring

Flooring type can affect contents and building claims, particularly in water damage scenarios. Timber and laminate floors can be costly to replace, so it's worth confirming your policy covers this adequately.

---

Tips for Homeowners in Taranganba

Whether you're reviewing an existing policy or shopping around for the first time, here are some practical steps worth taking.

1. Check your building sum insured regularly Construction costs have risen significantly in recent years. A 235 sqm home built in 2004 may cost considerably more to rebuild today than it did when you first took out your policy. Use a building cost calculator or speak with a local builder to sense-check your $750,000 sum insured — underinsurance is a real risk in the current environment.

2. Ask about cyclone excess separately Many insurers in Queensland apply a separate, higher excess specifically for cyclone-related claims. This is different from your standard building excess and can sometimes be in the tens of thousands of dollars. Make sure you understand exactly what your policy states before a cyclone season arrives.

3. Review your contents cover annually $100,000 in contents cover is a reasonable starting point, but it's easy for the value of your belongings to creep up over time — especially with solar systems, appliances, and furniture. Do a quick stocktake each year to make sure you're not underinsured on the contents side.

4. Compare quotes before your renewal date Loyalty doesn't always pay in insurance. Premiums can vary significantly between providers for the same level of cover. Shopping around at least 30 days before your renewal gives you time to compare properly without feeling rushed.

---

Ready to Compare?

Whether this quote looks like a good deal or you think you could do better, the best way to know for certain is to compare. Get a home insurance quote at CoverClub and see how multiple providers price your property — it takes just a few minutes and could save you hundreds of dollars a year.