If you own a free standing home in Taree, NSW 2430, you've probably noticed that home insurance premiums can vary quite dramatically — even between neighbouring streets. This article breaks down a real home and contents insurance quote for a three-bedroom weatherboard property in Taree, compares it against local, state, and national benchmarks, and offers practical guidance for getting better value on your cover.

---

Is This Quote Fair?

The annual premium for this quote comes in at $3,234 per year (or $310 per month), covering a building sum insured of $670,000 and contents valued at $50,000, each with a $1,000 excess.

Our price rating for this quote is Expensive — Above Average.

To put that in context, the suburb average for Taree (2430) sits at $2,415 per year, with a median of $2,217. That means this quote is running roughly 34% above the suburb average and about 46% above the median — a meaningful gap that's worth investigating before simply accepting the renewal or going ahead with the first quote you receive.

That said, "expensive" doesn't necessarily mean "wrong." Several features of this particular property — its age, construction type, and added extras like solar panels and a granny flat — can legitimately push premiums higher. We'll unpack those factors below.

---

How Taree Compares

Understanding where Taree sits within the broader insurance landscape helps put individual quotes into perspective.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,234 |

| Taree (2430) Suburb Average | $2,415 |

| Taree (2430) Suburb Median | $2,217 |

| Taree 25th Percentile | $1,489 |

| Taree 75th Percentile | $2,995 |

| Mid-Coast LGA Average | $5,840 |

| NSW State Median | $3,770 |

| National Median | $2,764 |

Based on 158 quotes collected for the Taree 2430 postcode.

A few things stand out here. First, despite this quote feeling expensive relative to the suburb, it actually sits well below the NSW state median of $3,770 and is considerably more affordable than the Mid-Coast LGA average of $5,840 — which is likely skewed by higher-risk coastal and flood-prone properties in the region.

Compared to the national median of $2,764, this quote is about 17% higher, but still within a range that experienced insurers would consider reasonable for a property with the characteristics described.

The 25th percentile figure of $1,489 is worth noting — it shows that some Taree homeowners are paying significantly less. However, those policies may carry different levels of cover, higher excesses, or apply to newer, lower-risk properties. Always compare like for like.

---

Property Features That Affect Your Premium

Several characteristics of this home are likely contributing to the above-average premium. Here's how insurers typically view each one:

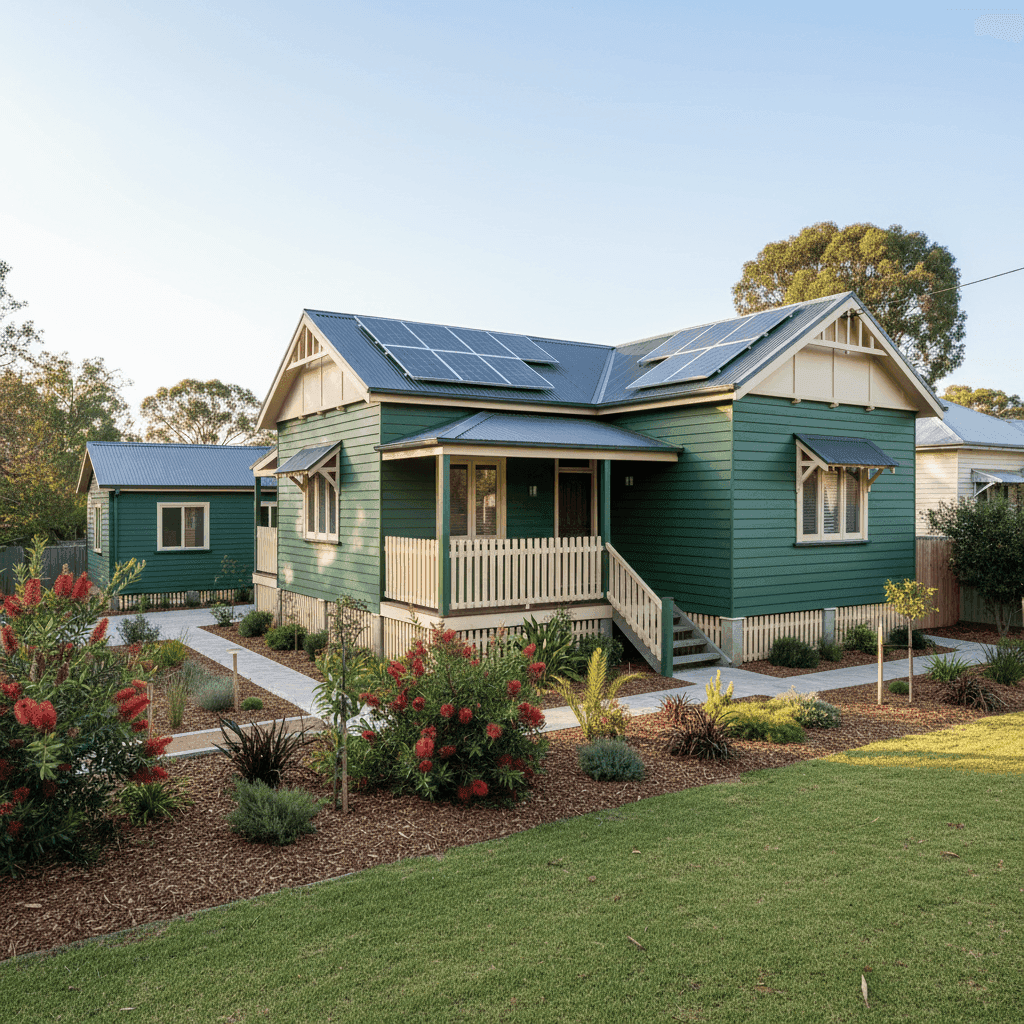

Age of Construction (Built c. 1900)

At over 120 years old, this is a heritage-era property. Older homes present greater risk to insurers because ageing plumbing, wiring, and structural elements are more prone to failure. Rebuilding or repairing period homes is also more expensive, often requiring specialist trades and materials — which is reflected in the $670,000 building sum insured.

Weatherboard Timber Walls

Weatherboard construction is common in older Australian homes and has a certain charm, but timber is more susceptible to fire, termite damage, and moisture-related issues than brick or concrete. Insurers typically apply a loading for timber-framed or clad properties, particularly older ones.

Stump Foundation

Homes on stumps (also called piers) are elevated off the ground, which can be beneficial in flood-prone areas but also introduces specific risks — including subfloor moisture, pest ingress, and structural movement over time. The stump foundation adds a layer of complexity that insurers factor into their pricing.

Solar Panels

Solar panels are an increasingly common addition to Australian homes, but they do add to the replacement cost of a property and can complicate roof-related claims. Their presence on this home is a modest but real contributor to the premium.

Granny Flat

The inclusion of a granny flat increases the insured value of the property and introduces additional liability considerations. Whether the flat is occupied by family or rented out, insurers need to account for the additional structure and its contents.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace and are typically covered under building insurance. Their inclusion adds to the overall replacement cost of the home.

Colorbond Roof

On the positive side, a steel Colorbond roof is one of the more insurer-friendly roofing materials — durable, fire-resistant, and low-maintenance. This may be partially offsetting what could otherwise be an even higher premium.

---

Tips for Homeowners in Taree

1. Shop Around — Seriously

The gap between the 25th and 75th percentile in Taree is enormous ($1,489 vs $2,995). That's not just statistical noise — it reflects real differences in how insurers price the same suburb. Getting two or three competing quotes could save you hundreds of dollars annually. Compare quotes for your Taree property here.

2. Review Your Sum Insured Carefully

A building sum insured of $670,000 for a 130 sqm home works out to roughly $5,150 per square metre — on the higher end, but potentially justified for a heritage property requiring specialist reconstruction. Use a building cost estimator to verify your sum insured is accurate; being over-insured means you're paying more premium than necessary, while being under-insured can leave you seriously exposed at claim time.

3. Consider Raising Your Excess

Both the building and contents excess on this policy sit at $1,000. Opting for a higher excess — say, $2,000 or $2,500 — can meaningfully reduce your annual premium. Just make sure you have that amount readily accessible if you ever need to claim.

4. Bundle and Maintain

Many insurers offer discounts when you combine building and contents cover under one policy (as this quote does) or when you hold multiple policies with the same provider. Additionally, demonstrating that you actively maintain an older home — updated wiring, treated stumps, maintained gutters — can sometimes support a case for a lower premium at renewal.

---

Ready to Find a Better Rate?

Whether this quote is your first or your fifth, it pays to keep comparing. CoverClub makes it easy to see how your premium stacks up against real data from your suburb, your state, and across Australia. Get a home insurance quote for your Taree property today and find out if you're getting the cover you deserve at a price that makes sense.

You can also explore detailed insurance pricing data for Taree (2430), New South Wales, and nationally to benchmark your own situation.