If you own a free standing home in Taree, NSW 2430, you've probably noticed that home insurance isn't cheap — and you may be wondering whether the quote sitting in your inbox is reasonable or whether you're paying too much. This article breaks down a real building insurance quote for a four-bedroom, two-bathroom brick veneer home in Taree, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value.

---

Is This Quote Fair?

The quote in question comes in at $3,352 per year (or $328/month) for building-only cover, with a $1,000 building excess and a sum insured of $719,000. Our price rating for this quote is EXPENSIVE — above average for the Taree area.

To put that in perspective, the suburb average premium for Taree (postcode 2430) sits at $2,415 per year, with a median of $2,217. This quote lands well above both of those figures — roughly 39% above the suburb average and about 51% above the suburb median. Even when you look at the 75th percentile for the area ($2,995/yr), this quote still exceeds it by more than $350.

That said, "expensive" doesn't automatically mean "wrong." Several property-specific factors — which we'll explore below — can legitimately push a premium higher than the local average. The key is understanding why your quote is where it is, so you can make an informed decision rather than simply accepting it.

---

How Taree Compares to the Rest of NSW and Australia

It's worth zooming out to get the full picture. While this quote looks steep against local Taree figures, the broader context tells a more nuanced story.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Taree (2430) | $2,415/yr | $2,217/yr |

| Mid-Coast LGA | $5,840/yr | — |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, the NSW state average of $9,528 is extraordinarily high — this is heavily skewed by expensive coastal and flood-prone properties across the state. The NSW median of $3,770 is a more reliable indicator, and against that figure, this quote of $3,352 actually looks more reasonable.

Nationally, the average sits at $5,347 and the median at $2,764 — meaning this quote is above the national median but well below the national average. For the Mid-Coast LGA, which includes Taree, the average premium is $5,840, making this quote look comparatively modest at the regional level.

You can explore the full breakdown of Taree suburb insurance statistics, NSW state averages, and national home insurance data on CoverClub.

The bottom line: relative to Taree's immediate suburb peers, this quote is on the high side. But relative to the broader Mid-Coast region and NSW as a whole, it's not as alarming as it might first appear.

---

Property Features That Affect Your Premium

Insurance pricing isn't arbitrary — it's driven by the specific characteristics of your home and its location. Here's how the features of this particular property are likely influencing the premium:

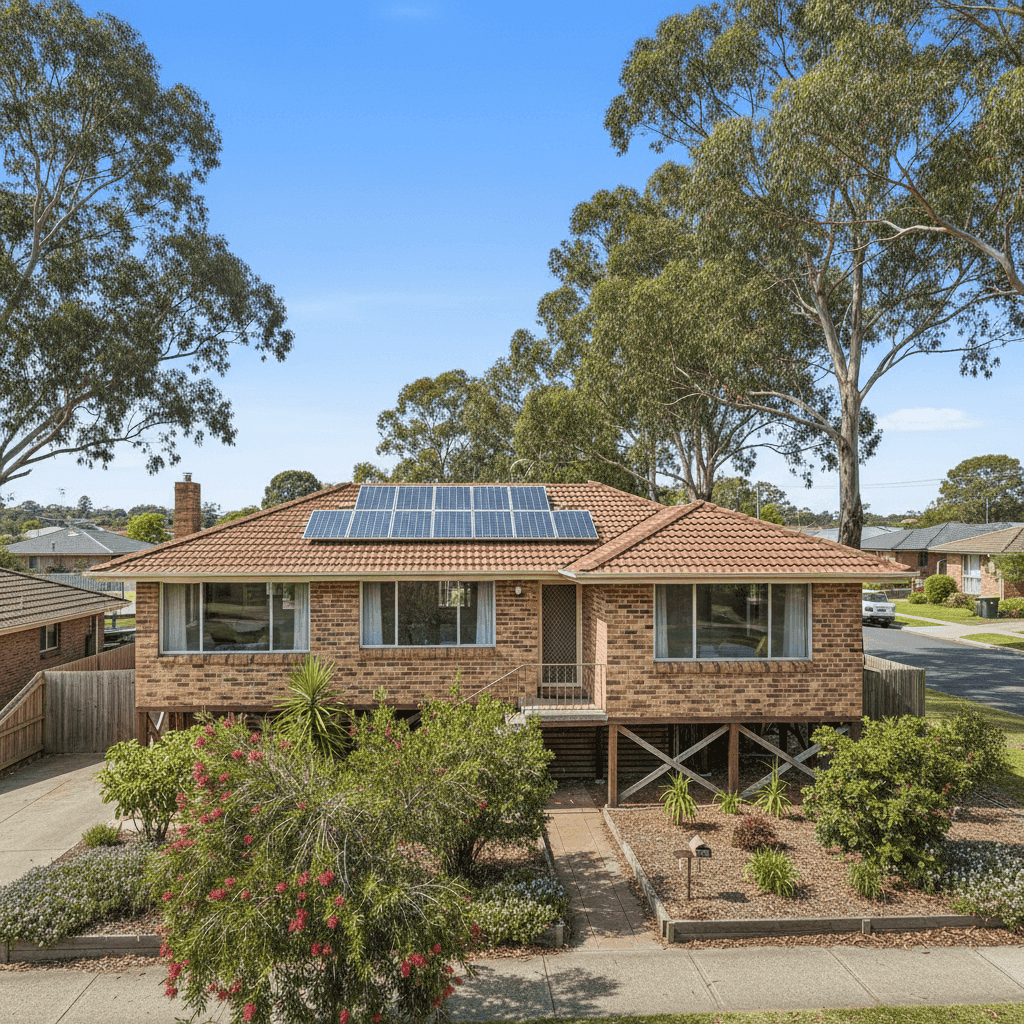

Brick Veneer Walls & Tiled Roof Brick veneer construction with a tiled roof is generally considered a mid-range risk profile. It's more resilient than timber weatherboard but slightly less so than full brick. Tiles are durable but can be more expensive to repair or replace after storm or hail damage compared to Colorbond roofing, which may contribute marginally to the premium.

Stump Foundation Homes built on stumps — as this 1985-era property is — can be more susceptible to movement, particularly in areas with reactive soils or flood risk. Stump foundations may attract slightly higher premiums because of the potential for subsidence, pest damage to stumps, and increased vulnerability during flood events.

Construction Year (1985) A home built in 1985 is approaching 40 years old. Older homes can carry higher premiums because of the increased likelihood of aging infrastructure — think older wiring, plumbing, and roofing materials — that may be more prone to failure or more costly to repair to current building standards.

Solar Panels This property has solar panels installed, which adds to the replacement cost of the building and can slightly increase the sum insured required. Insurers factor in the cost of replacing solar systems, which can run into the tens of thousands of dollars, so it's not unusual to see this reflected in the premium.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset within the home. As part of the building's infrastructure, they contribute to the overall sum insured and can add to the cost of a claim — and therefore the premium.

Sum Insured: $719,000 At 214 sqm, the sum insured of $719,000 works out to roughly $3,360 per sqm — which is on the higher end of typical rebuild costs in regional NSW. It's worth reviewing whether this figure accurately reflects your home's rebuild cost (not market value), as over-insuring can unnecessarily inflate your premium.

Flood & Weather Risk in Taree Taree sits on the Manning River and has a well-documented history of flooding. While this quote is not in a designated cyclone risk zone, flood risk is a significant pricing factor in this region and is very likely contributing to the above-average premium.

---

Tips for Homeowners in Taree

1. Review Your Sum Insured Make sure your building sum insured reflects the actual cost to rebuild — not the market value of your property. Use a professional building cost estimator or ask your insurer how they've calculated the figure. If $719,000 is higher than your true rebuild cost, reducing it could lower your premium meaningfully.

2. Compare Multiple Quotes The single most effective way to reduce your premium is to compare. Based on the suburb data, there's a wide spread between the 25th percentile ($1,489/yr) and the 75th percentile ($2,995/yr) in Taree — meaning some homeowners with similar properties are paying significantly less. Get a comparison quote at CoverClub to see what's available for your specific address.

3. Ask About Flood Cover Options Given Taree's flood history, it's important to understand exactly what flood cover is included in your policy — and at what cost. Some insurers price flood cover separately or allow you to opt out, which can reduce premiums. However, given the genuine risk in this area, removing flood cover entirely is a decision that warrants careful consideration.

4. Consider a Higher Excess If you're in a financial position to absorb a larger out-of-pocket cost in the event of a claim, increasing your excess (say, from $1,000 to $2,000 or more) can reduce your annual premium. Just make sure the saving justifies the additional risk you're taking on.

---

Compare Your Home Insurance Today

Whether this quote is the right one for your home depends on your individual circumstances — but you should never accept the first number you're given. CoverClub makes it easy to compare home insurance quotes from multiple insurers in one place, so you can see exactly where your premium sits and whether there's a better deal available.

Start comparing home insurance quotes for your Taree property →