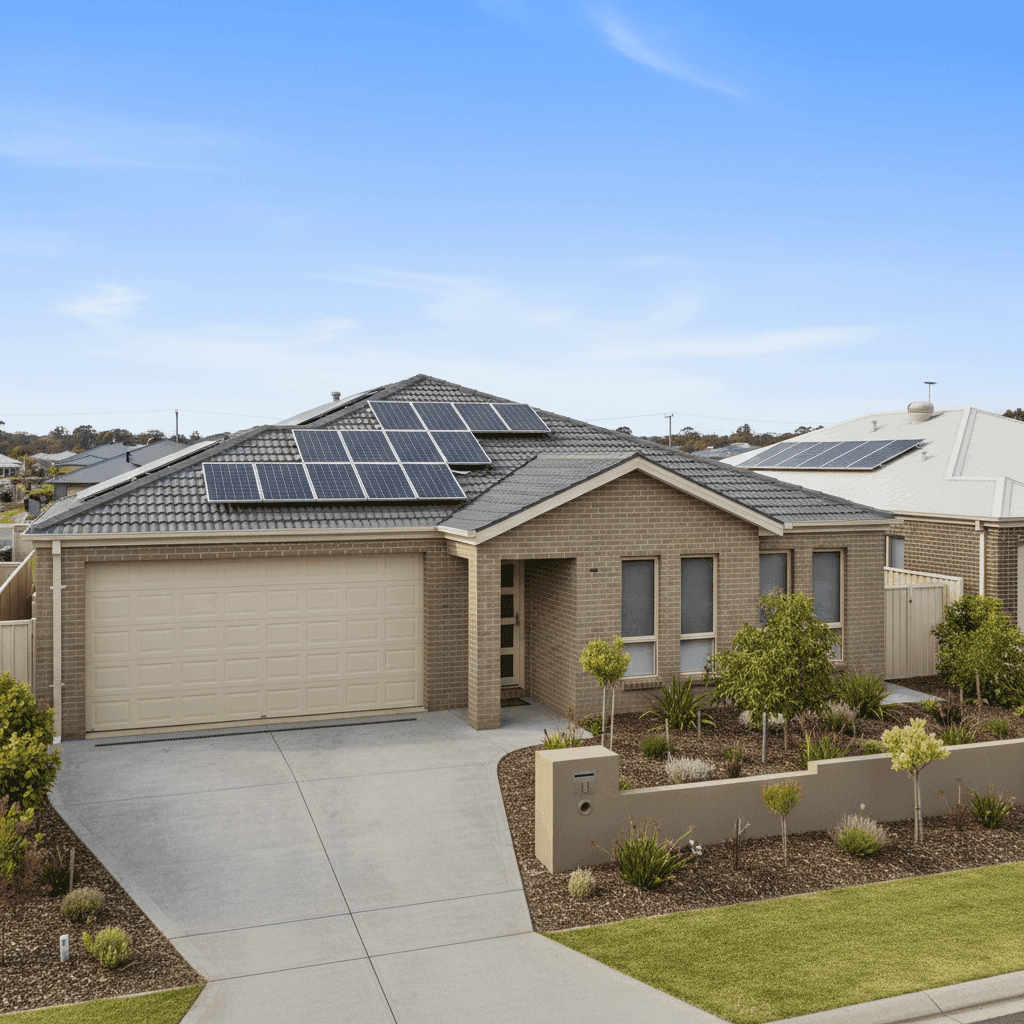

If you own a free standing home in Tea Gardens, NSW 2324, you already know the appeal — a relaxed coastal lifestyle on the shores of Port Stephens, with the Myall River at your doorstep. But like any property, protecting it with the right home insurance is just as important as finding it in the first place. In this article, we take a close look at a recent home and contents insurance quote for a five-bedroom brick veneer home in Tea Gardens, unpacking whether the price is competitive, how it stacks up against local and national benchmarks, and what you can do to make sure you're getting the best deal.

---

Is This Quote Fair?

The quote in question comes in at $2,488 per year (or $238 per month) for combined home and contents cover, with a building sum insured of $550,000 and contents valued at $40,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up.

Based on 113 quotes collected for Tea Gardens (2324), the suburb average premium sits at $3,044 per year, with a median of $2,792. That means this quote is tracking below both the local average and median — a genuinely positive result for the homeowner.

To put it in even sharper context: 25% of Tea Gardens quotes come in at $1,453 or less (the 25th percentile), while 25% exceed $4,056 (the 75th percentile). At $2,488, this quote sits comfortably in the middle band — not the cheapest on the market, but well clear of the expensive end. For a well-appointed five-bedroom home with solar panels and ducted climate control, that's a reasonable outcome.

---

How Tea Gardens Compares

It's worth zooming out to understand just how Tea Gardens fits into the broader insurance landscape across New South Wales and the country as a whole.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Tea Gardens (2324) | $3,044/yr | $2,792/yr |

| NSW State | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Maitland LGA | $13,875/yr | — |

A few things stand out here. The NSW state average of $9,528 is extraordinarily high — heavily skewed by flood-prone and high-risk postcodes elsewhere in the state. The median of $3,770 is a more realistic yardstick for typical NSW homeowners, and Tea Gardens' median of $2,792 sits below even that figure.

Perhaps most striking is the Maitland LGA average of $13,875, which is dramatically higher than Tea Gardens despite both falling within the broader Hunter region. This likely reflects significant flood risk in parts of Maitland, which pushes premiums up considerably. Tea Gardens, by comparison, benefits from a different risk profile.

Against national benchmarks, Tea Gardens also looks favourable. The national average of $5,347 is nearly double the local suburb average, and the national median of $2,764 is broadly in line with what Tea Gardens homeowners are typically paying.

The takeaway: Tea Gardens is a relatively affordable suburb to insure, particularly when compared to other parts of NSW and the Maitland LGA.

---

Property Features That Affect Your Premium

The specific characteristics of this property play a meaningful role in how insurers assess risk and calculate premiums. Here's how the key features of this home factor in:

Brick Veneer Walls Brick veneer is one of the most common and well-regarded construction types in Australia. Insurers generally view it favourably — it offers solid fire resistance and durability without the higher rebuild costs associated with full double-brick construction. This likely contributes to a more competitive premium.

Concrete Tile Roof Concrete roofing is robust and long-lasting, which insurers tend to reward. It performs well in storms and is less susceptible to fire than some other roofing materials, making it a lower-risk choice from an underwriting perspective.

Slab Foundation & Tile Flooring A concrete slab foundation is standard for homes of this era and is generally considered low-risk. Combined with tile flooring throughout, this reduces exposure to water damage claims that can affect homes with timber subfloors or carpet.

Built in 2018 A relatively modern construction year is a significant advantage. Newer homes are built to current Australian Standards, meaning better structural integrity, up-to-date electrical systems, and compliance with contemporary bushfire and wind-load requirements. Insurers often price newer builds more competitively as a result.

Solar Panels The presence of solar panels adds a small degree of complexity to a home insurance policy. Some insurers include panels as part of the building sum insured, while others may treat them separately. It's worth confirming with your insurer that your solar system is explicitly covered — including for storm damage and accidental breakage.

Ducted Climate Control Ducted air conditioning is a fixed installation and is typically covered under the building component of a policy. At $550,000 sum insured, it's important to ensure this figure accounts for the replacement cost of all fixed assets, including the ducted system.

No Pool, No Cyclone Risk Zone The absence of a pool removes a common source of liability and accidental damage claims. And while Tea Gardens is a coastal town, it falls outside designated cyclone risk zones — a factor that keeps premiums lower than they might be for similar properties in Far North Queensland or parts of WA.

---

Tips for Homeowners in Tea Gardens

1. Review your building sum insured regularly Construction costs have risen sharply in recent years. A $550,000 sum insured may have been accurate at the time of purchase, but rebuilding costs in regional NSW have increased. Use a building cost calculator or speak with a quantity surveyor to make sure you're not underinsured.

2. Confirm solar panel coverage As mentioned above, don't assume your solar panels are automatically covered. Ask your insurer directly whether they're included in the building sum insured, and whether there are any exclusions for panel degradation or inverter failure.

3. Shop around at renewal time Insurers often reserve their best pricing for new customers. If you've been with the same provider for several years without comparing, you may be paying a loyalty premium. Use a comparison tool like CoverClub to benchmark your renewal quote against the market.

4. Consider your excess carefully Both the building and contents excess on this policy are set at $1,000. Opting for a higher excess — say $2,000 or $2,500 — can meaningfully reduce your annual premium. If you have a solid emergency fund and a low-risk property, this trade-off is often worth making.

---

Compare Your Home Insurance Options

Whether you're renewing an existing policy or insuring a new purchase, it pays to see what the market has to offer. CoverClub aggregates real quote data from across Australia, so you can see exactly how your premium compares to your neighbours and to homeowners across the country.

Get a home insurance quote for your Tea Gardens property and find out if you're paying a fair price — or if there's a better deal waiting for you.