Teralba is a quiet lakeside suburb on the western shore of Lake Macquarie in New South Wales, known for its older character homes and relaxed semi-rural feel. If you own a free standing home here — particularly one of the area's heritage-era weatherboard properties — understanding what drives your insurance premium can save you a significant amount of money each year. In this analysis, we break down a real home and contents insurance quote for a 3-bedroom, 2-bathroom free standing home in Teralba (postcode 2284), and put the numbers in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $7,473 per year (or $716/month) for combined home and contents cover, with a building sum insured of $884,000 and contents valued at $150,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — Above Average.

To understand why, it helps to look at what other homeowners in the same suburb are paying. The average premium in Teralba sits at around $3,188 per year, with a median of $2,970. This quote is more than double the local median — a significant gap that warrants a closer look.

That said, it's important not to compare apples with oranges. The sum insured here ($884,000 for building alone) is likely considerably higher than many comparable quotes in the suburb sample, which would naturally push the premium up. Higher-value homes with above-average fittings, solar panels, ducted climate control, and heritage listing considerations will always attract a steeper price. Still, even accounting for these factors, the premium lands well above what most Teralba homeowners are paying.

---

How Teralba Compares

Here's how this quote stacks up against broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Teralba (2284) | $3,188/yr | $2,970/yr |

| Lake Macquarie LGA | $11,064/yr | — |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, the NSW average premium of $9,528 is heavily skewed by high-value properties and high-risk areas across the state — the median of $3,770 is a more realistic benchmark for most homeowners. Similarly, the national average of $5,347 is pulled upward by cyclone-prone regions in Queensland and WA, where premiums can be eye-watering.

Interestingly, the Lake Macquarie LGA average of $11,064 is quite high, suggesting that some properties in this local government area — possibly those with flood or storm surge exposure given the lake proximity — are attracting very significant premiums. Teralba's own suburb median of $2,970 is actually quite reasonable by comparison, sitting below both the state and national medians.

At $7,473, this particular quote is above the suburb average but below the LGA and NSW averages — placing it in a middle ground that reflects the specific risk profile and high insured value of this property.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to a higher-than-average premium. Understanding these can help you have more informed conversations with insurers.

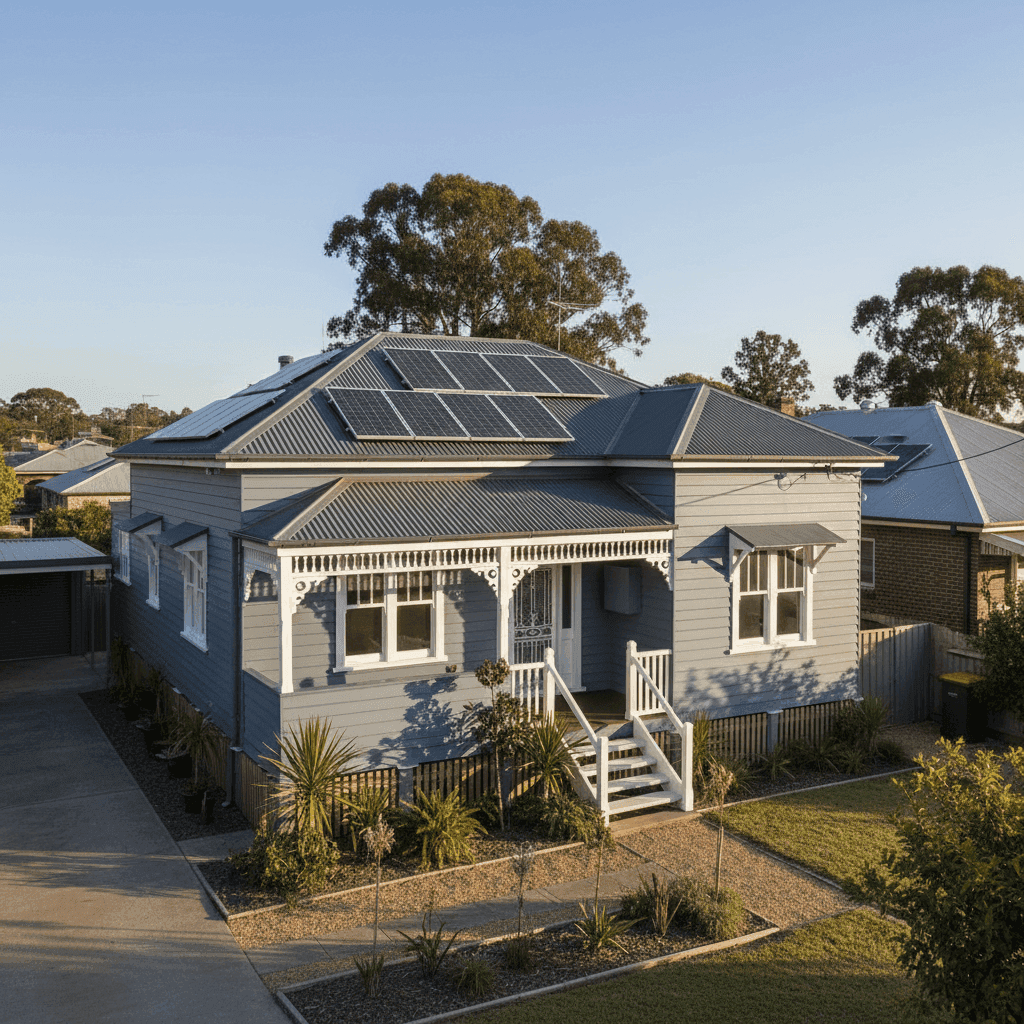

Heritage Listing

This property sits under a heritage overlay, which is one of the more significant premium drivers. Heritage-listed homes often require like-for-like repairs using period-appropriate materials and tradespeople, which can dramatically increase rebuild costs. Insurers price this risk accordingly.

Weatherboard Construction

Weatherboard timber walls are more susceptible to fire, rot, and storm damage compared to brick or rendered masonry. Many insurers view timber-clad homes as higher risk, which is reflected in the premium. Maintaining the cladding in good condition can help manage this risk.

Stump Foundation & Timber Flooring

The home sits on stumps and features timber and laminate flooring — a classic combination in older Australian homes. Stumped foundations can be vulnerable to movement, moisture, and pest damage. Insurers factor in the additional exposure that comes with this style of construction.

Age of the Property (Built 1930)

At nearly 100 years old, this home's age is a notable factor. Older homes may have outdated wiring, plumbing, or structural elements that increase the likelihood and cost of a claim. The 1930 construction year alone can trigger higher loadings with many insurers.

Solar Panels & Ducted Climate Control

The presence of solar panels and a ducted climate control system increases the replacement cost of the home's fixtures and fittings. These are valuable assets, but they add to the overall sum insured and the cost to rebuild or repair.

Above-Average Fittings

With above-average fittings quality, the interior of this home — think stone benchtops, quality appliances, and premium fixtures — would cost more to replace than a standard fit-out. This is appropriately reflected in both the building sum insured and the premium.

Slight Elevation

The home is elevated by less than 1 metre, which can offer a minor degree of protection against surface flooding, though it's unlikely to significantly reduce the premium on its own.

---

Tips for Homeowners in Teralba

1. Shop around — seriously. With this quote sitting well above the local suburb median, it's worth getting multiple quotes. Insurers assess heritage properties and older construction very differently, and the spread between the cheapest and most expensive quotes for a home like this can be thousands of dollars. Use CoverClub to compare quotes side by side.

2. Review your sum insured carefully. A building sum insured of $884,000 is substantial. Make sure this figure reflects the actual cost to rebuild — not the market value of the property. Overinsuring is a common mistake that inflates premiums unnecessarily. Consider getting a professional building replacement cost assessment, especially for a heritage home where rebuild costs can be complex to estimate.

3. Maintain your weatherboard cladding. Keeping your timber cladding painted, sealed, and free from rot or pest damage demonstrates to insurers that the property is well-maintained. Some insurers offer better rates for homes in good condition, and it reduces the risk of a claim in the first place.

4. Ask about heritage-specific policies. Not all insurers handle heritage properties equally. Some specialist insurers offer policies tailored to older and heritage-listed homes, which may provide better coverage at a more competitive price than a standard policy from a major insurer. It's worth asking the question.

---

Compare Your Home Insurance Today

Whether you're renewing your policy or shopping for the first time, it pays to compare. CoverClub makes it easy to see how your premium stacks up against other homeowners in Teralba and across NSW. Get a quote today and find out if you're getting a fair deal — or if there's a better option waiting for you.