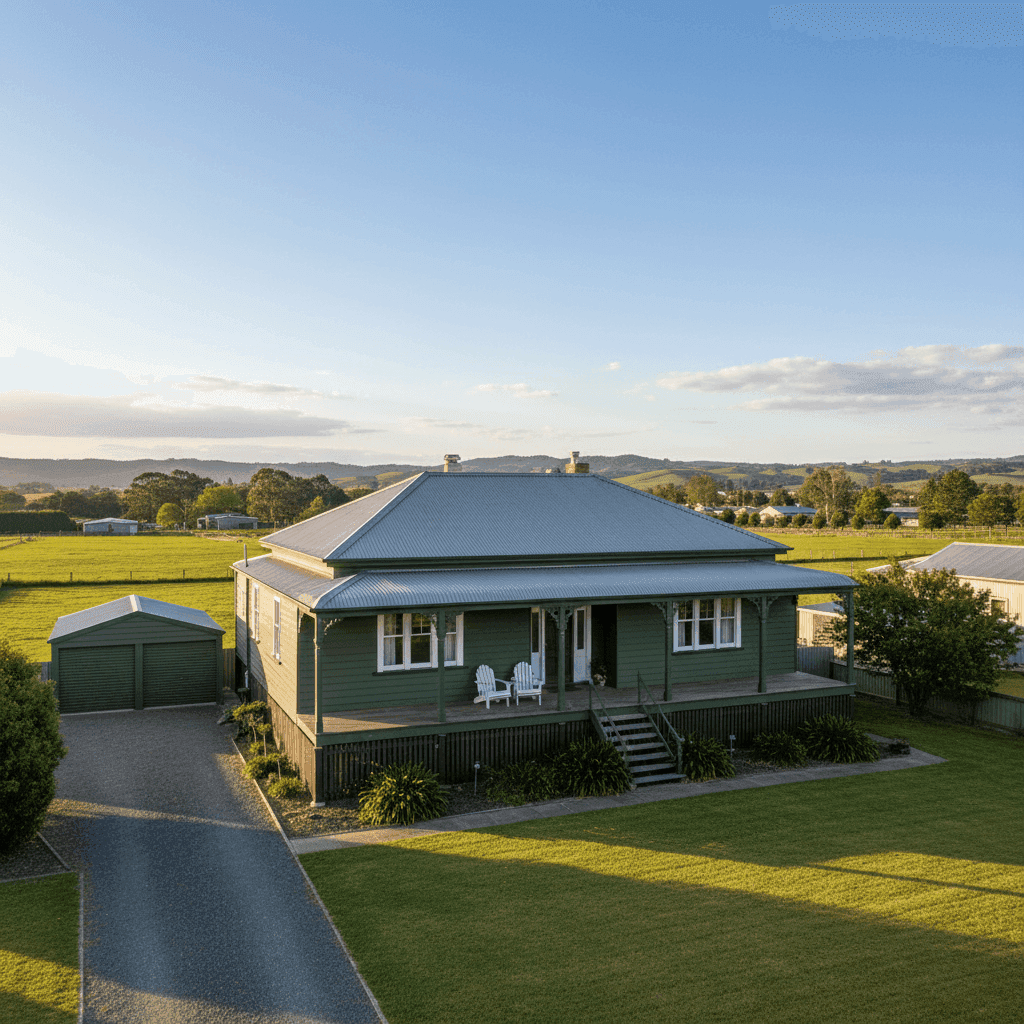

If you own a free standing home in Terang, VIC 3264, you've probably noticed that home insurance premiums can vary wildly depending on who you ask. This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom weatherboard property in Terang — and puts that number into context against suburb, state, and national benchmarks. Whether you're shopping around for the first time or reviewing your existing policy, read on to see what's driving the cost and where you might find savings.

---

Is This Quote Fair?

The quote in question comes in at $2,564 per year (or $246 per month) for combined home and contents cover, with a building sum insured of $860,000 and contents valued at $32,000. Both the building and contents excess are set at $5,000.

Our price rating for this quote is Expensive — above average for the Terang area.

To understand why, it helps to look at the local data. The suburb average premium for Terang (3264) sits at just $1,305 per year, with a median of $1,282. This quote is nearly double the local median — a significant gap that warrants a closer look.

That said, context matters. The building sum insured here is $860,000, which is likely higher than many comparable properties in the area. A higher replacement value directly increases the premium, since the insurer is on the hook for more in the event of a total loss. The property's age (built in 1905), elevated foundation on stumps, and weatherboard timber construction are also factors that push premiums upward — more on those shortly.

---

How Terang Compares

Here's how this quote stacks up across different geographic benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Terang (3264) | $1,305/yr | $1,282/yr |

| LGA: Moyne | $2,351/yr | — |

| Victoria | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. Terang's local premiums are relatively modest compared to both the Victorian state average and the national average. This reflects the area's generally lower risk profile — no cyclone zone, lower population density, and a rural/regional setting that typically sees fewer claims than metropolitan areas.

At the LGA level, the Moyne average of $2,351 is a more relevant comparison for this specific property, and our quote of $2,564 sits only modestly above that figure. So while it's expensive relative to the Terang suburb sample, it's not dramatically out of step with the broader Moyne council area — suggesting the property's specific characteristics, rather than location alone, are doing much of the heavy lifting on price.

It's also worth noting the suburb sample size is 19 quotes, which is a reasonably small dataset. Premiums can vary considerably based on individual property features, insurer appetite, and the level of cover selected.

---

Property Features That Affect Your Premium

This particular property has several characteristics that insurers treat as higher risk — and price accordingly.

Heritage-Era Construction (1905)

A home built in 1905 is over 120 years old. While many Federation-era homes are beautifully maintained, insurers consider age a risk factor due to older wiring, plumbing, and structural materials that may be more susceptible to damage or harder to replace. Rebuilding costs for period homes can also exceed those of modern construction, which partly justifies the higher sum insured.

Weatherboard Timber Walls

Weatherboard is a classic Australian building material, but timber external walls carry a higher fire risk rating than brick or rendered masonry. This is reflected in most insurers' pricing models, particularly in regional Victoria where grassfire risk can be a seasonal concern.

Elevated on Stumps

The property sits elevated by at least one metre on stump foundations — a common design in older Australian homes. While elevation can actually reduce flood risk (a positive), stumped homes introduce other considerations: subfloor ventilation issues, potential for pest damage, and structural movement over time. Some insurers apply a loading for this construction type.

Steel/Colorbond Roof

On the positive side, a Colorbond steel roof is generally viewed favourably by insurers. It's durable, low-maintenance, and performs well in wind events compared to terracotta tiles. This is one feature that likely keeps the premium lower than it might otherwise be.

Ducted Climate Control

The presence of ducted climate control adds to the replacement value of the home, which can marginally influence the building sum insured calculation.

No Pool, No Solar

The absence of a pool and solar panels removes two common sources of additional premium loading, keeping things a little simpler from an underwriting perspective.

---

Tips for Homeowners in Terang

1. Review Your Building Sum Insured Carefully

At $860,000, the building sum insured is the single biggest driver of this premium. It's worth getting an independent building replacement cost estimate — not a market value appraisal — to confirm this figure is accurate. Over-insuring is a common (and costly) mistake, but so is under-insuring, which can leave you exposed at claim time.

2. Consider a Higher Excess to Reduce Premiums

Both the building and contents excess are set at $5,000 — already on the higher side. If cash flow allows, some insurers offer further premium reductions for even higher voluntary excesses. Crunch the numbers to see if the trade-off makes sense for your situation.

3. Compare Multiple Insurers — Especially for Older Homes

Not all insurers price heritage or timber-framed homes the same way. Some specialise in older properties and offer more competitive rates; others apply heavy loadings. Shopping around — particularly through a comparison platform — can surface meaningfully different quotes for the same level of cover.

4. Maintain Your Home's Condition

For older weatherboard homes, ongoing maintenance is both a safety imperative and an insurance consideration. Keeping your subfloor clear, maintaining gutters, and ensuring electrical systems are up to code can reduce your risk profile and may support a better premium at renewal. Some insurers also ask about maintenance history during the application process.

---

Compare Your Quote at CoverClub

Wondering if you can do better? CoverClub makes it easy to compare home and contents insurance quotes from multiple Australian insurers in one place. Whether you're in Terang or anywhere else across Victoria, you can get a personalised quote in minutes and see exactly how your premium stacks up. Don't pay more than you need to — start comparing today.