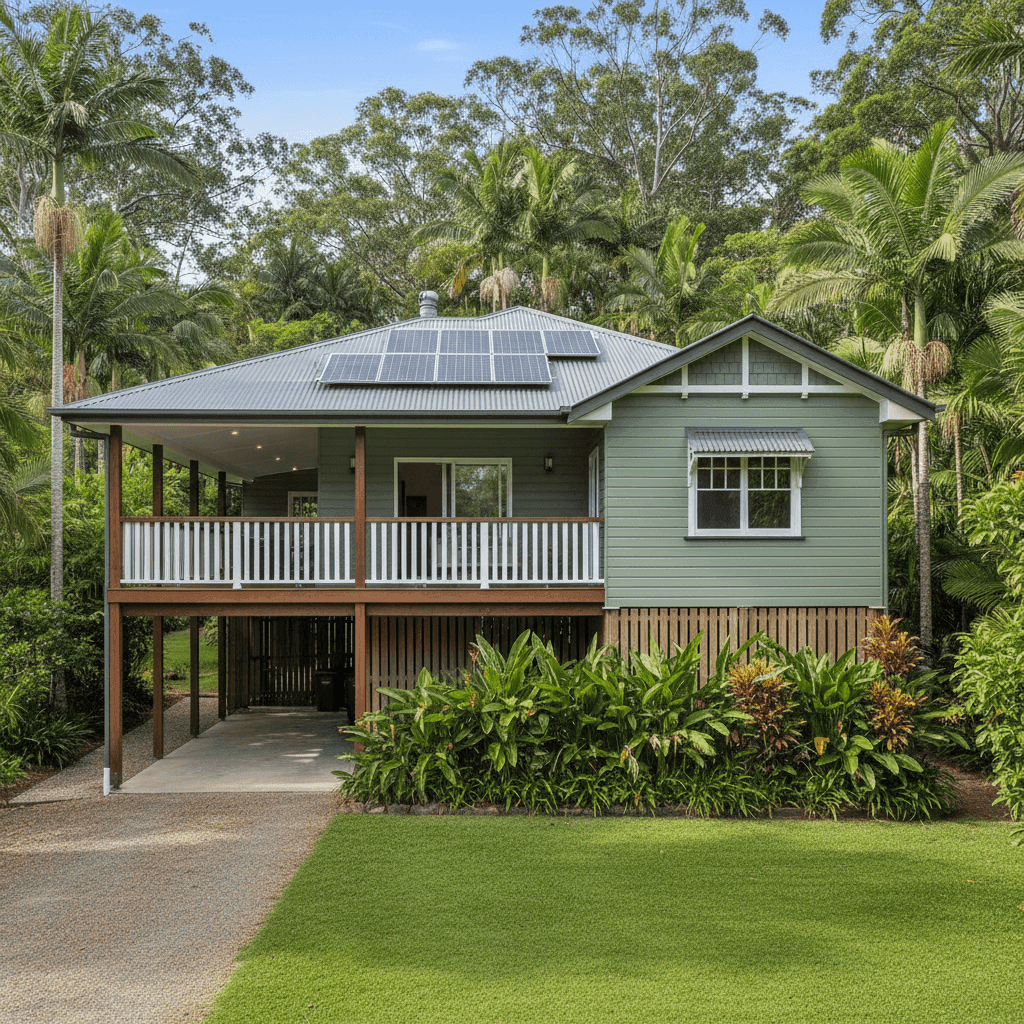

Tucked away in the lush hinterland of northern New South Wales, The Pocket (postcode 2483) is a quiet, semi-rural community near the Tweed Valley. It's the kind of place where character homes sit among rainforest and rolling hills — and the property we're examining today is a fine example: a four-bedroom, two-bathroom free-standing home built in 1979, clad in weatherboard timber and sitting elevated on poles beneath a Colorbond steel roof. While the setting is idyllic, the cost of insuring a home like this is anything but modest. Let's unpack what's driving this premium and whether it represents fair value.

---

Is This Quote Fair?

The annual premium on this quote comes in at $8,737 per year (or $856/month), with a building sum insured of $952,000 for building-only cover. Our price rating for this quote is Expensive — Above Average.

To put that into perspective: the suburb average for The Pocket sits at $4,113 per year, with a median of $3,740. This quote is more than double the local median, which is a significant gap by any measure. Even at the 75th percentile — meaning 75% of comparable quotes in the area are cheaper — the figure is $4,429/yr, still less than half of what's being quoted here.

So yes, on the face of it, this premium is steep. But context matters. The property has a number of characteristics that individually and collectively push premiums upward, and we'll explore each of those below. The key question for any homeowner isn't just "is this expensive?" — it's "is this the best available price for this specific property?" That's exactly where comparison shopping becomes essential.

---

How The Pocket Compares

Understanding where your premium sits relative to broader benchmarks helps frame the conversation:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| The Pocket (2483) | $4,113/yr | $3,740/yr |

| Tweed LGA | $4,680/yr | — |

| NSW State | $3,801/yr | $3,410/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out here. First, The Pocket is already a more expensive suburb to insure than the NSW state average — reflecting the region's elevated flood and storm risk profile. The Tweed LGA average of $4,680/yr is the highest benchmark in this table, suggesting that insurers broadly view this part of the state as higher risk. And when you zoom out to the national picture, the gap widens further — the national median is $2,716/yr, meaning homeowners in The Pocket are already paying roughly 38% more than the typical Australian.

It's worth noting that the suburb sample size here is six quotes — a relatively small dataset. As more data flows in, these averages may shift. Still, the directional signal is clear: this is a premium-priced area, and this particular quote sits well above even local norms.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to the elevated premium. Here's a breakdown of the key risk factors insurers are pricing in:

Elevated on Poles (Pole/Stump Foundation)

Homes built on poles — common in the hinterland and coastal ranges of northern NSW — are often associated with older construction methods and can be more expensive to repair or rebuild following storm or wind damage. While elevation can actually reduce flood risk, the structural complexity of a pole-frame home typically increases rebuild costs, which flows through to the sum insured and the premium.

Weatherboard Timber Exterior

Timber-clad homes are more susceptible to fire, rot, and termite damage compared to brick or rendered masonry. Insurers factor in the higher rebuild and repair costs associated with timber construction, particularly for older homes like this one (built in 1979), where materials may be harder to source and tradespeople more specialised.

High Sum Insured ($952,000)

The building sum insured is the single largest driver of any building insurance premium. At $952,000, this reflects the above-average fittings quality and the 214 sqm floor area. Larger, well-appointed homes cost significantly more to rebuild — and the premium scales accordingly. It's worth periodically reviewing your sum insured with a quantity surveyor to ensure you're not over- or under-insured.

Above-Average Fittings Quality

Kitchens, bathrooms, and finishes that sit above the standard market level are more costly to reinstate. Insurers apply a loading for homes with premium fixtures, stone benchtops, quality flooring, and high-end appliances — all of which are implied by the "above average" fittings classification.

Timber and Laminate Flooring

Combined with the elevated construction, timber flooring adds to the material replacement cost in a claim scenario, particularly if water ingress or storm damage affects the subfloor.

Solar Panels

Solar panels are increasingly common but do add a layer of complexity to claims — particularly for roof damage. Replacement, reinstallation, and potential electrical work can add thousands to a claim, and many insurers factor this into their pricing.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace and are typically included in the building sum insured. Their presence can nudge premiums slightly upward.

---

Tips for Homeowners in The Pocket

If you own a home in this area — or one with similar characteristics — here are some practical steps to help manage your insurance costs:

- Shop the market every renewal. Insurer pricing algorithms vary enormously, and the gap between the cheapest and most expensive quote for the same property can be thousands of dollars. Don't let your policy auto-renew without checking alternatives. Start a comparison at CoverClub to see what's available for your address.

- Review your sum insured with a professional. A quantity surveyor or building estimator can give you an accurate rebuild cost estimate. Many homeowners are significantly over-insured — paying premiums on a sum insured that exceeds what it would actually cost to rebuild. Equally, being under-insured can leave you seriously exposed, so get the number right.

- Consider your excess strategy. This quote carries a $2,000 building excess. Opting for a higher voluntary excess can reduce your annual premium, sometimes meaningfully. If you have the financial buffer to absorb a larger out-of-pocket cost in a claim, this trade-off can make sense over the long run.

- Maintain your home proactively. Insurers reward well-maintained properties — and older weatherboard homes in hinterland settings benefit greatly from regular upkeep. Keep gutters clear, check for signs of timber decay or pest activity, and ensure your roof and pole foundations are inspected periodically. Some insurers also offer discounts for documented maintenance or security upgrades.

---

Compare Your Options with CoverClub

Whether this quote is the right one for your home depends on what else is available in the market. CoverClub makes it easy to compare home insurance quotes side by side, so you can see exactly how different insurers price a property like yours — and make a confident, informed decision. Get a quote for your address today and find out if you could be paying less.