Thornbury is one of Melbourne's most character-rich inner-north suburbs — a lively mix of 1930s weatherboard cottages, converted warehouses, and a High Street buzzing with cafés and independent retailers. If you own a free standing home here, you'll know that protecting it is a serious priority. But are you paying a fair price for your home and contents insurance? This article breaks down a real quote for a 3-bedroom, 2-bathroom home in Thornbury (VIC 3071) and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium in question comes in at $2,526 per year (or $242/month) for a combined home and contents policy, covering a building sum insured of $900,000 and contents valued at $248,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — Above Average.

That label isn't arbitrary. Based on a sample of 25 quotes from the Thornbury area, the suburb average sits at $1,643/yr and the median at $1,467/yr. This quote lands above the 75th percentile threshold of $2,043/yr, meaning it's pricier than at least three-quarters of comparable quotes in the same postcode.

That said, context matters. The building sum insured here is a substantial $900,000 — a figure that reflects both the property's size and the premium construction quality of an above-average-fitted home. Higher replacement costs naturally push premiums up, so the "expensive" rating doesn't necessarily mean the policy is poor value — it may simply reflect the level of cover being sought.

---

How Thornbury Compares

Understanding where your premium sits relative to broader benchmarks is one of the most useful things you can do as a homeowner. Here's how this quote stacks up:

| Benchmark | Premium |

|---|---|

| This Quote | $2,526/yr |

| Thornbury Suburb Average | $1,643/yr |

| Thornbury Suburb Median | $1,467/yr |

| Thornbury 25th Percentile | $1,213/yr |

| Thornbury 75th Percentile | $2,043/yr |

| Darebin LGA Average | $1,622/yr |

| VIC State Average | $3,000/yr |

| VIC State Median | $2,718/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. While this quote is above the Thornbury suburb average, it actually comes in below both the Victorian state average ($3,000/yr) and the national average ($5,347/yr). Viewed through that wider lens, the premium is arguably reasonable — particularly given the high building sum insured and the above-average fittings quality.

The Victorian state average of $3,000/yr reflects the diverse risk profile across the state, from flood-prone regional areas to bushfire-exposed outer suburbs. Thornbury, being an established inner-urban suburb, generally benefits from lower natural disaster risk compared to many parts of Victoria. Meanwhile, the national average of $5,347/yr is heavily skewed by high-risk areas in Queensland and Northern Australia, making it a less relevant comparison for Melbourne homeowners.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful influence on what insurers charge. Understanding them helps you make sense of your premium — and potentially negotiate a better deal.

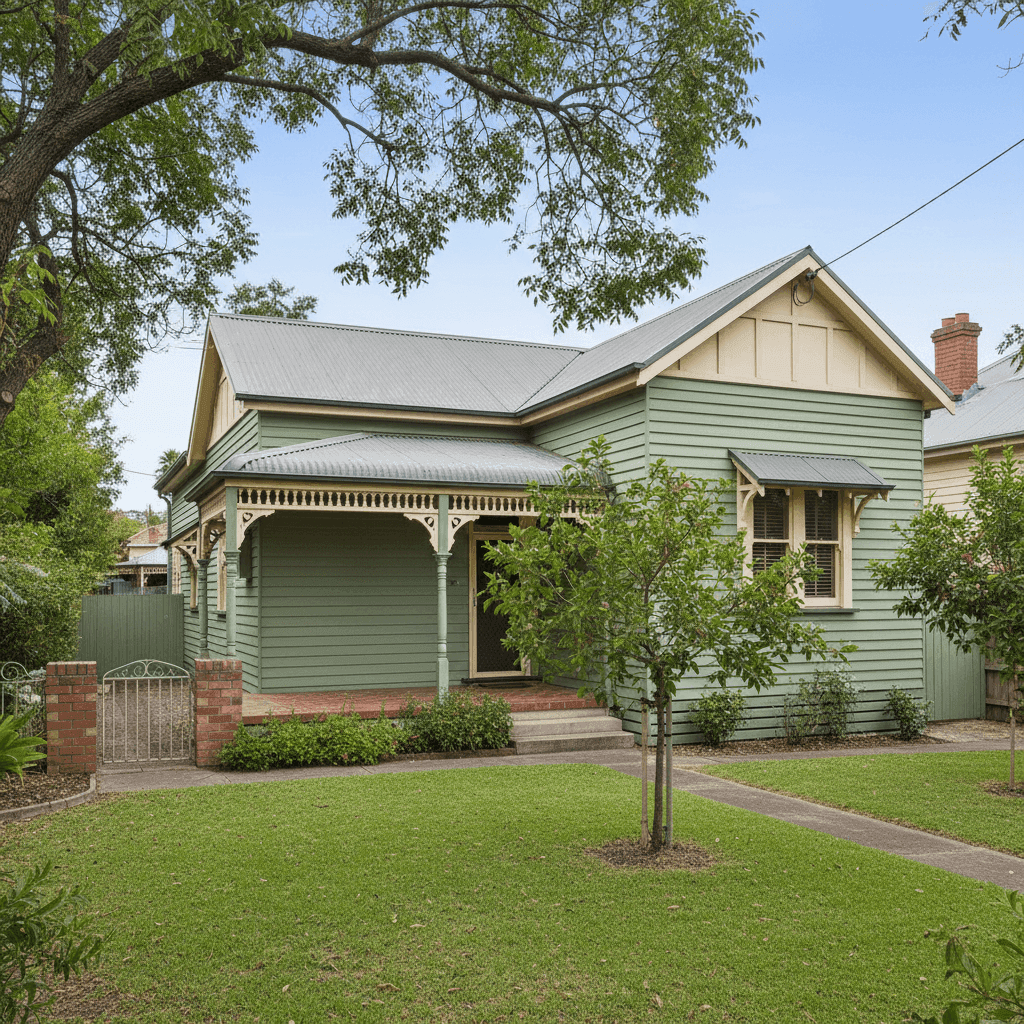

Weatherboard Timber Construction

This home features weatherboard wood external walls, which is extremely common in Thornbury's pre-war housing stock. Timber-clad homes are generally considered a higher risk by insurers than brick veneer or full brick, primarily due to greater susceptibility to fire spread and moisture damage. Expect this to be a contributing factor in the premium calculation.

Stump Foundation

The property sits on stumps, a foundation type typical of homes built in the 1930s across Melbourne's inner suburbs. Stumped homes can be more vulnerable to subsidence, movement, and pest damage over time. Insurers factor in foundation type when assessing structural risk, and stumps can attract slightly higher premiums compared to concrete slab foundations.

Age of Construction — 1936

At nearly 90 years old, this is a heritage-era home. Older properties can be more expensive to rebuild or repair to modern standards, which is reflected in a higher sum insured. Insurers also recognise that ageing electrical, plumbing, and roofing systems can increase the likelihood of a claim.

Steel / Colorbond Roof

On the positive side, the Colorbond steel roof is a modern, durable material that performs well in Australian conditions. It's resistant to fire, corrosion, and high winds — factors that can work in your favour when insurers assess risk.

Ducted Climate Control

The presence of ducted climate control adds to the replacement value of the home, contributing to the higher building sum insured. It's worth ensuring this system is explicitly covered under your policy.

Above-Average Fittings Quality

Above-average fittings — think stone benchtops, quality appliances, and premium fixtures — increase the cost to rebuild or restore the home to its current standard. This is a key driver of the $900,000 building sum insured and, by extension, the premium.

---

Tips for Homeowners in Thornbury

Whether you're reviewing an existing policy or shopping around for the first time, here are four practical steps to make sure you're getting the best deal.

1. Don't underinsure — but don't overinsure either. With a building sum insured of $900,000, it's important to verify that figure reflects the actual cost to rebuild your home (not its market value). Use a building cost calculator or engage a quantity surveyor to confirm your sum insured is accurate. Overinsuring means paying unnecessarily high premiums; underinsuring leaves you exposed when it matters most.

2. Shop around at renewal time. Insurers often reserve their best rates for new customers. If your policy is coming up for renewal, use a comparison platform like CoverClub to see what other providers are offering for the same level of cover. Even a few minutes of comparison shopping can save you hundreds of dollars a year.

3. Consider your excess level. Both excesses on this policy are set at $1,000. Opting for a higher voluntary excess can reduce your annual premium — but make sure you can comfortably cover that amount out of pocket if you need to make a claim. It's a balancing act worth revisiting each year.

4. Maintain your home proactively. For an older weatherboard home on stumps, regular maintenance is both a practical necessity and an insurance consideration. Keeping gutters clear, treating for termites, maintaining the roof, and ensuring your electrical wiring is up to code can reduce your risk profile — and may support a case for a lower premium when you next renew or switch providers.

---

Ready to Compare?

Whether this quote looks like a fair deal or feels a little steep, the best way to know for certain is to compare. At CoverClub, you can get home and contents insurance quotes tailored to your property in Thornbury — and see how they stack up against real data from your suburb and beyond. Explore the Thornbury suburb stats to see what your neighbours are paying, and make a more informed decision about your cover today.