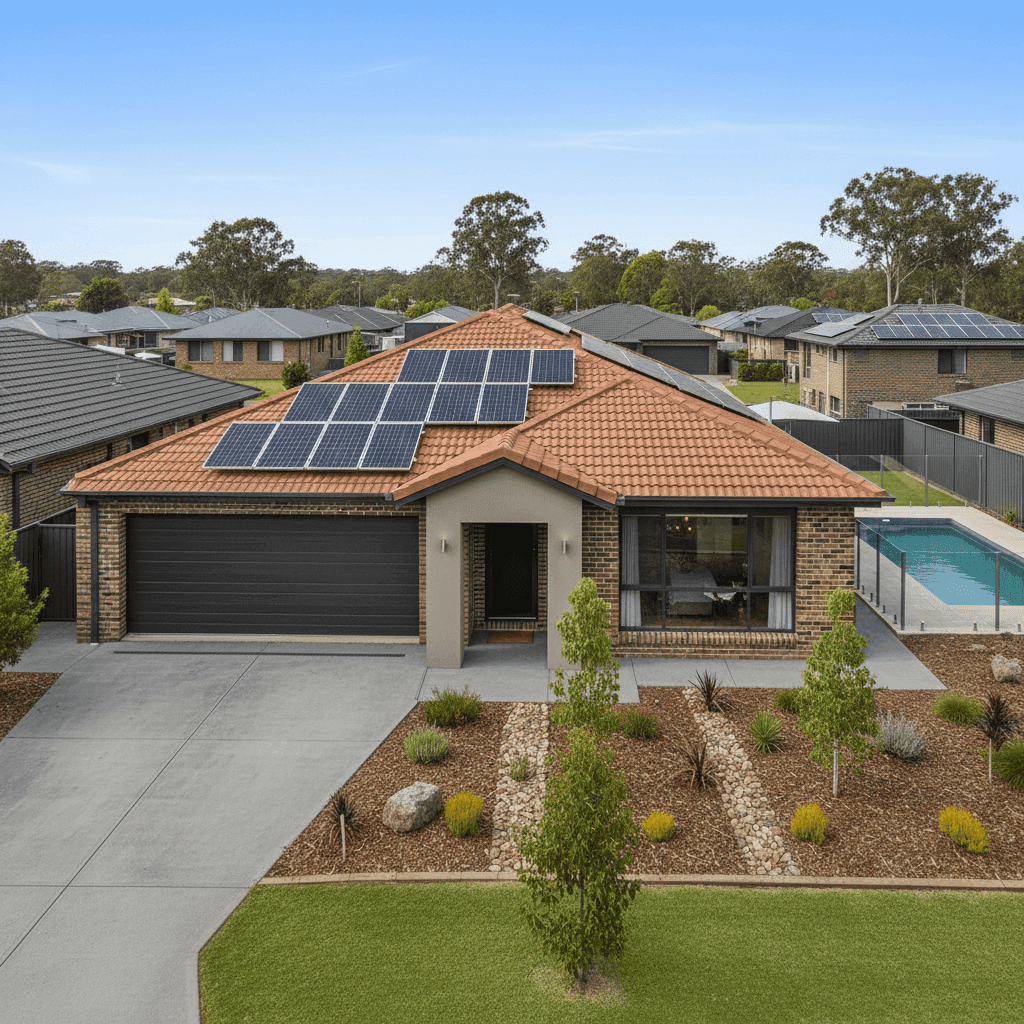

Thornlands is a well-established residential suburb on the southern end of the Redland City coastline, known for its family-friendly streets, proximity to the bay, and a strong mix of modern and mid-2000s housing stock. If you own a free standing home here, understanding what you should expect to pay for home and contents insurance — and why — can save you hundreds of dollars a year. This article breaks down a real quote for a four-bedroom, two-bathroom brick veneer home in Thornlands, and puts the numbers in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $3,053 per year (or $293/month) for combined home and contents cover, with a building sum insured of $852,000 and contents valued at $122,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Based on 60 quotes collected for Thornlands (postcode 4164), the suburb average sits at $2,654/yr and the median at $2,544/yr. At $3,053, this quote lands in the upper half of the local range — above the median, but well below the 75th percentile of $3,557/yr.

In other words, roughly 25–30% of Thornlands homeowners are paying more than this quote, while the majority are paying somewhat less. It's not a bargain, but it's not an outlier either. Given the property's size (244 sqm), features like a pool and solar panels, and the relatively high building sum insured, a premium sitting above the suburb median is entirely understandable.

---

How Thornlands Compares

One of the most striking things about this quote is how it looks when you zoom out to Queensland-wide data.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Thornlands (4164) | $2,654/yr | $2,544/yr |

| Redland LGA | $3,178/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

The Queensland state average of $9,129/yr is eye-watering — heavily skewed by high-risk cyclone and flood-prone areas in North Queensland and Far North Queensland. The median of $3,903/yr is a more representative figure for most Queenslanders, and this quote at $3,053 sits comfortably below that.

Compared to national figures, the story is similar. The national average of $5,347/yr is inflated by catastrophe-prone regions, but even against the national median of $2,764/yr, this Thornlands quote is only modestly higher — a reasonable outcome for a larger-than-average home with several premium features.

At the Redland LGA level, the average is $3,178/yr, meaning this quote is actually slightly below the broader local government area average — a positive sign for the policyholder.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated. Here's how they stack up:

Brick Veneer Walls & Tiled Roof Brick veneer construction with a tiled roof is generally regarded as a solid, mid-range risk profile by insurers. It's more resilient than timber weatherboard and less expensive to rebuild than full double-brick, making it a common and relatively insurer-friendly combination in southeast Queensland.

Concrete Slab Foundation A slab-on-ground foundation is standard for homes of this era in Queensland and carries no particular premium loading. It also reduces the risk of subsidence-related claims compared to older pier-and-beam designs.

Swimming Pool A pool increases the replacement and liability risk associated with a property, which typically results in a modest premium uplift. Pools require accurate inclusion in your sum insured to avoid being underinsured for any structural damage.

Solar Panels Solar panels are an increasingly common feature on Queensland homes and are generally covered under building insurance. However, they do add to the replacement cost, and insurers factor this into the building sum insured calculation. At 244 sqm with a full solar system, the $852,000 building sum insured appears appropriately calibrated.

Ducted Climate Control Ducted air conditioning is a fixed building fixture and contributes to the overall rebuild cost. Like solar panels, it's typically covered under building insurance and is reflected in the sum insured rather than attracting a separate loading.

No Cyclone Risk Thornlands is not classified as a cyclone risk area, which is a meaningful advantage for homeowners in this part of Queensland. Properties in North Queensland can face cyclone-related loadings that dramatically increase premiums — sometimes doubling or tripling the base cost. Being outside this zone keeps the Thornlands premium profile far more manageable.

Standard Fittings With standard-quality fittings, there's no luxury or high-specification loading applied to this property. Homes with premium finishes (stone benchtops throughout, imported tiles, custom joinery) can attract higher rebuild cost estimates and therefore higher premiums.

---

Tips for Homeowners in Thornlands

1. Review Your Building Sum Insured Annually Construction costs in southeast Queensland have risen significantly in recent years. A sum insured of $852,000 for a 244 sqm home built in 2005 appears reasonable today, but it's worth checking against a current building cost calculator each year at renewal. Being underinsured — even by 10–15% — can result in proportional claim payouts rather than full replacement.

2. Compare Quotes Before Renewing The spread of premiums in Thornlands is wide — from $1,607/yr at the 25th percentile to $3,557/yr at the 75th percentile. That's a $1,950 gap between the cheapest and most expensive quarter of the market. Shopping around at renewal, rather than simply accepting the automatic renewal offer, could yield meaningful savings. Get a comparison quote at CoverClub to see where you stand.

3. Check Your Contents Coverage Is Realistic A $122,000 contents value is a common starting point, but it's easy to underestimate the true replacement cost of everything inside your home — furniture, appliances, clothing, electronics, and valuables. Do a room-by-room audit every couple of years to make sure your contents sum insured keeps pace with what you actually own.

4. Ask About Discounts for Security and Safety Features Many insurers offer discounts for homes with monitored alarm systems, deadbolts, and smoke detectors. If your home has these features and they weren't factored into your quote, it's worth asking your insurer directly — or switching to one that rewards them.

---

Ready to See What You Could Pay?

Whether you're reviewing an existing policy or shopping for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. CoverClub makes it easy to see real premium estimates for your specific property in Thornlands — no obligation, no jargon.

Get your personalised home insurance quote at CoverClub →

You can also explore detailed premium data for your area on the Thornlands suburb stats page or browse Queensland-wide insurance trends to see how your postcode fits into the bigger picture.