If you own a free standing home in Thornton, NSW 2322, you've probably wondered whether you're paying a fair price for home and contents insurance — or whether you could be doing better. Thornton is a well-established residential suburb in the Hunter Valley region, sitting within the City of Cessnock LGA, and it attracts a wide range of homeowners thanks to its family-friendly streets and relative affordability compared to the Greater Newcastle area. In this article, we break down a real home insurance quote for a six-bedroom property in the suburb and compare it against local, state, and national benchmarks to help you understand what "good value" actually looks like.

---

Is This Quote Fair?

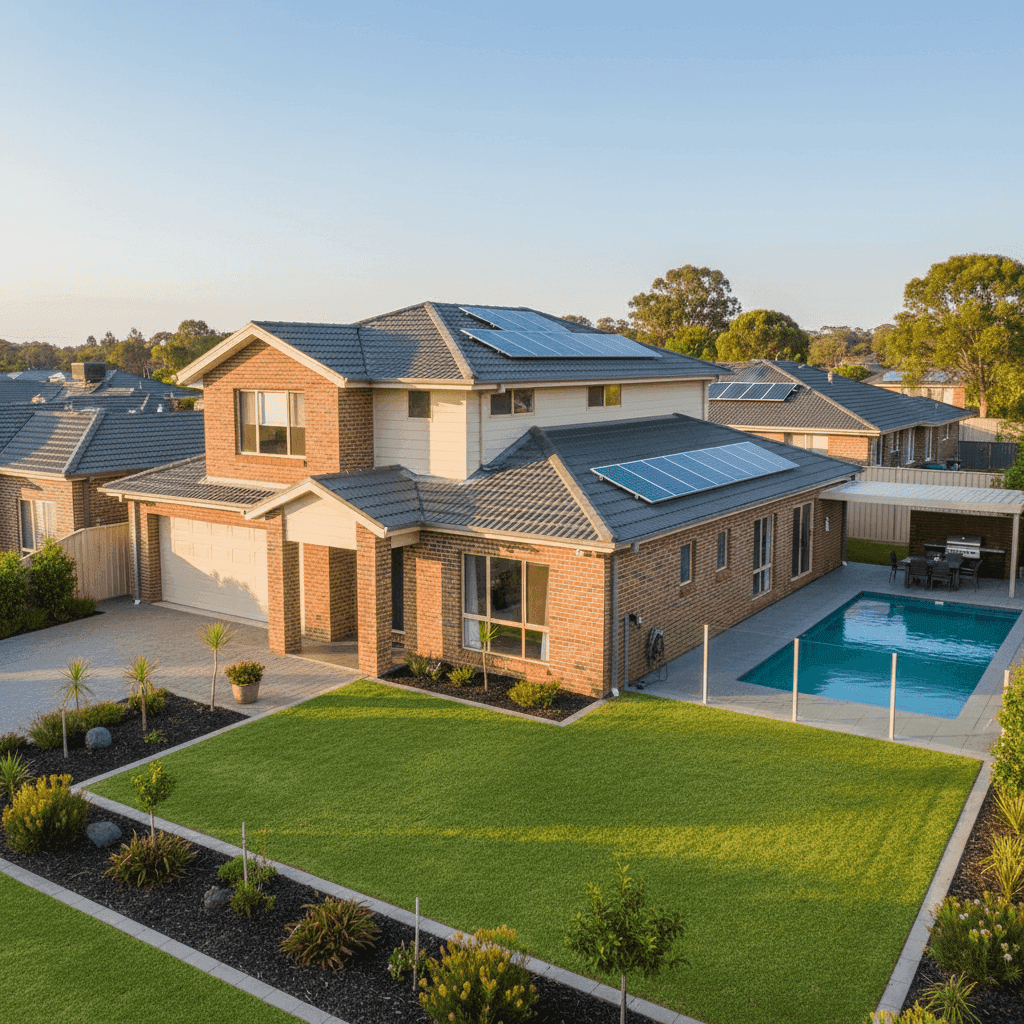

The quote in question comes in at $4,705 per year (or around $454 per month) for combined home and contents cover, with a building sum insured of $1,315,000 and contents valued at $151,000. Both the building and contents excess are set at a standard $500.

Our price rating for this quote is CHEAP — below average — which is genuinely good news for the homeowner. To put that into perspective:

- The NSW state average premium sits at $9,528/year, making this quote less than half the state average.

- The NSW state median is $3,770/year — this quote is modestly above the median, which is expected given the size and value of the property.

- The national average is $5,347/year, meaning this quote also comes in below what most Australians pay across the country.

Given that this is a large, six-bedroom home with a high building sum insured of over $1.3 million, a premium under $5,000 represents strong value. Larger homes typically attract higher premiums due to greater rebuild costs, so seeing a below-average rating here is a meaningful result. You can explore broader NSW home insurance statistics and national home insurance data to see how premiums vary across Australia.

---

How Thornton Compares

Understanding where your suburb sits in the broader pricing landscape is key to evaluating any quote. Here's how Thornton stacks up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $4,705 |

| Cessnock LGA Average | $2,462 |

| NSW State Median | $3,770 |

| NSW State Average | $9,528 |

| National Average | $5,347 |

| National Median | $2,764 |

It's worth noting that the Cessnock LGA average of $2,462/year is notably lower than this quote — but that figure reflects the broader LGA population, which includes many smaller and lower-value properties. A six-bedroom home with a $1.3 million sum insured and extras like a pool and solar panels will naturally sit above the LGA average. When you adjust for property size and features, this quote holds up very well.

For suburb-specific data, you can check out the Thornton NSW 2322 insurance statistics page for more localised context as more data becomes available.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence the cost of cover. Understanding these can help you have more informed conversations with insurers.

Brick Veneer Walls & Tiled Roof

Brick veneer construction with a tiled roof is one of the most common — and insurer-friendly — combinations in Australia. Both materials are considered durable and fire-resistant, which typically translates to more competitive premiums compared to homes with timber cladding or older iron roofing.

Slab Foundation

A concrete slab foundation is standard for homes built in this era and is generally viewed favourably by underwriters. It reduces the risk of subsidence and pest-related structural damage that can affect older homes on stumps or piers.

Size: 345 sqm

At 345 square metres, this is a substantial home. Building size is one of the most significant drivers of rebuild cost, and a $1,315,000 sum insured reflects that. Getting the sum insured right is critical — underinsurance is a common and costly mistake for owners of larger homes.

Pool, Solar Panels & Ducted Climate Control

These three features add value to the property but also add complexity to the insurance equation. A swimming pool introduces liability considerations and can increase contents or liability cover requirements. Solar panels are a significant asset — typically covered under building insurance — and their replacement cost should be factored into the sum insured. Ducted climate control is a fixed installation and similarly forms part of the building cover.

Timber & Laminate Flooring

Flooring type matters more for contents and internal damage claims. Timber and laminate floors can be costly to repair or replace after water damage, so it's worth confirming your policy covers floor coverings adequately.

No Cyclone Risk

Thornton falls outside designated cyclone risk zones, which removes one of the more significant premium loading factors that affects homeowners in northern Queensland and parts of WA. This contributes to the relatively competitive pricing seen here.

---

Tips for Homeowners in Thornton

1. Review your sum insured annually With construction costs continuing to rise across NSW, the cost to rebuild a 345 sqm home can change significantly year to year. Make sure your $1,315,000 building sum insured keeps pace with current building rates in the Hunter region — your insurer may offer an automatic indexation feature, but it's worth checking.

2. Confirm solar panels are covered under building Solar panel systems can cost tens of thousands of dollars to replace. Verify with your insurer that your panels are explicitly included in your building cover and that the replacement value is reflected in your sum insured.

3. Check pool liability cover A swimming pool increases the importance of having adequate liability cover within your home insurance policy. Ensure your policy includes public liability protection of at least $10–$20 million, which is standard in most comprehensive policies.

4. Consider a higher excess to reduce premiums Your current excess is $500 for both building and contents — a fairly standard level. If you have a financial buffer and rarely make small claims, increasing your excess to $1,000 or more could meaningfully reduce your annual premium, freeing up cash for other priorities.

---

Compare and Save with CoverClub

Whether you're renewing your current policy or shopping around for the first time, comparing quotes is one of the easiest ways to ensure you're not overpaying. This quote shows that below-average pricing is achievable for a large home in Thornton — but the market is always moving. Head to CoverClub to compare home and contents quotes for your property and see what's available to you today.