Tinana is a quiet residential suburb in Queensland's Fraser Coast region, sitting just south of Maryborough. It's the kind of neighbourhood where free standing family homes dominate the streetscape — and for good reason. With solid block sizes, established infrastructure, and a relaxed lifestyle, it's a popular choice for families putting down roots. But when it comes to protecting one of your biggest assets, understanding what you should be paying for home and contents insurance is just as important as finding the right property in the first place.

This article breaks down a real insurance quote for a 4-bedroom, 2-bathroom free standing home in Tinana (postcode 4650) and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

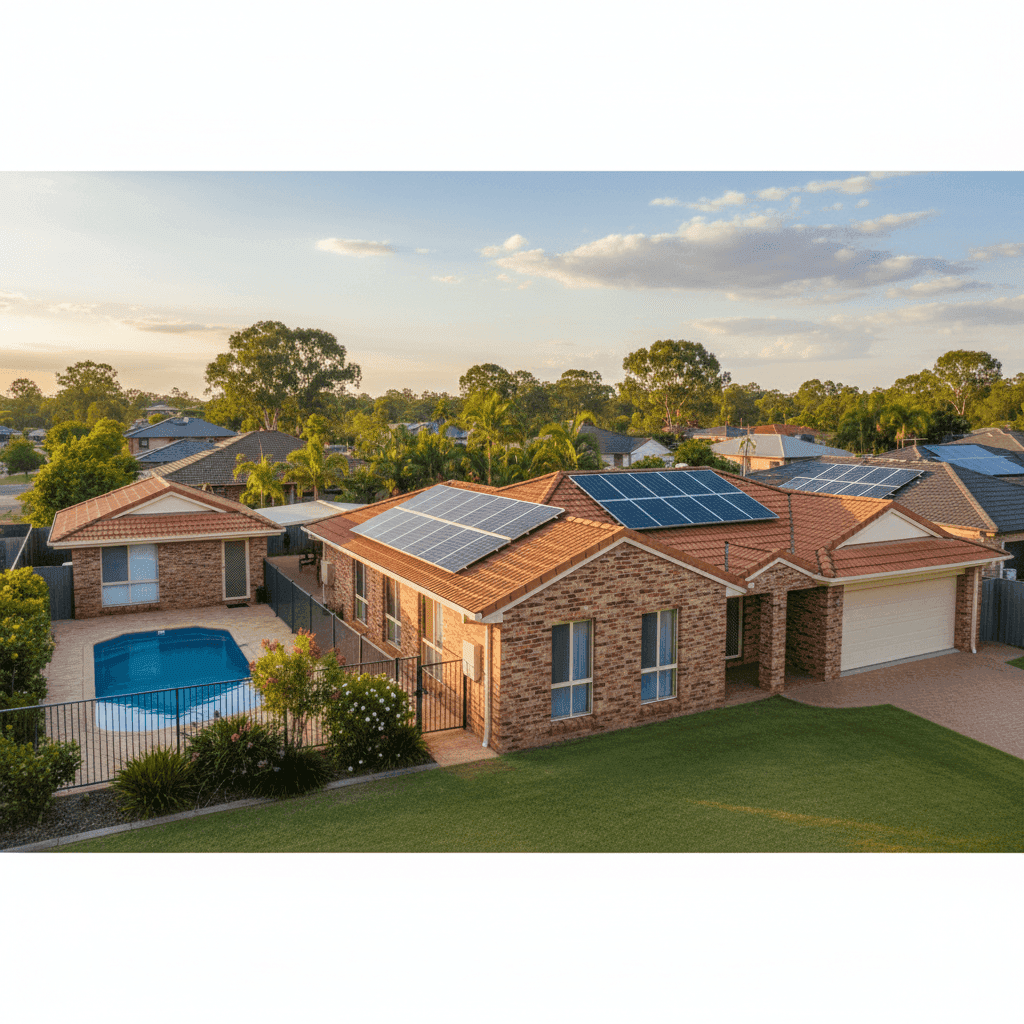

The quote in question comes in at $3,149 per year (or roughly $302 per month) for combined home and contents cover, with a building sum insured of $840,000 and contents valued at $80,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up well under scrutiny. The suburb median for Tinana sits at $3,215 per year, meaning this quote lands just below the midpoint of what most comparable properties in the area are paying. It's not a bargain-basement price, but it's also not cause for concern. For a well-specified property of this size — with features like a pool, solar panels, ducted climate control, and a granny flat — sitting near the median is a reasonable outcome.

It's worth noting that insurance pricing isn't purely about the property itself. Insurers weigh up a complex mix of factors including local claims history, proximity to flood zones or fire-prone areas, and the cost to rebuild in your region. A quote that lands near the suburb median suggests the insurer has priced this risk without loading the premium excessively.

---

How Tinana Compares

To put this quote in proper perspective, here's how Tinana stacks up against broader benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $3,149/yr |

| Tinana Suburb Median | $3,215/yr |

| Tinana Suburb Average | $4,082/yr |

| Tinana 25th Percentile | $2,471/yr |

| Tinana 75th Percentile | $5,838/yr |

| Gympie LGA Average | $5,581/yr |

| QLD State Median | $3,903/yr |

| QLD State Average | $9,129/yr |

| National Median | $2,764/yr |

| National Average | $5,347/yr |

A few things stand out here. First, the gap between Queensland's average ($9,129) and its median ($3,903) is enormous — a clear sign that the state's premium distribution is heavily skewed by high-risk coastal and cyclone-prone areas pushing the average upward. Tinana, which is not classified as a cyclone risk area, benefits from sitting outside those high-premium zones.

Second, this quote is notably below the Gympie LGA average of $5,581, which suggests that Tinana — as a suburb within the broader Gympie local government area — carries a more favourable risk profile than some surrounding localities.

Compared to the national median of $2,764, this quote is moderately higher, which reflects Queensland's generally elevated insurance environment relative to southern states. You can explore more detail on Tinana suburb insurance stats, Queensland-wide trends, or national insurance benchmarks to dig deeper into the data.

---

Property Features That Affect Your Premium

This particular property has a number of characteristics that insurers pay close attention to when calculating risk and replacement cost.

Double Brick Construction Double brick external walls are generally viewed favourably by insurers. They offer strong resistance to fire, wind, and structural damage, which can translate to lower risk assessments compared to timber-framed or clad homes. This is a meaningful advantage in Queensland's variable climate.

Tiled Roof on a Slab Foundation Concrete tile roofs are durable and perform well in heavy rain and hail events — both of which are relevant in South East Queensland. A slab foundation is similarly robust and reduces the risk of subsidence or pest-related structural issues that can affect stumped or raised homes.

Swimming Pool A pool adds to the replacement cost of the property and may also factor into liability considerations. Homeowners with pools should ensure their policy includes adequate liability cover in addition to building and contents protection.

Solar Panels Solar systems are typically covered under building insurance, but it's worth confirming with your insurer that the panels and associated inverter equipment are explicitly included in your sum insured. Given the cost of modern solar installations, this can represent a meaningful portion of your building value.

Granny Flat A secondary dwelling on the property adds both value and complexity to your cover. Insurers treat granny flats differently — some include them automatically under the main building policy, while others require a separate endorsement. Make sure your policy documentation is clear on this point.

Ducted Climate Control Ducted air conditioning systems are fixed to the structure and generally covered under building insurance. However, mechanical breakdown is typically excluded from standard policies, so a separate appliance or home warranty product may be worth considering.

Building Size: 244 sqm At 244 square metres, this is a substantial home. The $840,000 sum insured equates to roughly $3,443 per square metre — broadly in line with current Queensland rebuild cost estimates for a well-finished double brick home, though homeowners should periodically review this figure as construction costs continue to rise.

---

Tips for Homeowners in Tinana

1. Review Your Sum Insured Annually Construction costs in Queensland have increased significantly over recent years due to labour shortages and material price inflation. A sum insured that was adequate two or three years ago may no longer cover a full rebuild today. Use a building cost calculator or speak with a quantity surveyor to sense-check your figure each year.

2. Confirm Granny Flat Coverage Explicitly Don't assume your granny flat is automatically covered under your main policy. Ask your insurer directly whether the secondary dwelling is included, and if so, whether there are any conditions — such as restrictions on renting it out — that could affect your cover.

3. Check Flood and Storm Definitions Carefully While Tinana is not in a cyclone risk zone, the Fraser Coast region is no stranger to heavy rainfall and localised flooding. Home insurance policies in Australia distinguish between "flood" (rising water from a river or lake) and "storm surge" or "stormwater," and not all policies cover both. Read the Product Disclosure Statement carefully and consider adding flood cover if it's not included by default.

4. Compare Quotes at Renewal Time The home insurance market is competitive, and premiums can vary significantly between providers for identical cover. Even if you're happy with your current insurer, it's worth running a comparison at renewal to make sure you're not paying a loyalty premium. Get a quote at CoverClub to see how your current premium stacks up.

---

Ready to Compare?

Whether you're a first-time buyer in Tinana or a long-term homeowner reviewing your cover, comparing quotes is one of the simplest ways to make sure you're getting value for money. At CoverClub, you can enter your address and get a quote in minutes — then benchmark it against real data from your suburb, your state, and across Australia. Smart cover starts with knowing your numbers.