If you own a free standing home in Tinana, QLD 4650, you've probably noticed that home insurance premiums can vary enormously — even between neighbouring streets. This article breaks down a real home and contents insurance quote for a 2-bedroom, 1-bathroom free standing home in Tinana, comparing it against suburb, state, and national benchmarks to help you understand whether you're getting a fair deal.

---

Is This Quote Fair?

The annual premium for this property came in at $3,505 per year (or $329/month), covering both building and contents with a building sum insured of $874,000 and contents valued at $98,000. Both the building and contents excess are set at $1,000.

Our pricing engine rates this quote as FAIR — Around Average, which is a reasonable outcome for a property of this type and age in the Tinana area. It sits comfortably within the middle range of what local homeowners are paying, neither among the cheapest nor the most expensive quotes we see for this suburb.

For context, the suburb average premium is $4,082/year, meaning this quote comes in roughly $577 below the local average — a meaningful saving. The suburb median sits at $3,215/year, placing this quote slightly above the midpoint of what Tinana homeowners typically pay. Based on a sample of 50 quotes in the area, the spread is wide: the 25th percentile sits at $2,471/year while the 75th percentile reaches $5,838/year. This wide range reflects the diversity of properties, sum insured values, and insurer pricing models across the suburb.

---

How Tinana Compares

To put this quote in broader perspective, it's worth zooming out to the state and national picture.

| Benchmark | Average | Median |

|---|---|---|

| Tinana (4650) | $4,082/yr | $3,215/yr |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

| LGA (Gympie) | $5,581/yr | — |

A few things stand out here. Queensland's state average of $9,129/year is dramatically higher than the median of $3,903/year — a clear sign that a relatively small number of very high-risk or high-value properties are pulling the average upward. North Queensland cyclone-prone areas, in particular, are known to push premiums into the tens of thousands annually.

Tinana sits within the Gympie LGA, where the average premium is $5,581/year. This quote at $3,505/year is well below that LGA average, which is encouraging. Compared to the national average of $5,347/year, this quote also looks competitive, coming in around 34% below that figure.

One important note: Tinana is not classified as a cyclone risk area, which is a significant factor in keeping premiums more manageable compared to coastal Far North Queensland. This is a notable advantage for homeowners in this part of the Wide Bay region.

---

Property Features That Affect Your Premium

The characteristics of this particular home play a meaningful role in how insurers price the risk. Here's how each feature stacks up:

- Construction year (1985): A home built in the mid-1980s is old enough to carry some age-related risk (ageing plumbing, wiring, and roofing materials), but not so old as to attract the highest loadings reserved for pre-1960s homes. Insurers will factor in the potential cost of bringing repairs up to current building codes.

- Concrete external walls: Concrete construction is generally viewed favourably by insurers. It offers strong resistance to fire, wind, and impact damage compared to timber-framed homes, and can contribute to a lower premium.

- Steel/Colorbond roof: Colorbond roofing is widely regarded as one of the more durable and insurer-friendly roofing materials in Australia. It performs well in high winds, resists corrosion, and is relatively inexpensive to repair or replace — all factors that can help moderate your premium.

- Slab foundation: A concrete slab foundation is standard for Queensland homes of this era and is generally considered low-risk from an insurance perspective, with no subfloor space that could be subject to flooding or pest damage.

- Timber/Laminate flooring: While attractive and common, timber and laminate floors can be susceptible to water damage. Insurers may factor this in when assessing contents and building claims.

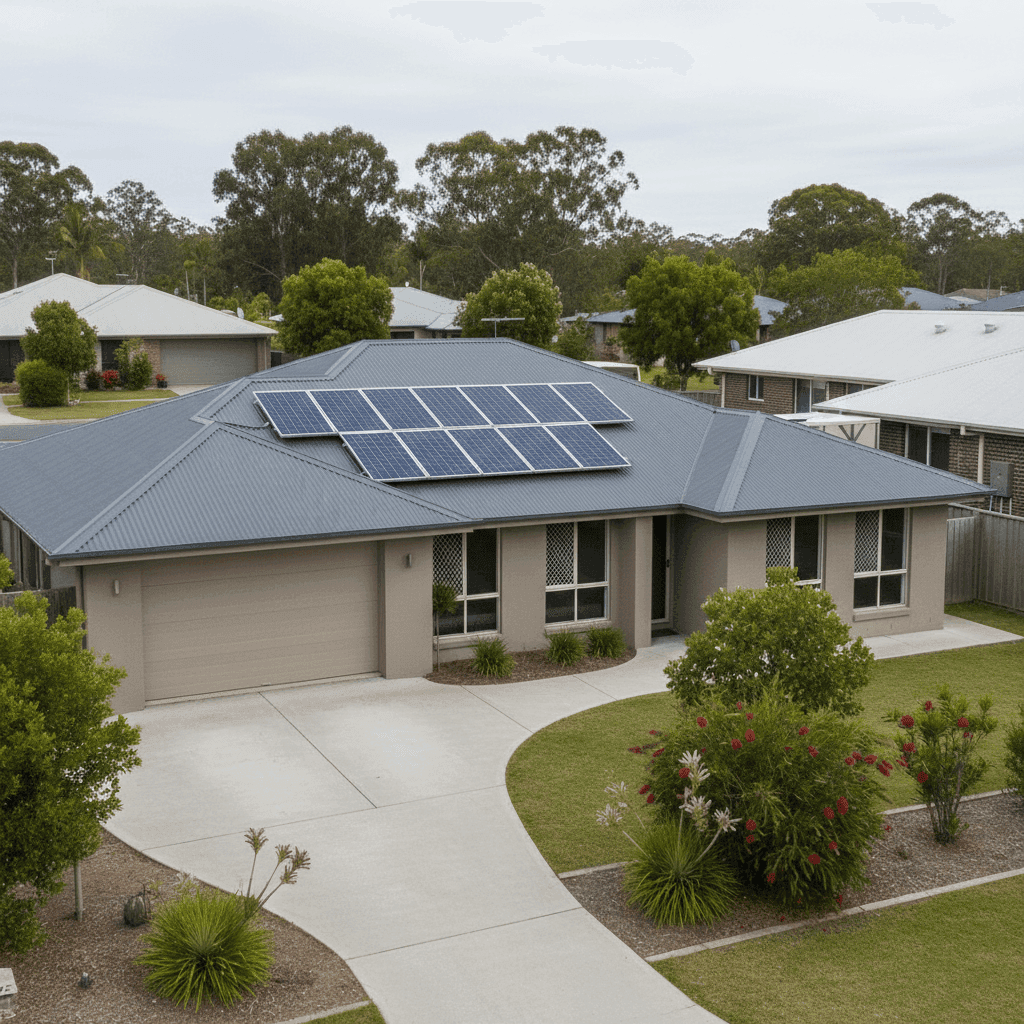

- Solar panels: The presence of solar panels adds modest value to the property and is increasingly common in Queensland. It's worth confirming with your insurer that your solar system is explicitly covered under your building policy, as some policies treat it as a separate item.

- Standard fittings: Standard-quality fittings mean rebuild costs are more predictable and typically lower than homes with premium or bespoke finishes, which can help keep the sum insured — and therefore the premium — in check.

- Building size (105 sqm): At 105 square metres, this is a modestly sized home. A smaller footprint generally means a lower rebuild cost, which is reflected in the sum insured and ultimately the premium.

---

Tips for Homeowners in Tinana

Whether you're reviewing your existing policy or shopping around for the first time, here are four practical steps to help you get the best value on home insurance in Tinana.

- Review your sum insured regularly. Building costs in Queensland have risen significantly in recent years due to labour shortages and material price increases. Make sure your $874,000 sum insured still reflects what it would actually cost to rebuild your home from scratch — not just its market value. Underinsurance is one of the most common and costly mistakes homeowners make.

- Confirm your solar panels are covered. Solar panel systems are a meaningful investment and can be damaged by storms, hail, or electrical faults. Check your policy wording carefully to ensure they're included under your building cover, and note the coverage limits.

- Compare quotes annually. Insurers reprice their books regularly, and loyalty doesn't always pay. Even if your current premium seems reasonable, running a comparison at renewal time takes only a few minutes and could reveal a better deal. Get a quote at CoverClub to see what's available in your area.

- Check your excess settings. Both the building and contents excess on this policy are set at $1,000. Opting for a higher excess can reduce your annual premium, but make sure it's an amount you could comfortably pay out of pocket in the event of a claim. It's a balance worth revisiting as your financial situation changes.

---

Compare Your Home Insurance Today

Whether this quote reflects your own situation or you're simply curious about what homeowners in Tinana are paying, CoverClub makes it easy to see where you stand. Our platform aggregates real quote data so you can compare premiums with confidence. Start a quote at CoverClub and find out if you're getting the best deal on your home and contents insurance — it only takes a few minutes.