Torbanlea is a quiet rural locality in Queensland's Fraser Coast region, and like much of regional Queensland, home insurance here deserves careful attention. This article breaks down a real home and contents insurance quote for a four-bedroom, free-standing home in Torbanlea (postcode 4662) — examining whether the price is competitive, how it stacks up against local and national benchmarks, and what property features are likely driving the premium.

---

Is This Quote Fair?

The annual premium for this property came in at $1,891 per year (or roughly $190 per month), covering both building (insured at $680,000) and contents ($55,000). Our price rating for this quote is FAIR — Around Average.

That rating holds up well under scrutiny. Based on 34 quotes collected for Torbanlea, the suburb average sits at $1,936/yr and the median at $1,976/yr — meaning this quote comes in below both the local average and median. That's a solid result, particularly for a property of this size and age.

It's worth noting the wide spread of premiums in the suburb: the 25th percentile is just $992/yr, while the 75th percentile jumps to $2,685/yr. This kind of variability is common in regional Queensland, where insurers assess risk quite differently depending on property characteristics, construction materials, and proximity to flood or fire-prone areas. At $1,891, this quote sits comfortably in the middle of that range — not the cheapest available, but well clear of the more expensive end.

The building excess of $4,000 and contents excess of $1,000 are on the higher side, which likely helps keep the annual premium down. It's a trade-off worth understanding: a higher excess means lower ongoing costs, but more out-of-pocket expense if you do need to make a claim.

---

How Torbanlea Compares

To put this quote in broader context, here's how Torbanlea stacks up against Queensland and national benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Torbanlea (4662) | $1,936/yr | $1,976/yr |

| Fraser Coast LGA | $4,810/yr | — |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

These figures are striking. Torbanlea's average premium is less than half the Fraser Coast LGA average ($4,810/yr) and less than half the Queensland state average ($4,547/yr). Even compared to the national average of $2,965/yr, Torbanlea comes out significantly cheaper.

This likely reflects a combination of factors: Torbanlea is not classified as a cyclone risk area, which removes one of the biggest premium drivers in Queensland. The suburb also sits away from the coastal flood zones that push premiums sky-high in many other parts of the Fraser Coast. For homeowners in Torbanlea, this is genuinely good news — you're in one of the more affordable pockets of an otherwise expensive state for home insurance.

The quote analysed here, at $1,891/yr, beats the suburb average by around $45 and the national median by over $800. That's a meaningful saving, particularly over a five- or ten-year period.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth understanding in the context of insurance pricing:

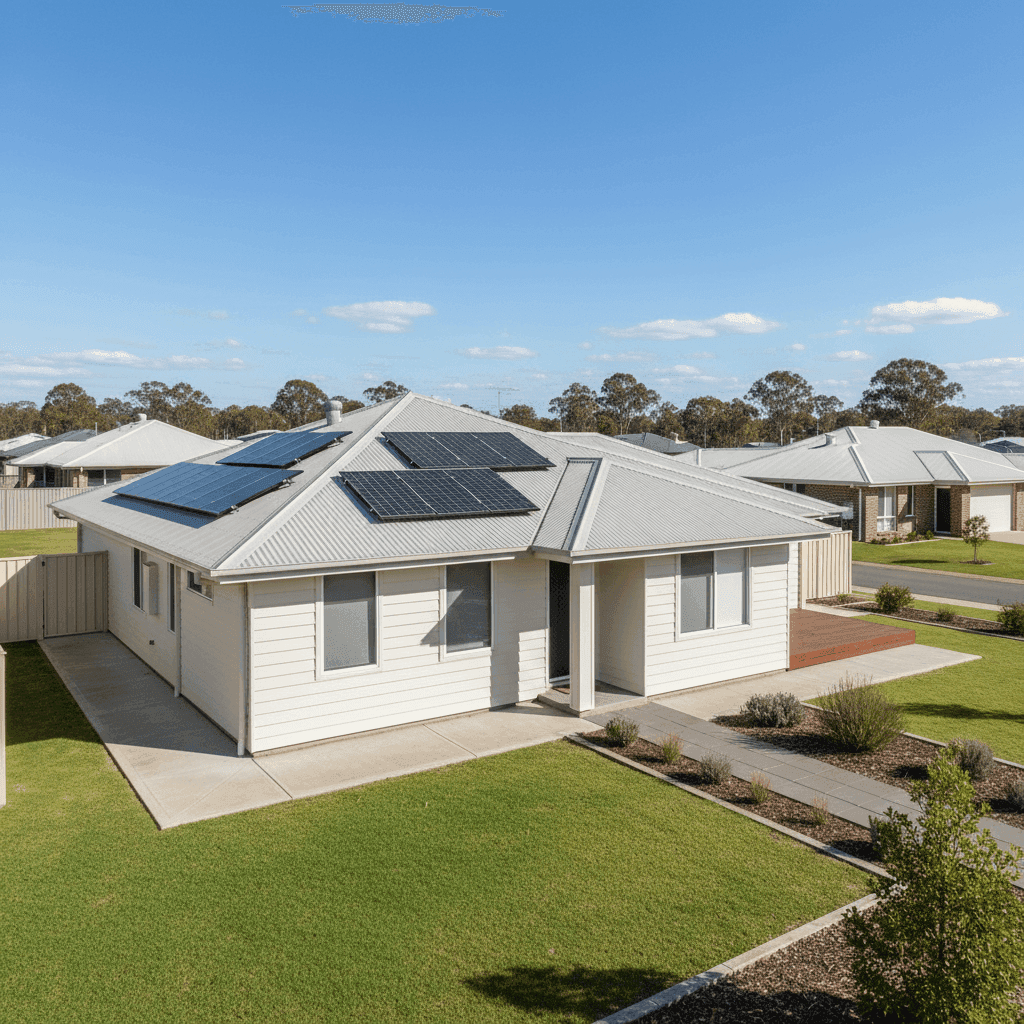

Hardiplank/Hardiflex external walls are a fibre cement product that insurers generally view favourably. It's durable, resistant to rot and termites, and performs reasonably well in fire conditions compared to timber weatherboard. This is a positive factor for premium pricing.

Steel/Colorbond roofing is another tick in the right column. Colorbond is one of the most widely accepted roofing materials by Australian insurers — it's lightweight, fire-resistant, and long-lasting. It also handles hail better than some alternatives, which matters in Queensland's storm season.

Slab foundation is standard and uncontroversial from an insurance perspective. It's stable and doesn't carry the underfloor risks associated with high-set or timber-stumped homes.

Construction year: 1980 — at over 40 years old, this home is ageing, and insurers do factor building age into their calculations. Older homes can carry higher risk of plumbing failures, electrical issues, or structural wear. However, the use of durable materials like Colorbond roofing and Hardiflex cladding may offset some of this concern.

Solar panels are present on this property. While solar systems add value and are typically covered under building insurance, they can also add modest complexity to a claim (e.g., damage during storms). It's worth confirming with your insurer that your solar system is explicitly included in your building sum insured.

No pool, no ducted climate control — both of these simplify the risk profile and keep the premium lower than it might otherwise be.

214 sqm building size is a reasonable footprint for a four-bedroom home. The building sum insured of $680,000 translates to roughly $3,177 per sqm — a figure that's worth reviewing periodically to ensure it reflects current construction costs in your area.

---

Tips for Homeowners in Torbanlea

1. Review your building sum insured regularly Construction costs have risen significantly across Australia in recent years. A sum insured set several years ago may no longer be sufficient to fully rebuild your home. Use a building cost calculator or speak with a local builder to sense-check your coverage amount.

2. Confirm your solar panels are covered Solar panel systems can be worth tens of thousands of dollars. Make sure your policy explicitly covers them under the building section, and check whether storm damage, inverter failure, or accidental breakage are included.

3. Shop around — even when your quote looks fair A "fair" rating means you're around the average, not necessarily at the best available price. Given the wide premium range in Torbanlea (from $992 to $2,685+), there may be room to find a more competitive quote without sacrificing cover quality. Compare quotes at CoverClub to see what's available for your specific property.

4. Understand your excess before you commit This quote carries a $4,000 building excess — which is relatively high. If your finances would make a $4,000 out-of-pocket payment difficult in the event of a claim, it may be worth requesting a quote with a lower excess, even if the annual premium increases slightly.

---

Ready to Compare?

Whether you're renewing your existing policy or shopping for the first time, it pays to compare. CoverClub makes it easy to get multiple home insurance quotes tailored to your property in Torbanlea. Start your free quote today and see how your premium stacks up against the suburb, state, and national benchmarks — all in one place.