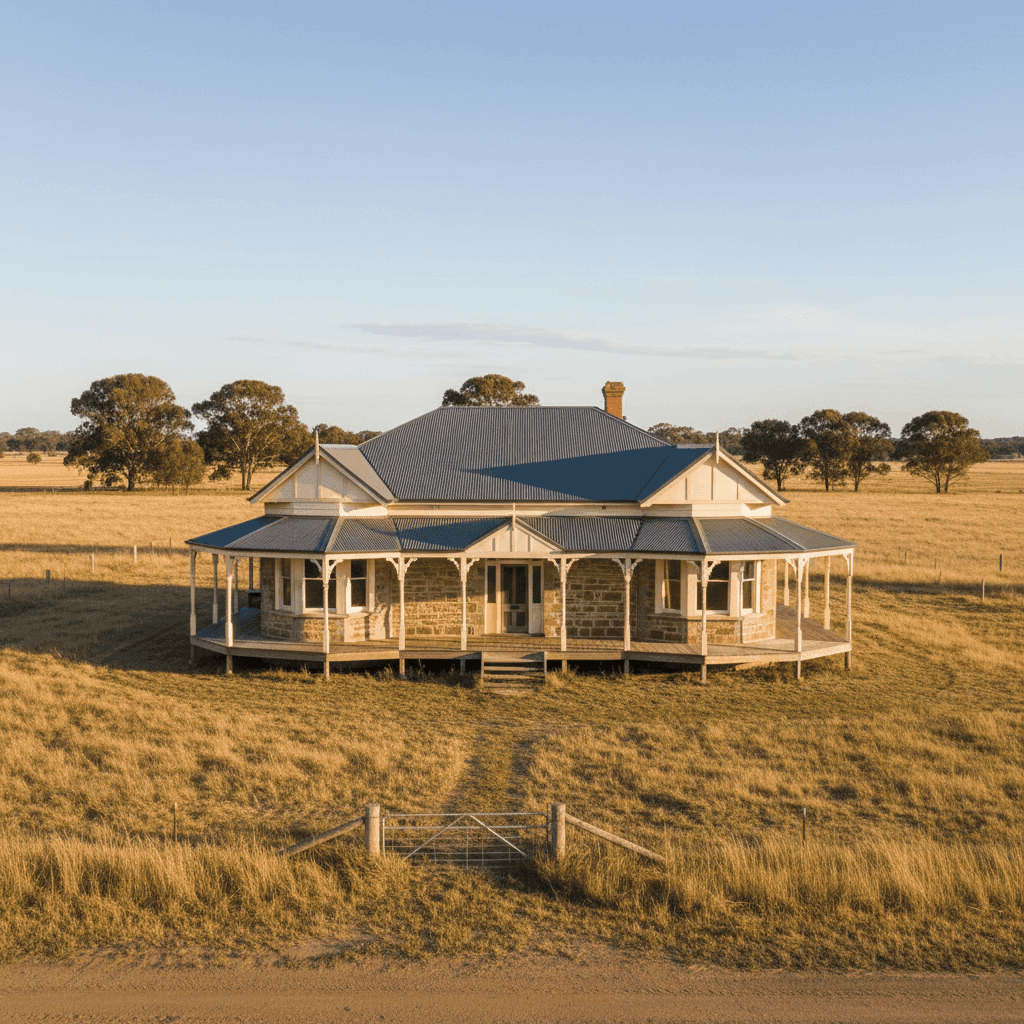

Tragowel is a quiet rural locality in Victoria's Murray River country, sitting within the Shire of Swan Hill. It's the kind of place where large, character-filled homes on generous blocks are the norm — and this five-bedroom free-standing home, built back in 1904, is a fine example. With a building sum insured of $933,000 and an annual premium of $3,436, this quote gives us a great opportunity to dig into what drives home insurance costs in regional Victoria and how this property stacks up against the broader market.

---

Is This Quote Fair?

The short answer: yes, broadly speaking. This quote has been rated FAIR (Around Average), which means it's sitting in a reasonable range relative to comparable properties — not a bargain, but not an outlier either.

At $3,436 per year (or $336 per month), this premium is notably higher than the VIC state average of $3,000/yr and the state median of $2,718/yr. However, it sits well below the national average of $5,347/yr, which is heavily influenced by high-risk coastal and cyclone-prone areas in Queensland and Western Australia.

The "FAIR" rating reflects that while the premium is above the Victorian average, it's not unreasonable given the property's age, size, construction characteristics, and the relatively high sum insured of $933,000. Older homes — particularly those built in the early 1900s — often attract higher premiums due to the increased cost of like-for-like restoration using period-appropriate materials and methods.

---

How Tragowel Compares

Putting this quote in context across different benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,436 |

| LGA (Swan Hill) Average | $2,484 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

The most telling comparison here is against the Swan Hill LGA average of $2,484/yr — this quote comes in about $952 above that local benchmark. That gap is worth understanding rather than simply accepting. Much of it is likely attributable to the property's age, its stump foundation, and the higher-than-average sum insured relative to typical homes in the area.

Suburb-level data for Tragowel specifically isn't available at this stage, but you can keep an eye on the Tragowel suburb stats page as more data comes through. For broader Victorian context, the VIC insurance stats page is a useful reference point.

Compared to the national picture, this premium looks quite reasonable — homeowners in parts of Far North Queensland or cyclone-exposed coastal WA can pay two to three times this amount.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium quoted. Here's how each one plays into the equation:

Age of construction (1904) A home over 120 years old carries inherent complexity when it comes to insurance. Reinstatement costs are higher because older homes often require specialised trades, heritage-compatible materials, and more labour-intensive repair work. Insurers price this risk accordingly.

Stump foundation Homes on stumps — common in rural Victoria and across older Australian housing stock — can be more susceptible to movement, subsidence, and pest damage over time. This adds a layer of risk that can nudge premiums upward compared to slab-on-ground construction.

Timber and laminate flooring While aesthetically appealing and typical of period homes, timber flooring can be costly to repair or replace following water damage or fire. It also contributes to the overall reinstatement value of the building.

Steel/Colorbond roof This is actually a positive from an insurance standpoint. Colorbond roofing is durable, fire-resistant, and relatively straightforward to replace. It's one of the more insurer-friendly roof types and likely helps moderate the premium.

Building size (277 sqm) and sum insured ($933,000) At 277 square metres with five bedrooms and two bathrooms, this is a substantial home. The $933,000 sum insured reflects the true cost of rebuilding — particularly given the age and construction style — and is the single biggest driver of the premium amount.

Ducted climate control The presence of ducted climate control adds to the overall replacement value of the home's fixed fittings, contributing modestly to the sum insured and premium.

No pool, no solar panels The absence of a pool and solar panels removes two common sources of additional risk and cost. This keeps the policy scope focused squarely on the core building.

---

Tips for Homeowners in Tragowel

1. Review your sum insured regularly Construction costs in regional Victoria have risen significantly in recent years. Make sure your $933,000 sum insured still reflects the true cost of rebuilding your home — not just its market value. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Get multiple quotes before renewing A "FAIR" rating means this quote is around average — but average isn't necessarily the best you can do. Insurers use different pricing models, and a premium that's competitive with one insurer may be significantly cheaper with another. Compare quotes at CoverClub to see what else is available for your property.

3. Ask about discounts for home security and maintenance Some insurers offer premium reductions for homes with monitored security systems, smoke alarms, or deadbolt locks. Keeping an older home well-maintained — particularly stumps, roofing, and plumbing — can also support your claim outcomes and potentially your renewal pricing.

4. Consider whether building-only cover is sufficient This policy covers the building only, not contents. If you have valuable furniture, appliances, or personal belongings, a separate contents policy (or a combined building and contents policy) is worth exploring. For a five-bedroom home, the contents value can add up quickly.

---

Compare Your Options with CoverClub

Whether you're renewing an existing policy or shopping for the first time, it pays to compare. CoverClub makes it easy to see how your quote stacks up and find competitive options tailored to your property. Get a quote today and make sure your Tragowel home is properly protected — without paying more than you need to.