Trinity Beach is one of Cairns' most sought-after coastal suburbs — a relaxed beachside community that attracts families, retirees, and sea-changers alike. But living close to the Coral Sea in Far North Queensland comes with a real-world cost that many homeowners only discover when they receive their annual insurance renewal: premiums that can be significantly higher than the national norm.

This article takes a close look at a recent building insurance quote for a three-bedroom, two-bathroom free-standing home in Trinity Beach (postcode 4879) — breaking down whether the price is fair, how it stacks up against local and national benchmarks, and what you can do to manage costs without sacrificing cover.

---

Is This Quote Fair?

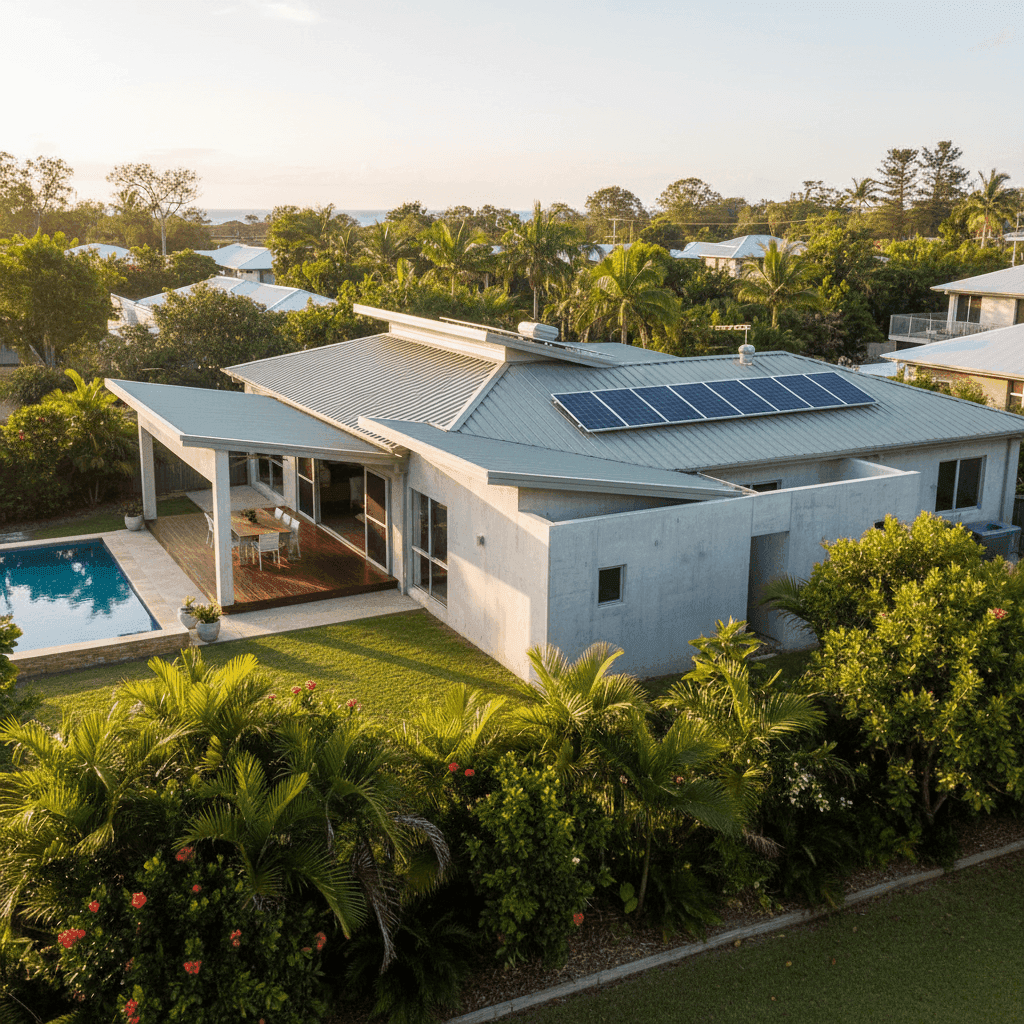

The quote in question sits at $6,489 per year (or $622/month) for building-only cover on a 139 sqm concrete home, insured for $788,000 with a $1,000 excess.

Our price rating for this quote is EXPENSIVE — Above Average.

Compared to the Trinity Beach suburb average of $5,148/yr, this quote comes in roughly 26% above what other homeowners in the area are typically paying. It also sits above the suburb's 75th percentile of $5,520/yr — meaning it's pricier than at least three-quarters of comparable quotes we've seen in this postcode.

That said, "expensive" is relative. The quote is meaningfully higher than the local median, but it isn't wildly out of step with what's possible in a high-risk coastal zone. There's a reasonable chance a different insurer could price this risk more competitively — and that's exactly why comparing quotes matters.

---

How Trinity Beach Compares

To put this quote in proper context, here's how Trinity Beach stacks up across different geographic levels:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Trinity Beach (4879) | $5,148/yr | $4,612/yr |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

| Cairns LGA | $12,404/yr | — |

A few things stand out here. First, the Queensland state average of $9,129/yr is dramatically higher than the state median of $3,903/yr — a sign that a relatively small number of very expensive properties (particularly in cyclone-prone coastal areas) are pulling the average up significantly. Trinity Beach sits in that higher-risk cohort.

Second, the Cairns LGA average of $12,404/yr is striking. It suggests that while this particular quote feels expensive relative to the Trinity Beach suburb sample, it's actually well below what some homeowners in the broader Cairns region are paying. Location within the LGA, property age, construction type, and insurer appetite all contribute to that wide spread.

At a national level, the median of $2,764/yr illustrates just how much of a premium Far North Queensland homeowners pay compared to the rest of the country. This isn't a quirk of one insurer — it reflects the genuine risk profile of the region.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on its insurance cost. Understanding these helps explain why the quote lands where it does.

Cyclone risk area: This is the single biggest factor. Trinity Beach falls within a designated cyclone risk zone, and insurers price accordingly. Cyclone cover typically adds a substantial loading to premiums across all of Far North Queensland — there's no avoiding it, but some insurers manage this risk more efficiently than others.

Construction year (1985): Homes built in the mid-1980s predate modern cyclone-resistant building codes that were progressively strengthened after Cyclone Tracy and further refined in subsequent decades. Older builds can attract a higher risk assessment from underwriters, particularly if the construction hasn't been upgraded.

Concrete external walls: This is a positive factor. Concrete construction is generally viewed more favourably than timber weatherboard in cyclone-prone areas, as it offers greater structural resilience. It may be helping to keep this quote lower than it might otherwise be for a comparable timber home.

Steel/Colorbond roof: Another tick in the right column. Colorbond roofing is durable and performs well in high-wind events compared to older materials like terracotta tiles or fibrous cement sheeting.

Slab foundation and tiled flooring: These features signal a robust, low-maintenance build that's less susceptible to moisture and termite damage — both relevant risk factors in tropical Queensland.

Swimming pool: Pools add a small but real liability component to building policies, and may also factor into the overall sum insured calculation.

Solar panels: Panels are increasingly common in QLD and most insurers now include them under building cover, but they do add to the replacement cost — which is likely reflected in the $788,000 sum insured.

Ducted climate control: Similarly, ducted systems are a significant fixed asset that contributes to rebuilding costs and is factored into the insured value.

---

Tips for Homeowners in Trinity Beach

1. Compare quotes — every year The gap between the cheapest and most expensive insurer for the same property in a cyclone zone can be thousands of dollars annually. Insurers regularly reprice their appetite for specific postcodes, so a policy that was competitive last year may not be this year. Use CoverClub to compare quotes at renewal time rather than simply auto-renewing.

2. Review your sum insured carefully At $788,000 for a 139 sqm home, the sum insured works out to roughly $5,670/sqm — which is on the higher end but not unreasonable given the tropical build requirements, pool, solar, and ducted systems. However, it's worth using a building cost calculator to verify this figure. Being over-insured means you're paying a premium on value you'd never recover; being under-insured can leave you seriously exposed after a major event.

3. Ask about cyclone mitigation discounts Some insurers offer premium reductions for homes that have been assessed or upgraded to improve cyclone resilience — things like roof tie-downs, shutters, or a formal cyclone rating. If your home has had any of these upgrades, make sure your insurer knows.

4. Consider your excess strategically This quote carries a $1,000 excess. In many cases, opting for a higher excess (say, $2,500 or $5,000) can meaningfully reduce the annual premium. If you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim, this trade-off can be worth exploring — particularly for a property where you're unlikely to make small claims.

---

Compare Your Home Insurance Today

Whether you're a long-term Trinity Beach local or new to the area, it pays to know what the market looks like before you commit to a policy. CoverClub aggregates real quote data from across Australia so you can see exactly where your premium sits relative to your neighbours.

Get a home insurance quote for your Trinity Beach property and find out if you're getting a fair deal — or paying more than you need to.