Trinity Park is a leafy coastal suburb on the northern fringe of Cairns, popular with families drawn to its relaxed lifestyle, proximity to the Great Barrier Reef, and easy access to the Cairns CBD. It's also a suburb where home insurance costs can vary dramatically — largely because of its location in a declared cyclone risk zone. This article breaks down a recent building insurance quote for a five-bedroom free-standing home in Trinity Park (postcode 4879), examines how it compares to local and national benchmarks, and offers practical tips for homeowners looking to get the best value on their cover.

---

Is This Quote Fair?

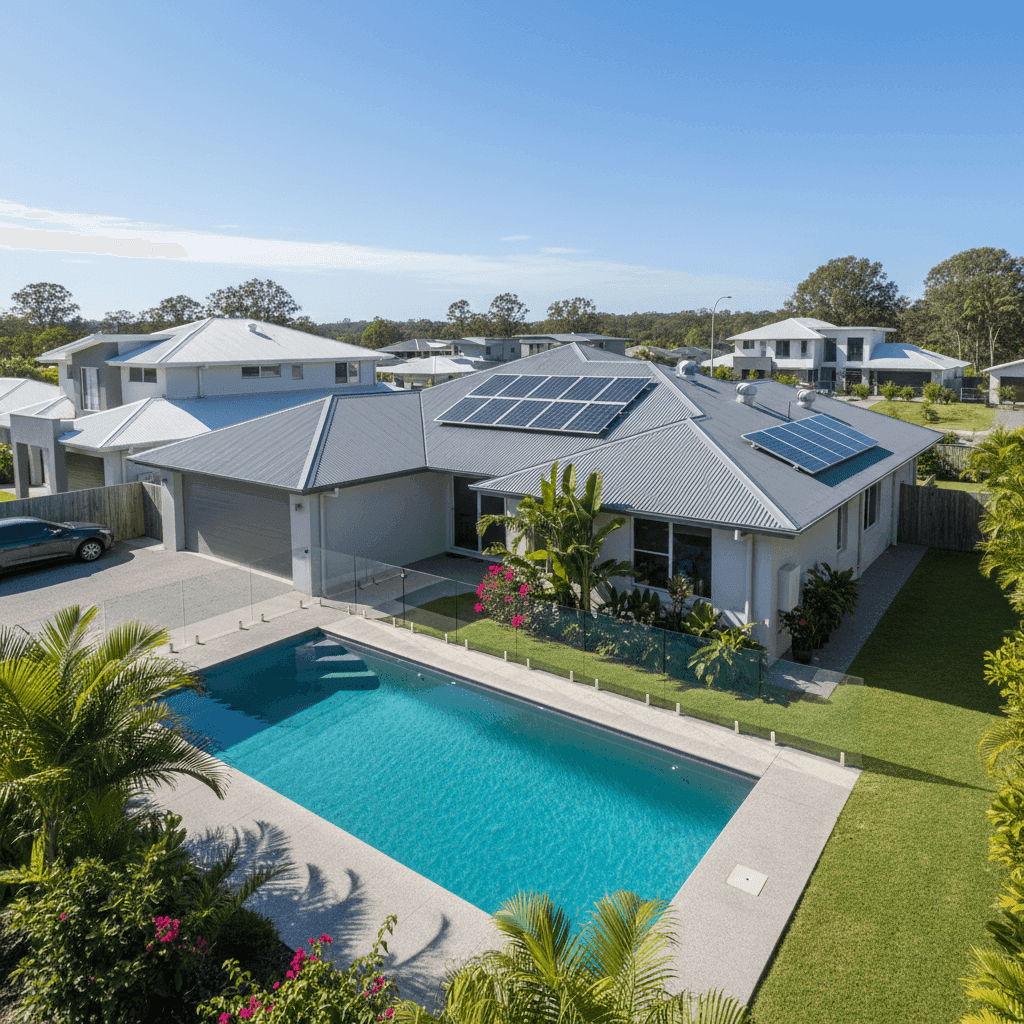

The quote in question comes in at $3,896 per year (or $373/month) for building-only cover on a 325 sqm concrete-walled, Colorbond-roofed home with a sum insured of $813,000. The building excess is $5,000.

Our price rating for this quote is CHEAP — Below Average, meaning it sits well below what most comparable properties in the area are paying. That's a meaningful result in a suburb where insurance costs are notoriously elevated.

To put it in perspective:

- The suburb average for Trinity Park is $8,275/year, and the median sits at $6,741/year

- The 25th percentile — meaning only 25% of quotes come in cheaper — is $5,471/year

- This quote, at $3,896, sits below even the cheapest quarter of quotes in the suburb

In other words, securing this premium represents a genuinely strong outcome for a Trinity Park homeowner. At roughly 47% below the suburb average, this isn't just marginally cheaper — it's a standout result.

---

How Trinity Park Compares

To understand just how significant this quote is, it helps to zoom out and look at the broader picture. You can explore the full data on the Trinity Park suburb stats page, the Queensland state overview, and national home insurance statistics.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Trinity Park (suburb) | $8,275/yr | $6,741/yr |

| LGA (Cairns) | $12,404/yr | — |

| Queensland (state) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The Cairns LGA average of $12,404/year is extraordinarily high — one of the steepest in the country — driven by the region's cyclone exposure and flood risk. Trinity Park's suburb average of $8,275 is lower than the broader LGA figure, but still well above the national average of $5,347.

It's also worth noting the large gap between Queensland's average ($9,129) and median ($3,903). This tells us that a relatively small number of very expensive quotes are pulling the average upward — likely properties in high-risk coastal or flood-prone areas. The quote analysed here, at $3,896, sits just below the state median, which is a strong position to be in for a property of this size and location.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers charge — both positively and negatively.

Cyclone Risk Zone

Trinity Park falls within a declared cyclone risk area, which is the single biggest driver of elevated premiums in this part of Queensland. Insurers price in the potential cost of wind, rain, and storm surge damage from tropical cyclones. This alone can add thousands of dollars to an annual premium compared to properties in southern Queensland or interstate.

Construction: Concrete Walls and Colorbond Roof

This home's concrete external walls are viewed favourably by insurers. Concrete is highly resistant to fire, wind, and impact damage — all relevant perils in Far North Queensland. Similarly, a steel/Colorbond roof is considered one of the more durable roofing materials, performing well in high-wind events compared to tiles, which can lift or shatter. Together, these construction materials likely contribute to a more competitive premium than a timber-framed or brick-veneer equivalent.

Slab Foundation

A concrete slab foundation provides good structural stability and, importantly, reduces the risk of underfloor flooding or pest damage. This is another factor that can work in a homeowner's favour when insurers assess risk.

Pool, Solar Panels, and Ducted Climate Control

The presence of a swimming pool, solar panels, and ducted climate control all add to the replacement value of the property — and therefore the sum insured. These features are reflected in the $813,000 building sum insured, which is a substantial figure. Underinsuring a property with these extras can leave homeowners significantly out of pocket after a major claim.

Timber and Laminate Flooring

While timber and laminate flooring adds aesthetic and resale value, it can be more susceptible to water damage than ceramic tiles. In a cyclone-prone area where storm water ingress is a real risk, this is worth keeping in mind from both an insurance and a home maintenance perspective.

---

Tips for Homeowners in Trinity Park

1. Don't Underinsure — Especially With a Pool and Solar

With a pool, solar system, and ducted air conditioning, the cost to rebuild this home from scratch is significant. Make sure your sum insured reflects today's construction costs, not what you paid for the property years ago. CoverClub's quoting tool can help you sense-check your building sum insured against current benchmarks.

2. Cyclone Preparation Can Pay Off

Some insurers offer discounts or more favourable terms for homes that meet cyclone construction standards or have undergone cyclone-proofing upgrades (such as roof tie-downs or impact-resistant glazing). If you've made improvements since 2005, make sure your insurer is aware — it could influence your premium.

3. Review Your Excess Carefully

This policy carries a $5,000 building excess, which is on the higher end. A higher excess generally reduces your premium, but it also means you'll need to cover more out of pocket before a claim kicks in. In a cyclone event where damage may be widespread, a $5,000 excess is manageable — but make sure you have that amount readily accessible.

4. Compare Quotes Annually

The fact that this quote came in well below the suburb average is a reminder that premiums vary significantly between insurers for the same property. The insurance market is competitive, and loyalty doesn't always pay. Set a reminder to compare quotes at renewal each year — even a modest saving compounds over time.

---

Get Your Own Quote

Whether you're a Trinity Park homeowner reviewing your current policy or shopping for cover on a new property, comparing quotes is the smartest first step. CoverClub makes it easy to see what multiple insurers would charge for your specific home — in seconds, without the paperwork.