Tugun is a laid-back coastal suburb tucked at the southern end of the Gold Coast, just minutes from the beach and the Queensland–New South Wales border. It's a popular spot for families and sea-changers alike, and the local housing stock reflects that — a mix of older character homes and more modern builds sitting comfortably in a relaxed beachside setting. If you own a free standing home here, understanding what you should be paying for home insurance is an important part of protecting one of your biggest assets.

This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom free standing home in Tugun (postcode 4224), compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $2,632 per year (or $252 per month) for combined home and contents cover, with a building sum insured of $426,000 and contents valued at $10,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is CHEAP — below average — which is genuinely good news for the homeowner. To put that in context:

- The suburb median for Tugun is $3,793/yr, meaning this quote sits comfortably below what most comparable properties in the area are paying.

- The suburb 25th percentile is $2,698/yr — so this quote is actually nudging below even the cheapest quarter of premiums seen locally.

- Against the Gold Coast LGA average of $8,161/yr and the QLD state average of $9,129/yr, the saving is even more striking.

It's worth noting that Tugun's suburb average premium is a very high $63,305/yr — but this figure is heavily skewed by outliers in a relatively small sample of 18 quotes. The median of $3,793/yr is a far more reliable indicator of what most homeowners pay, and against that benchmark, this quote represents solid value.

---

How Tugun Compares

To understand where this quote sits in the broader landscape, here's a quick snapshot:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,632 |

| Tugun Suburb Median | $3,793 |

| Tugun 25th Percentile | $2,698 |

| Tugun 75th Percentile | $16,610 |

| Gold Coast LGA Average | $8,161 |

| QLD State Median | $3,903 |

| National Median | $2,764 |

| National Average | $5,347 |

You can explore the full breakdown of premiums for Tugun on the Tugun suburb stats page, compare it against other Queensland postcodes on the QLD stats page, or see how it measures up nationally on the national stats page.

What stands out here is how wide the spread is in Tugun — the 75th percentile sits at $16,610/yr, more than six times the 25th percentile. This tells us that the right property features, the right insurer, and the right level of cover can make an enormous difference to what you pay. Shopping around is not just worthwhile — it's essential.

---

Property Features That Affect Your Premium

Every property is different, and insurers price risk based on a range of physical characteristics. Here's how the features of this particular home likely influence its premium:

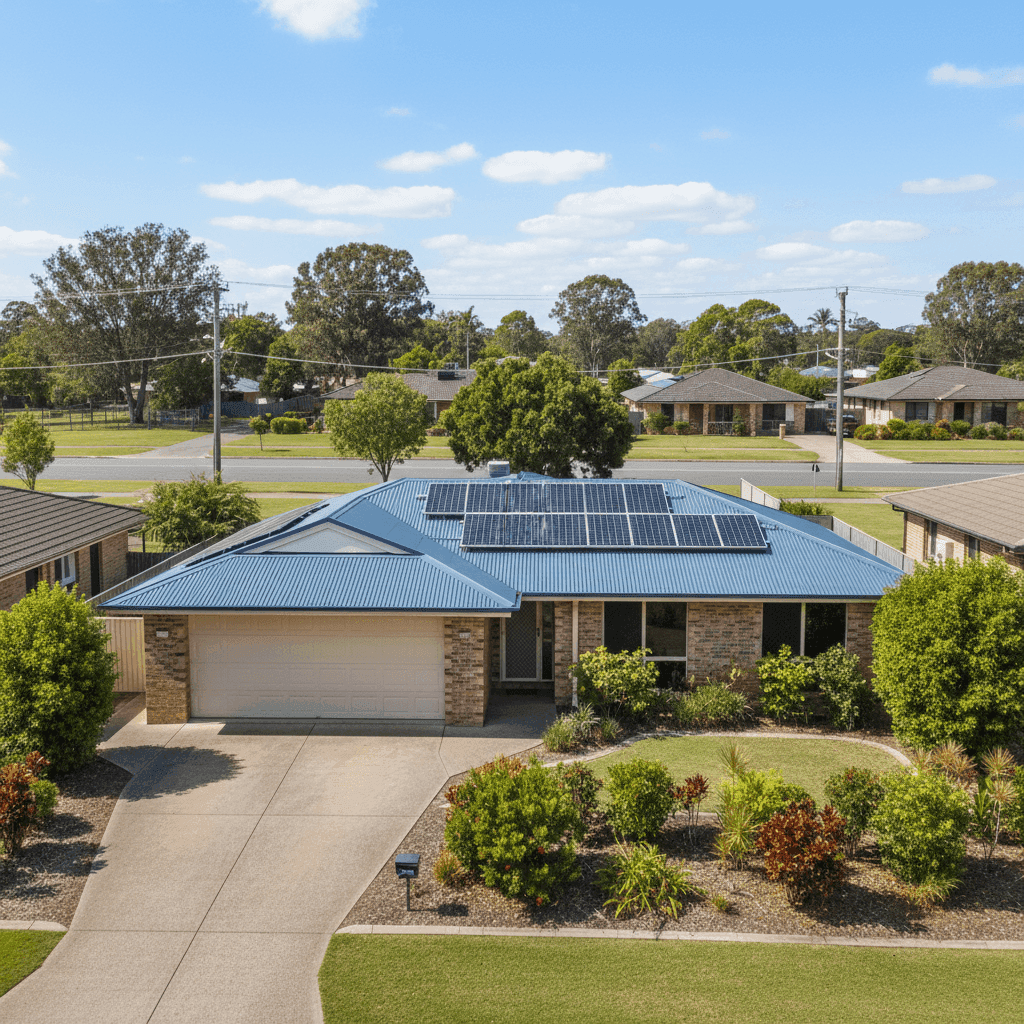

Brick Veneer Walls Brick veneer is a well-regarded construction type in the eyes of most insurers. It offers solid fire resistance and structural durability, which generally translates to more favourable underwriting compared to, say, weatherboard or clad homes.

Steel / Colorbond Roof A Colorbond steel roof is considered low-maintenance and highly durable, with good resistance to fire and wind. Insurers tend to view this positively, particularly in Queensland's harsh climate. It's a meaningful advantage over older tile roofs, which can be more susceptible to storm damage.

Stump Foundation The home sits on stumps, which is common for homes of this era (built in 1985) in South East Queensland. Stumped homes can be more vulnerable to movement and moisture-related issues over time, but they also allow for easier access and inspection — which can work in your favour when it comes to maintenance.

Timber / Laminate Flooring Timber and laminate floors are a standard feature in many Queensland homes. While they add aesthetic value, they can be more susceptible to water damage than tiles. This is worth keeping in mind when assessing your contents and building cover.

Solar Panels The presence of solar panels adds value to the property and should be factored into your building sum insured. Most standard home insurance policies cover rooftop solar panels as part of the building, but it's always worth confirming this with your insurer.

Ducted Climate Control Ducted air conditioning is a significant fixed asset and is typically covered under building insurance. Make sure your sum insured accounts for its replacement cost — ducted systems can run to several thousand dollars to replace.

No Pool, No Cyclone Risk Zone The absence of a swimming pool removes a common source of liability and maintenance claims. And while Tugun sits in Queensland, it falls outside the designated cyclone risk zone — a factor that can meaningfully reduce premiums compared to properties further north.

---

Tips for Homeowners in Tugun

1. Review your building sum insured regularly At $426,000, this policy's building sum insured needs to reflect the true cost of rebuilding — not the market value of the land. With construction costs rising across South East Queensland, it's worth getting a professional assessment every few years to avoid being underinsured. Don't forget to factor in your solar panels and ducted air conditioning.

2. Consider increasing your contents cover A contents value of $10,000 is on the lower end for a three-bedroom home. Take a room-by-room inventory of your belongings — furniture, appliances, clothing, electronics, and valuables — to make sure you're not left short after a claim.

3. Shop around at renewal time Even if your current premium is competitive, insurers regularly adjust their pricing. Set a reminder to compare quotes before your policy renews each year. What's cheap today may not be the best deal in 12 months. Use CoverClub to compare quotes and see what's available for your property.

4. Maintain your home to protect your claim Insurers can reduce or deny claims if damage is attributed to poor maintenance. For a stumped home with timber floors, keeping an eye on moisture levels, stump condition, and roof integrity is particularly important — and it can also help keep your premiums stable over time.

---

Get a Quote for Your Tugun Home

Whether you're reviewing your existing policy or shopping for cover for the first time, it pays to compare. CoverClub makes it easy to see what home and contents insurance should cost for your specific property — and to find out if you're paying more than you need to. Start your free quote comparison today and see how your premium stacks up.