If you own a free standing home in Tweed Heads, NSW 2485, you already know this corner of the country is one of Australia's most enviable places to live — perched on the Queensland border, with beaches, waterways, and a relaxed coastal lifestyle on your doorstep. But that desirable location comes with its own insurance considerations, and premiums in this postcode can vary dramatically depending on your property's characteristics and the insurer you choose.

This article breaks down a recent building insurance quote for a four-bedroom, three-bathroom free standing home in Tweed Heads, examining whether the price stacks up and what's likely driving the cost.

---

Is This Quote Fair?

The quoted annual premium for this property is $31,929 per year (or $3,060/month), covering the building only with a $1,000 excess and a sum insured of $1,046,000.

Our price rating for this quote is EXPENSIVE — above average for the area.

To put that in perspective: the suburb average for Tweed Heads sits at $14,734 per year, with a median of $7,900. This quote is more than double the local average and over four times the suburb median. Even measured against the suburb's 75th percentile — meaning 75% of quotes in the area come in below $19,190 — this premium still sits well above the pack.

That's a significant gap, and it's worth understanding what's pushing the price up before simply accepting the figure at face value.

---

How Tweed Heads Compares

Zooming out to a broader context makes the picture even clearer.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Tweed Heads (suburb) | $14,734/yr | $7,900/yr |

| Tweed LGA | $26,089/yr | — |

| NSW (state) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

You can explore full NSW home insurance statistics and national benchmarks on CoverClub.

A few things stand out here. First, Tweed Heads already commands higher-than-average premiums compared to both the state and national figures — the suburb average of $14,734 is well above the NSW average of $9,528 and nearly three times the national average of $5,347. This reflects the genuine risk profile of coastal NSW properties, including flood exposure, storm surge, and the general cost of rebuilding in a high-demand area.

Second, even within the Tweed LGA — which itself averages $26,089 per year — this quote of $31,929 is elevated. It's worth noting the suburb sample size is 14 quotes, so the data is directionally useful but not exhaustive.

The takeaway? Tweed Heads is an inherently more expensive market to insure, but this particular quote is still at the higher end even by local standards.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium, some upward and some in a more neutral direction.

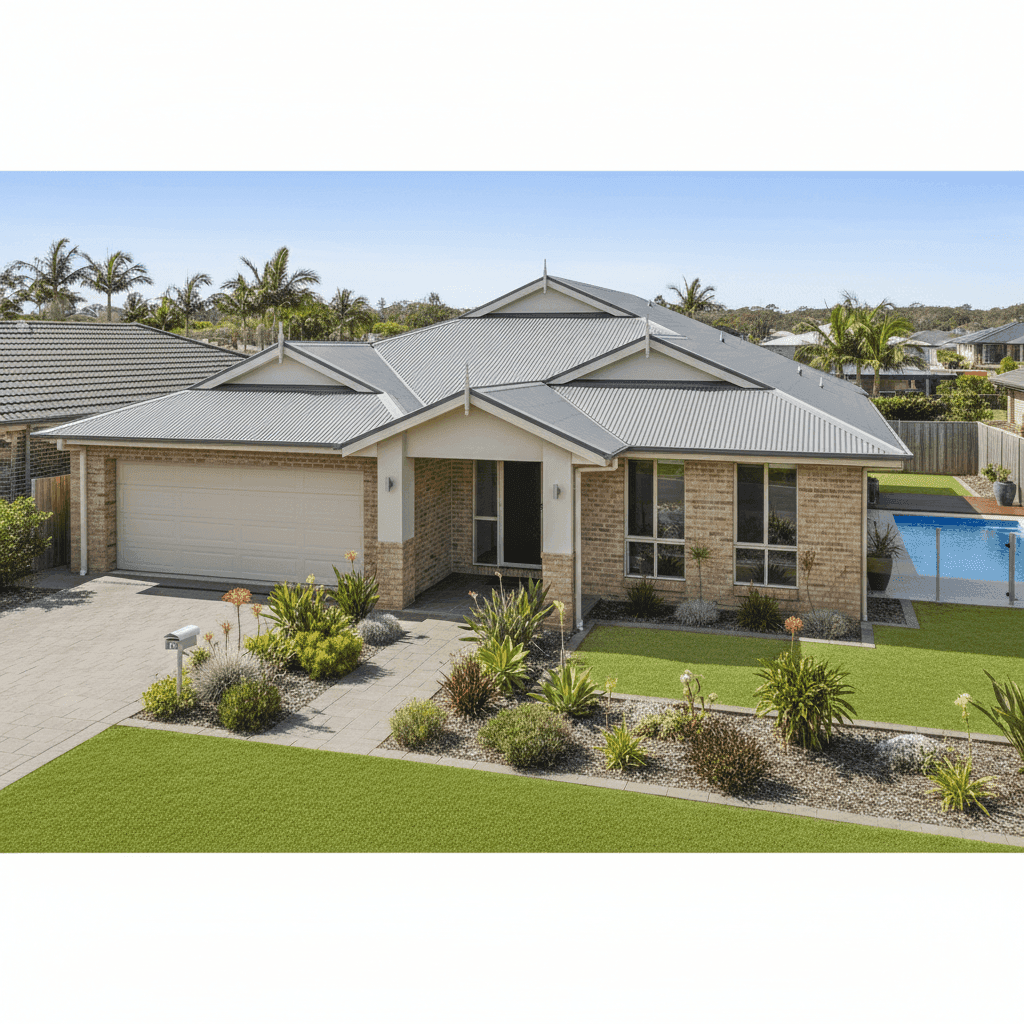

Construction year (1978): Homes built in the late 1970s predate modern building codes, particularly around cyclone and flood resilience standards. Insurers often apply loadings to older properties due to the higher likelihood of hidden wear, outdated wiring, or plumbing that may not meet current standards.

Brick veneer walls and Colorbond roof: These are generally considered solid, low-maintenance construction materials. Brick veneer is a common and well-regarded wall type in Australia, and Colorbond steel roofing is durable and fire-resistant. These features typically don't attract negative loadings and may actually be viewed favourably by insurers compared to, say, weatherboard or fibrous cement.

Slab foundation: A concrete slab is standard for this era and region. It's generally considered stable, though in flood-prone areas insurers will consider how the slab sits relative to flood levels.

Swimming pool: Pools add replacement value to the sum insured and can also introduce liability considerations depending on the policy. With a sum insured of $1,046,000 on a 244 sqm home, the pool and associated infrastructure are likely factored into the rebuild cost.

Ducted climate control: A ducted air conditioning system is a significant fixed asset. It adds to the replacement cost of the building and can be expensive to repair or replace after storm or water damage events.

Building size (244 sqm): At 244 sqm, this is a generously sized family home. Combined with four bedrooms, three bathrooms, and standard fittings, the sum insured of $1,046,000 reflects a substantial rebuild cost — which directly flows through to the premium.

Location — Tweed Heads: Proximity to water, whether ocean, river, or estuary, is one of the most significant premium drivers in coastal NSW. Flood mapping, storm surge risk, and the general exposure of properties in the Tweed region all contribute to elevated base rates.

---

Tips for Homeowners in Tweed Heads

If you're looking to get better value on your home insurance, here are four practical steps worth considering.

1. Shop around — seriously. The spread of quotes in Tweed Heads is enormous, with premiums ranging from around $6,500 at the 25th percentile to over $19,000 at the 75th percentile. A quote at $31,929 suggests there may be significantly cheaper options available for a comparable level of cover. Comparing quotes on CoverClub takes minutes and could save thousands.

2. Review your sum insured carefully. Over-insuring is a common issue. While you should always ensure your sum insured covers the full cost to rebuild (not the market value of the land), it's worth getting a professional building replacement cost estimate to confirm $1,046,000 is accurate for your specific property. Both under- and over-insuring carry risks.

3. Ask about flood and storm excess options. In coastal and riverine areas like Tweed Heads, insurers sometimes offer policies with higher specific excesses for flood or storm events in exchange for a lower base premium. This can be a reasonable trade-off if you have a strong emergency fund and want to reduce ongoing costs.

4. Consider mitigation improvements. Upgrades such as storm shutters, improved drainage, or roof tie-down systems can sometimes attract premium discounts, particularly for older homes. It's worth asking your insurer directly what risk mitigation measures they recognise — especially given the 1978 construction date.

---

Ready to Find a Better Deal?

A premium of $31,929 per year is a significant household expense, and our analysis suggests there may be room to do better. Whether you're renewing soon or just want to benchmark your current policy, CoverClub makes it easy to compare home insurance quotes across Australia.

Get a quote for your Tweed Heads home today and see how your premium stacks up against the market — it only takes a few minutes and could make a meaningful difference to your budget.