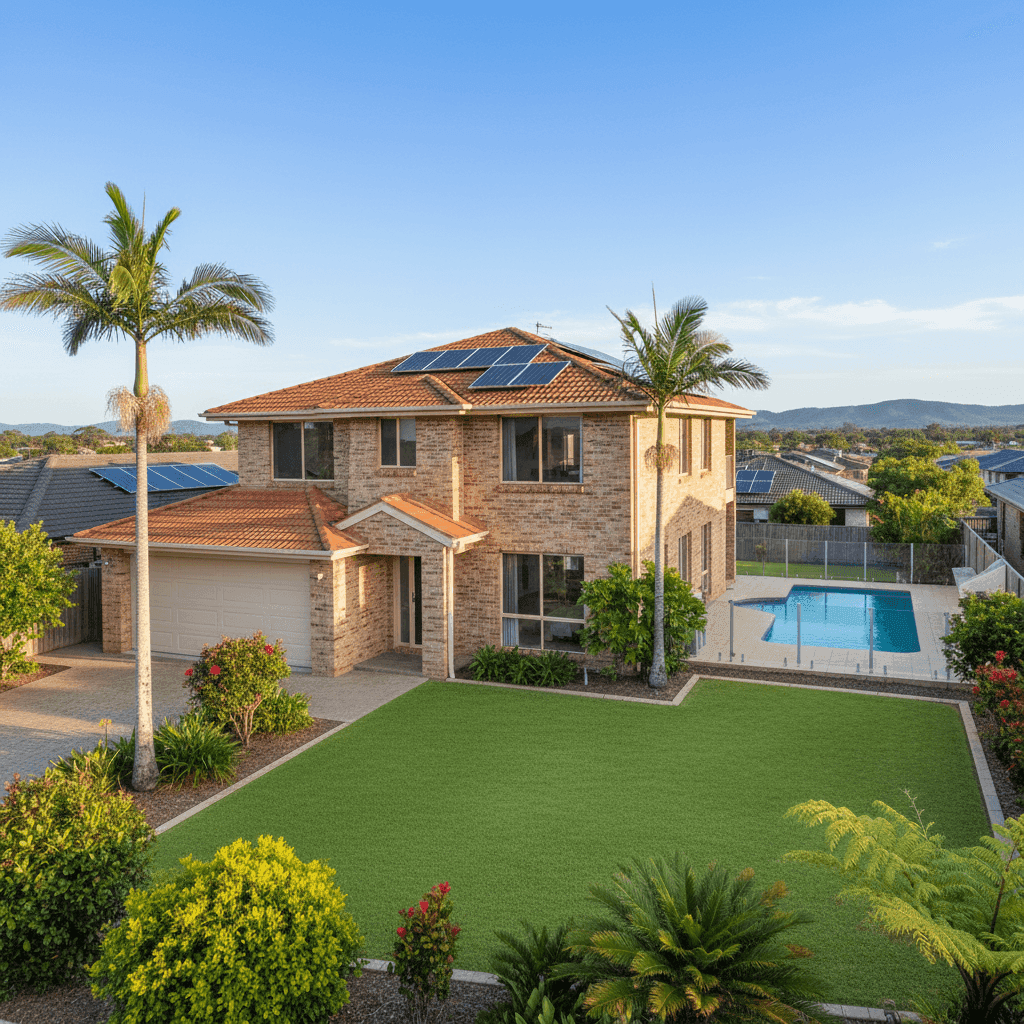

Tweed Heads South sits in one of the most sought-after corners of New South Wales — a sun-drenched coastal community on the Queensland border that blends relaxed lifestyle living with real exposure to the elements. For owners of free standing homes in this postcode, understanding what drives home insurance costs is more important than ever. This article breaks down a real building insurance quote for a four-bedroom, two-bathroom home in Tweed Heads South (NSW 2486) and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question is $5,495 per year (or $527 per month) for building-only cover, with a $2,000 building excess and a sum insured of $695,000. Our price rating for this quote is EXPENSIVE — above average.

To understand why, it helps to look at where this figure sits relative to what other homeowners in the area are paying. Based on 34 quotes collected for Tweed Heads South, the suburb median premium is $2,999 per year — meaning this quote is roughly 83% higher than the typical price paid by neighbours in the same postcode. It also sits above the suburb's 75th percentile of $4,741 per year, placing it firmly in the top quarter of quotes for the area.

That said, it's worth noting that the suburb average premium is a striking $39,104 per year — a figure heavily skewed by a small number of very high-cost outliers in the 34-quote sample. The median is a far more reliable benchmark for most homeowners, and against that measure, this quote is clearly on the pricier side.

For a property with a $695,000 sum insured, the annual cost works out to roughly 0.79% of the insured value — a ratio that is higher than what many comparable properties attract, and a signal that there may be room to shop around.

---

How Tweed Heads South Compares

Zooming out to a broader view helps put this quote in perspective.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Tweed Heads South (2486) | $39,104/yr | $2,999/yr |

| Tweed LGA | $26,089/yr | — |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

You can explore the full NSW home insurance statistics or browse national home insurance data to see how your situation compares at a broader level.

A few things stand out from this table. First, both the Tweed LGA and the Tweed Heads South suburb averages are dramatically higher than the NSW and national figures — a reflection of the elevated risk profile that coastal and near-coastal properties in this region carry. Flood, storm surge, and severe weather events are genuine considerations for insurers pricing policies in the Northern Rivers and Tweed corridor.

Second, while this particular quote of $5,495 is above the suburb median, it is actually very close to the national average of $5,347 — suggesting that on a national scale, the premium is not wildly out of line. The real question is whether a better deal is available for this specific property, and the answer is almost certainly yes with the right comparison approach.

---

Property Features That Affect Your Premium

Several characteristics of this property will be influencing the premium, both positively and negatively.

Brick veneer construction with a tiled roof is generally viewed favourably by insurers. Brick veneer offers solid fire resistance and structural durability, while tiles are considered more resilient than Colorbond or corrugated iron in certain weather scenarios. These features typically attract more competitive premiums compared to timber-framed or clad homes.

Slab foundation is standard for homes of this era and construction type in coastal NSW, and it presents no particular red flags for insurers. The 1998 build year means the property is post-major building code updates but old enough that some components — roofing, plumbing, electrical — may be approaching the age where insurers factor in maintenance risk.

Timber and laminate flooring can increase the cost of a claim if water damage occurs, as these materials are more susceptible to warping and swelling than tiles. This is worth keeping in mind given the region's exposure to heavy rainfall events.

The swimming pool adds liability exposure and can slightly elevate premiums, particularly if the policy includes legal liability cover for pool-related incidents. Solar panels are another consideration — they add to the replacement cost of the building and can complicate roof claims, which may be reflected in the sum insured and the premium. The ducted climate control system similarly adds to the overall rebuild cost and is appropriately factored into the $695,000 sum insured.

It's also worth noting that Tweed Heads South is not classified as a cyclone risk area, which is a meaningful positive distinction compared to properties further north in Queensland. However, the region does sit within a zone that experiences significant storm activity, particularly during La Niña years.

---

Tips for Homeowners in Tweed Heads South

1. Compare at least three to four quotes before renewing. The wide spread between the 25th percentile ($1,843/yr) and the 75th percentile ($4,741/yr) in this suburb tells you that insurers price this postcode very differently. A single quote — especially at renewal — is rarely the best available price. Use a comparison service to see what multiple insurers would offer for the same property.

2. Review your sum insured carefully. At $695,000 for a 139 sqm home, the insured value works out to roughly $5,000 per square metre — which is on the higher end for a standard-quality fit-out. It's worth getting an independent building replacement cost estimate to ensure you're neither underinsured nor paying a premium on an inflated figure.

3. Ask about discounts for security and risk mitigation. Some insurers offer reduced premiums for homes with monitored alarm systems, deadbolts, or ember guards on vents. Given the storm exposure in this region, demonstrating that you've invested in resilience measures (such as roof tie-downs or water-resistant flooring) may also support a better rate with certain providers.

4. Consider a higher excess to reduce your annual premium. The current building excess is $2,000. Increasing this to $2,500 or even $5,000 can meaningfully reduce your annual premium if you're comfortable self-insuring smaller claims. For a home in good condition with no recent claim history, this is often a sensible trade-off.

---

Ready to Find a Better Rate?

Whether you're renewing your policy or insuring for the first time, it pays to compare. CoverClub makes it easy to see how your quote stacks up and to access competitive building insurance options tailored to your property. Get a quote today at CoverClub and find out if you could be paying less for the same level of cover.