Nestled along the Maroochy River on Queensland's Sunshine Coast, Twin Waters is a sought-after suburb known for its canals, golf course, and relaxed coastal lifestyle. For homeowners in this area, protecting a well-appointed free standing home with the right insurance cover is an important financial decision — and understanding whether you're paying a fair premium can save you hundreds of dollars a year.

This article breaks down a recent home and contents insurance quote for a four-bedroom, three-bathroom free standing home in Twin Waters (QLD 4564), examining how it stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The quoted annual premium of $4,628 (or $437/month) covers both building and contents, with a building sum insured of $1,079,000 and contents valued at $200,000. Both the building and contents excess are set at $1,000 — a fairly standard arrangement.

CoverClub's pricing analysis rates this quote as FAIR — Around Average, and the numbers back that up. The premium sits just 5.8% above the Twin Waters suburb average of $4,374/yr and about 9% above the suburb median of $4,246/yr. It falls comfortably within the interquartile range for the suburb — between the 25th percentile of $3,355/yr and the 75th percentile of $5,267/yr — meaning it's neither a bargain nor an outlier.

In plain terms: this quote is in the middle of the pack for Twin Waters. There's room to potentially do better, but there's no cause for alarm either. It's worth shopping around to see if a lower premium is available for equivalent cover.

---

How Twin Waters Compares

To put this quote in context, it helps to zoom out and look at the broader insurance landscape across Queensland and nationally.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Twin Waters (4564) | $4,374/yr | $4,246/yr |

| Sunshine Coast LGA | $7,249/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The Queensland state average of $9,129/yr is extraordinarily high — heavily skewed by cyclone-prone regions in Far North Queensland, where premiums can be eye-watering. The state median of $3,903/yr is a far more representative figure for most Queensland homeowners, and the Twin Waters quote sits only modestly above it.

Compared to the national average of $5,347/yr, this quote is actually below average — a positive sign. And while the national median of $2,764/yr looks attractive, it reflects the many lower-risk, lower-value properties across the country, which aren't a fair comparison for a well-appointed 244 sqm home with above-average fittings in a desirable coastal suburb.

Interestingly, the Sunshine Coast LGA average of $7,249/yr is considerably higher than the Twin Waters suburb average, suggesting that Twin Waters itself may benefit from relatively favourable risk characteristics compared to other parts of the Sunshine Coast — such as beachfront or flood-prone pockets.

---

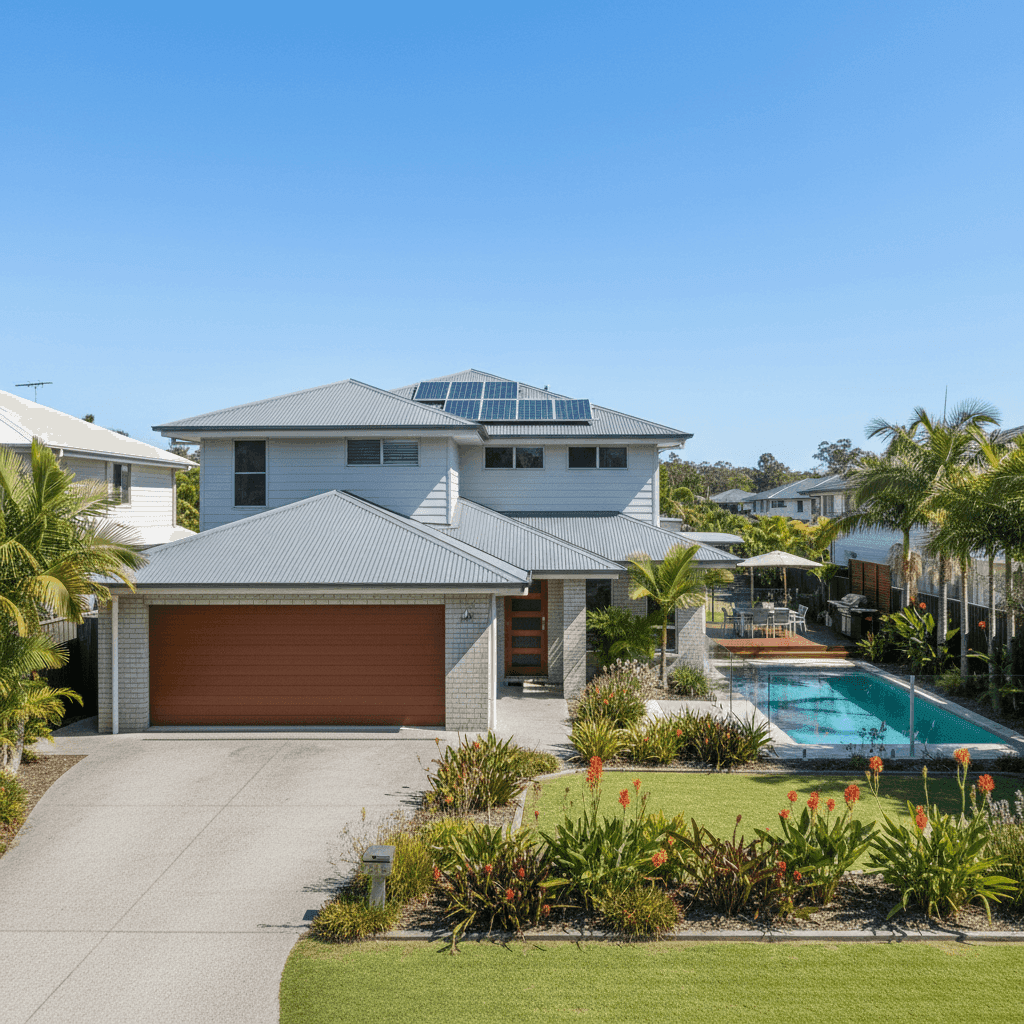

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on the quoted premium, both positively and negatively.

Building Size & Sum Insured

At 244 sqm with a building sum insured of $1,079,000, this is a substantial home. A higher sum insured directly increases the premium, as the insurer is taking on greater financial exposure. Above-average fittings — think stone benchtops, quality cabinetry, and premium fixtures — also push rebuild costs (and therefore premiums) higher.

Construction Type

Brick veneer walls and a steel/Colorbond roof are generally viewed favourably by insurers. Brick veneer offers solid fire resistance and structural durability, while Colorbond roofing is low-maintenance and resilient in Australian conditions. Together, they typically attract more competitive premiums compared to timber-framed or older construction types.

Slab Foundation

A concrete slab foundation is standard for homes of this era and is generally considered a low-risk construction method by insurers — particularly in non-flood-prone areas.

Pool, Solar Panels & Ducted Climate Control

These features add value to the property but also increase replacement costs. A swimming pool introduces some liability considerations, while solar panels add to the building sum insured and can be affected by storm or hail damage. Ducted climate control is a significant fixture that contributes to the above-average fittings rating and replacement value.

No Cyclone Risk

Twin Waters falls outside designated cyclone risk zones — a significant advantage for Queensland homeowners. Cyclone-rated premiums in parts of North Queensland can be many multiples of what's quoted here, so this property benefits considerably from its location.

Timber & Laminate Flooring

From a contents perspective, timber and laminate flooring can be more susceptible to water damage than tiles, which is worth keeping in mind when assessing contents cover and the adequacy of the $200,000 sum.

---

Tips for Homeowners in Twin Waters

1. Review Your Building Sum Insured Regularly

Construction costs in South East Queensland have risen sharply in recent years. With a home of this size and quality, it's worth having your building sum insured reviewed annually — ideally using a quantity surveyor's estimate — to ensure you're not underinsured. Rebuilding a 244 sqm home with above-average fittings could easily exceed $1 million in today's market.

2. Check Your Contents Cover is Adequate

$200,000 in contents cover sounds substantial, but for a four-bedroom, three-bathroom home with quality fittings, it can go quickly. Take time to itemise high-value items like jewellery, electronics, artwork, and furniture. Many homeowners discover they're underinsured for contents when they actually sit down and add it up.

3. Compare Quotes Before Renewal

A "fair" rating means this premium is around average — not that it's the best available. With 12 quotes sampled in the Twin Waters area, there's a reasonable spread of pricing. Using a comparison tool like CoverClub at renewal time could help you find equivalent cover at a lower price, potentially saving several hundred dollars a year.

4. Ask About Discounts for Security & Safety Features

Insurers often offer discounts for homes with monitored alarm systems, deadbolts, and smoke detectors. If you've made upgrades to your home's security or safety features since your last policy, it's worth flagging these with your insurer or when getting new quotes — they may reduce your premium.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for cover for the first time, CoverClub makes it easy to compare home and contents insurance quotes tailored to your property. Get a quote today and see how much you could save — or simply confirm that your current cover is competitively priced. You can also explore detailed insurance pricing data for Twin Waters, Queensland, and across Australia on the CoverClub stats pages.