Tyabb is a semi-rural township on Victoria's Mornington Peninsula — known for its antique stores, equestrian properties, and relaxed lifestyle just an hour south-east of Melbourne. It's also a suburb where home insurance costs can vary quite a bit depending on your property's features, age, and construction. This article breaks down a real home and contents insurance quote for a four-bedroom, free-standing home in Tyabb (postcode 3913), comparing it against local, state, and national benchmarks to help you understand whether you're paying a fair price.

---

Is This Quote Fair?

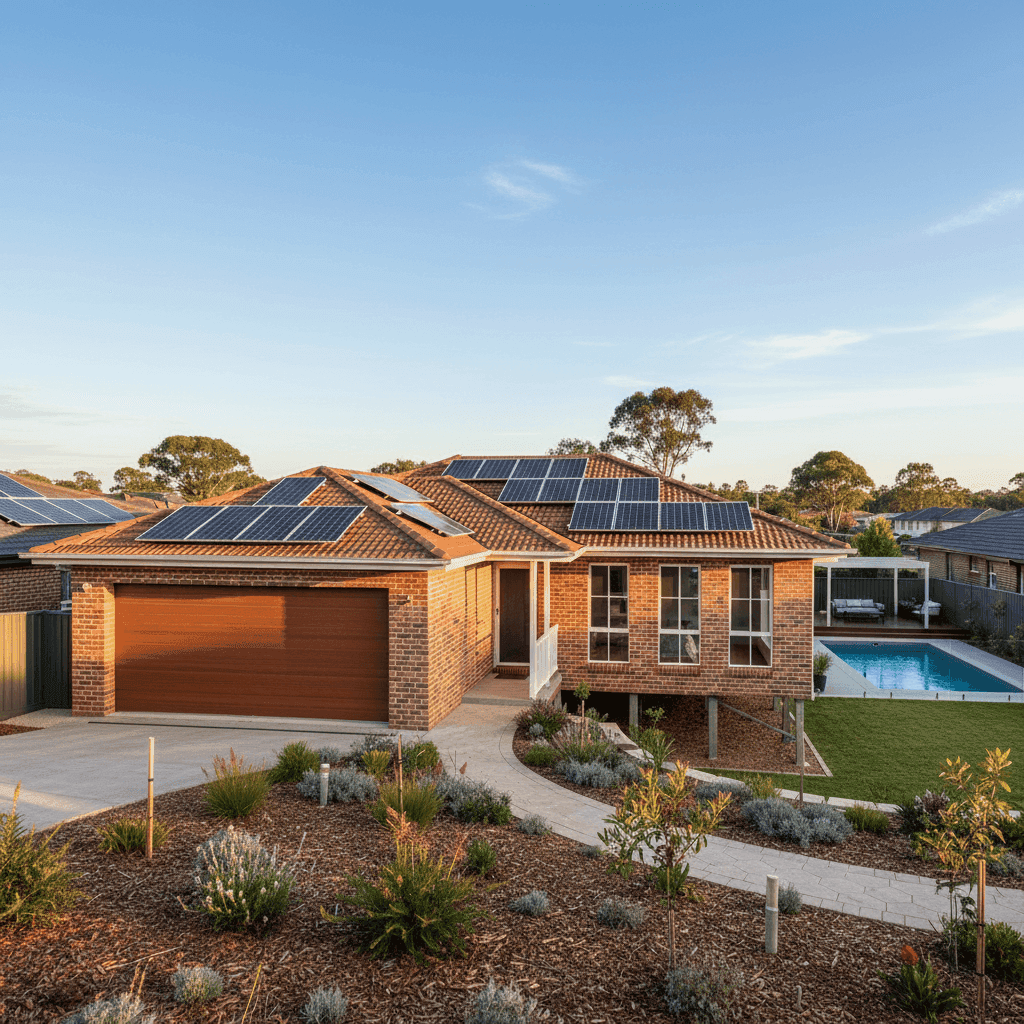

The annual premium for this property came in at $5,169 per year (or roughly $505/month), covering both building and contents. The building is insured for $1,750,000 and contents for $235,000, with a $1,000 excess on each.

CoverClub's pricing engine rates this quote as Fair — Around Average, which is a reasonable outcome for a property of this size and specification. It's sitting above the suburb average of $4,420/yr and the suburb median of $4,557/yr, but comfortably within the suburb's interquartile range of $3,361–$5,451/yr. That means roughly half of comparable Tyabb properties are paying between those two figures — and this quote lands in the upper half of that band.

The higher-than-median premium is largely explained by the property's above-average fittings quality, generous building sum insured of $1.75 million, and additional risk features like a swimming pool and solar panels. These aren't red flags — they're simply characteristics that insurers price accordingly.

---

How Tyabb Compares

Understanding your premium in context is one of the most useful things you can do as a homeowner. Here's how this quote stacks up across different comparison points:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Tyabb (3913) | $4,420/yr | $4,557/yr |

| Victoria (VIC) | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

| Mornington Peninsula LGA | $2,652/yr | — |

A few things stand out here. First, Tyabb premiums are noticeably higher than the broader Victorian state average of $3,000/yr — reflecting the Peninsula's unique risk profile, including coastal proximity and the higher rebuild costs associated with larger, well-appointed homes in the area.

Second, the national average premium of $5,347/yr is actually higher than this quote — driven upward by high-cost postcodes in Queensland, Western Australia, and Northern Territory where cyclone, flood, and bushfire risk can push premiums into the tens of thousands. On a national scale, $5,169/yr is quite reasonable.

Third, the Mornington Peninsula LGA average of $2,652/yr is considerably lower than the Tyabb suburb average. This likely reflects the mix of smaller, lower-value properties across the broader LGA bringing the average down. For a 214 sqm home with above-average fittings and a $1.75M building sum insured, a premium well above the LGA average is entirely expected.

You can explore more localised data on the Tyabb suburb stats page.

> Note: The suburb sample size for Tyabb is 15 quotes, which is a reasonable dataset but still relatively small. Averages may shift as more data is collected.

---

Property Features That Affect Your Premium

This property has a number of characteristics that directly influence how insurers assess risk and calculate premiums. Here's a breakdown of the key factors at play:

Brick Veneer Walls & Tiled Roof

Brick veneer construction is one of the most common wall types in Victoria and is generally viewed favourably by insurers — it offers good fire resistance and structural durability. A tiled roof similarly signals longevity and resilience. Together, these materials typically attract more competitive premiums than timber weatherboard or metal cladding alternatives.

Stump Foundation

The property sits on stumps, which is common for homes of this era (built in 1988) on the Mornington Peninsula. Stumped foundations can be more susceptible to movement and moisture-related issues over time, and some insurers may factor this into their pricing. It's worth ensuring your policy covers underpinning and restumping scenarios where relevant.

Swimming Pool

A pool adds both value and liability to a property. Insurers consider pools when calculating contents and liability risk — particularly in relation to accidental damage and public liability coverage. Make sure your policy explicitly covers pool-related incidents.

Solar Panels

With solar panels installed, it's essential your home insurance policy covers these as part of the building sum insured. Solar systems can cost $8,000–$20,000+ to replace, and not all policies include them automatically. Confirm this with your insurer.

Above-Average Fittings

Above-average fittings — think stone benchtops, quality appliances, ducted climate control, and premium fixtures — increase both the rebuild cost and the contents valuation. This property's $1.75M building sum insured reflects the cost of restoring a well-appointed home to its original standard, which is the right approach to avoid being underinsured.

Elevation

The property is slightly elevated (less than 1 metre), which can offer modest protection against surface-water flooding. While this won't dramatically reduce your premium, it's a positive factor in flood risk assessments.

---

Tips for Homeowners in Tyabb

1. Review your building sum insured regularly Construction costs have risen sharply in recent years. A sum insured that was accurate two or three years ago may now fall short of what it would actually cost to rebuild your home. Use a building cost calculator or speak with a quantity surveyor to ensure your $1.75M figure still reflects current rebuild costs — including your above-average fittings.

2. Confirm solar panels and pool equipment are covered Ask your insurer directly whether solar panels are included under the building definition and whether pool equipment (pumps, filters, heating systems) is covered for accidental damage. If not, you may need to add these as specified items.

3. Check your flood and storm cover Tyabb and the broader Mornington Peninsula can experience significant rainfall and storm events. Ensure your policy includes storm surge and flash flooding cover — these are sometimes excluded or subject to separate sub-limits, particularly for stumped homes where water ingress can be a concern.

4. Compare quotes before renewal Insurers don't always reward loyalty with competitive pricing. With a premium at this level, even a 10–15% saving would put hundreds of dollars back in your pocket each year. CoverClub makes it easy to compare multiple quotes side by side — so you're never paying more than you need to.

---

Ready to Compare?

Whether you're reviewing your existing policy or shopping around for the first time, CoverClub helps Australian homeowners find the right cover at a fair price. Get a home insurance quote now and see how your premium stacks up against your neighbours in Tyabb and across Victoria.