If you own a free standing home in Tyers, VIC 3844, you already know the appeal — a quiet Gippsland community surrounded by natural beauty, close to Lake Narracan and within easy reach of the Latrobe Valley. But living in a regional Victorian setting also means understanding how your location, property features, and local risk environment shape the cost of your home insurance.

This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Tyers — and compares it against what other homeowners in the suburb, across Victoria, and nationally are paying. Whether you're reviewing your current policy or shopping for the first time, this analysis will help you understand whether you're getting a fair deal.

---

Is This Quote Fair?

The quote in question comes in at $1,300 per year (or approximately $123 per month) for combined home and contents cover. The building is insured for $550,000, contents for $20,000, with a building excess of $4,000 and a contents excess of $2,000.

Our price rating for this quote? Cheap — well below average.

To put that in perspective: the average home insurance premium for properties in the Tyers suburb sits at $3,893 per year, with a median of $3,952. This quote is paying roughly one-third of what most Tyers homeowners are quoted — a remarkable saving of over $2,500 annually.

Even against the broader Victorian state average of $2,921 per year, this premium is less than half. And compared to the national average of $2,965 per year, the savings remain substantial.

So what's driving such a competitive premium? A combination of favourable property characteristics, a relatively modest contents value, and the insurer's own pricing model all play a role — but the property itself is doing a lot of the heavy lifting here.

---

How Tyers Compares

Tyers sits within the Wellington Local Government Area (LGA), which carries an average premium of $4,409 per year — notably higher than both the Victorian and national averages. This elevated LGA average likely reflects the bushfire and flood risk exposure that's common across parts of the Wellington region, including proximity to forested areas and waterways.

Here's a quick snapshot of how the premiums stack up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,300 |

| Tyers Suburb Average | $3,893 |

| Tyers Suburb Median | $3,952 |

| Tyers 25th Percentile | $3,343 |

| VIC State Average | $2,921 |

| National Average | $2,965 |

| Wellington LGA Average | $4,409 |

It's worth noting that the Tyers suburb data is based on a sample of 14 quotes, so while it's a useful guide, the pool is relatively small. Still, the consistent pattern — suburb, LGA, state, and national figures all sitting well above this quote — reinforces that this is genuinely a below-market result.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour from a risk and pricing perspective.

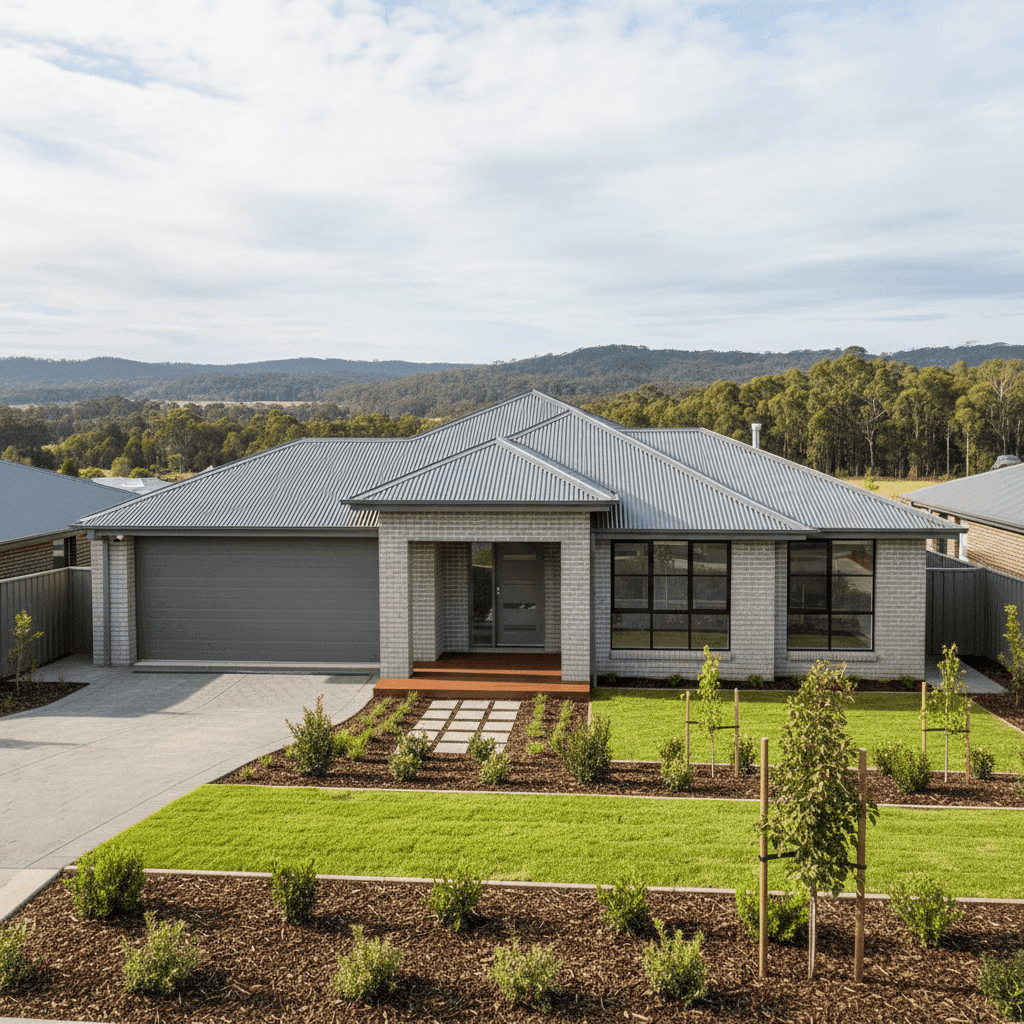

Newly built construction (2023) A home built in 2023 benefits from modern building codes, updated fire and safety standards, and contemporary construction practices. Insurers generally view newer homes as lower risk — there's less likelihood of ageing infrastructure issues like old wiring, deteriorating plumbing, or structural wear that can drive up claims.

Brick veneer external walls Brick veneer is one of the more insurer-friendly wall materials in Australia. It offers solid fire resistance and durability, which can translate to lower premiums compared to properties with timber or weatherboard cladding — particularly relevant in bushfire-prone regions like Gippsland.

Steel/Colorbond roof A Colorbond roof is another tick in the "low risk" column. It's non-combustible, highly durable, resistant to extreme weather, and requires minimal maintenance. Compared to tiled or older roofing materials, Colorbond is generally well-regarded by underwriters.

Concrete slab foundation Slab foundations are considered structurally sound and are less susceptible to subsidence or pest-related damage than elevated timber stumps. This reduces the likelihood of costly structural claims.

Modest contents value ($20,000) The contents sum insured is relatively conservative for a four-bedroom home. A lower contents value means less exposure for the insurer on that component of the policy, which contributes to keeping the overall premium down.

No pool, no solar panels The absence of a swimming pool removes a significant liability risk factor. Solar panels, while increasingly common, can add complexity and cost to building insurance due to replacement and installation costs. Neither applies here, which simplifies the risk profile.

No cyclone risk area Tyers is not in a designated cyclone risk zone, which eliminates one of the premium loading factors that affect properties in northern Australia.

---

Tips for Homeowners in Tyers

1. Review your building sum insured regularly A $550,000 building sum insured for a 277 sqm home built in 2023 is worth checking against current construction costs. Rebuild costs — not market value — should drive your sum insured. With construction costs rising in regional Victoria, it's worth getting a building replacement estimate every year or two to avoid being underinsured.

2. Understand your bushfire exposure Tyers is in the Gippsland region, which has a documented history of bushfire risk. Even if your specific property has a manageable BAL (Bushfire Attack Level) rating, it's worth confirming with your insurer exactly what bushfire-related events are covered and whether any exclusions apply. Maintaining a defensible space around your home is both a safety and insurance consideration.

3. Consider whether your contents cover is adequate $20,000 in contents cover is on the lower end for a four-bedroom home. Take stock of your furniture, appliances, clothing, electronics, and valuables. Many homeowners underestimate their contents — a room-by-room audit often reveals the true replacement cost is higher than expected. Increasing your contents sum insured may add only a modest amount to your premium.

4. Don't let your policy auto-renew without shopping around Even if you're currently on a great rate, insurers can adjust premiums significantly at renewal. The Tyers suburb average of $3,893 shows that many homeowners in the area are paying far more than necessary. Make it a habit to compare quotes annually — a few minutes on CoverClub could save you hundreds of dollars.

---

Compare Your Home Insurance Quote Today

Whether you're a Tyers local or own a property anywhere in regional Victoria, it pays to know where your premium sits relative to the market. The quote analysed here is a strong result — but every property is different, and your own circumstances may yield an even better outcome with the right insurer.

[Get a home insurance quote on CoverClub](https://coverclub.com.au/?focus=address) and see how your property compares against suburb, state, and national benchmarks in seconds. It's free, fast, and could save you a significant amount at your next renewal.