Umina Beach, nestled on the Central Coast of New South Wales, is a popular coastal suburb that blends relaxed beachside living with easy access to Sydney. For homeowners here, protecting a free standing home is a serious financial consideration — and understanding whether you're paying a fair price for building insurance can make a real difference to your budget.

This article breaks down a recent building-only insurance quote for a three-bedroom, three-bathroom free standing home in Umina Beach (postcode 2257), and puts the numbers into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quoted annual premium of $2,459 (or roughly $229 per month) for $500,000 in building cover has been rated Fair — Around Average based on current market data.

To understand what "fair" actually means here, it helps to look at what other homeowners in the same suburb are paying. The suburb median premium for Umina Beach sits at $2,587 per year, which places this quote comfortably just below the midpoint. The suburb average is higher again at $3,353/yr, pulled upward by some significantly more expensive policies at the top end of the market.

At $2,459, this quote lands between the 25th percentile ($1,646/yr) and the median ($2,587/yr) — meaning it's better than roughly half of the quotes seen in this suburb, but there are still cheaper options available for those willing to shop around. It's not a standout bargain, but it's certainly not overpriced either.

The $1,000 building excess is a standard figure for Australian home insurance policies. Opting for a higher excess is one lever homeowners can pull to reduce their annual premium, though it does mean more out-of-pocket cost if a claim arises.

---

How Umina Beach Compares

One of the more striking takeaways from this data is just how favourably Umina Beach compares to broader benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Umina Beach (suburb) | $3,353/yr | $2,587/yr |

| Central Coast LGA | $8,387/yr | — |

| NSW (state) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

The NSW state average of $9,528 per year is dramatically higher than what most Umina Beach homeowners are paying. This is largely driven by high-risk postcodes elsewhere in the state — areas prone to flooding, bushfire, or cyclone activity — which push the average skyward. The national average of $5,347/yr tells a similar story.

Interestingly, the Central Coast LGA average of $8,387/yr is significantly higher than the Umina Beach suburb average of $3,353/yr. This suggests that other parts of the Central Coast council area carry considerably more risk — or attract higher premiums — than Umina Beach specifically. For homeowners in this suburb, that's a reassuring sign.

It's worth noting that this analysis is based on a sample of 24 quotes for the Umina Beach suburb, which provides a reasonable but not exhaustive picture of the local market. Premiums can vary considerably depending on the insurer, the level of cover, and specific property characteristics.

---

Property Features That Affect Your Premium

Several features of this particular property are worth examining through an insurance lens.

Concrete external walls are generally viewed favourably by insurers. Concrete is highly resistant to fire, impact damage, and general wear — all factors that reduce the likelihood and cost of claims. Combined with a steel/Colorbond roof, this home has a construction profile that many insurers consider lower risk than, say, a timber-framed home with a tiled roof.

The slab foundation is another positive. Slab-on-ground construction tends to be less susceptible to subsidence and pest-related damage compared to raised or suspended foundations, which can be a factor in coastal areas where soil conditions vary.

Timber and laminate flooring can be a consideration in the event of water damage — these materials are more vulnerable to moisture than tiles — but this is a relatively minor factor in overall premium calculations.

The above average fittings quality is likely contributing to the $500,000 sum insured. Higher-quality fixtures, fittings, and finishes cost more to repair or replace, so it's important that the building sum insured accurately reflects what it would cost to rebuild the home to the same standard. Underinsurance is a genuine risk for homes with premium fittings.

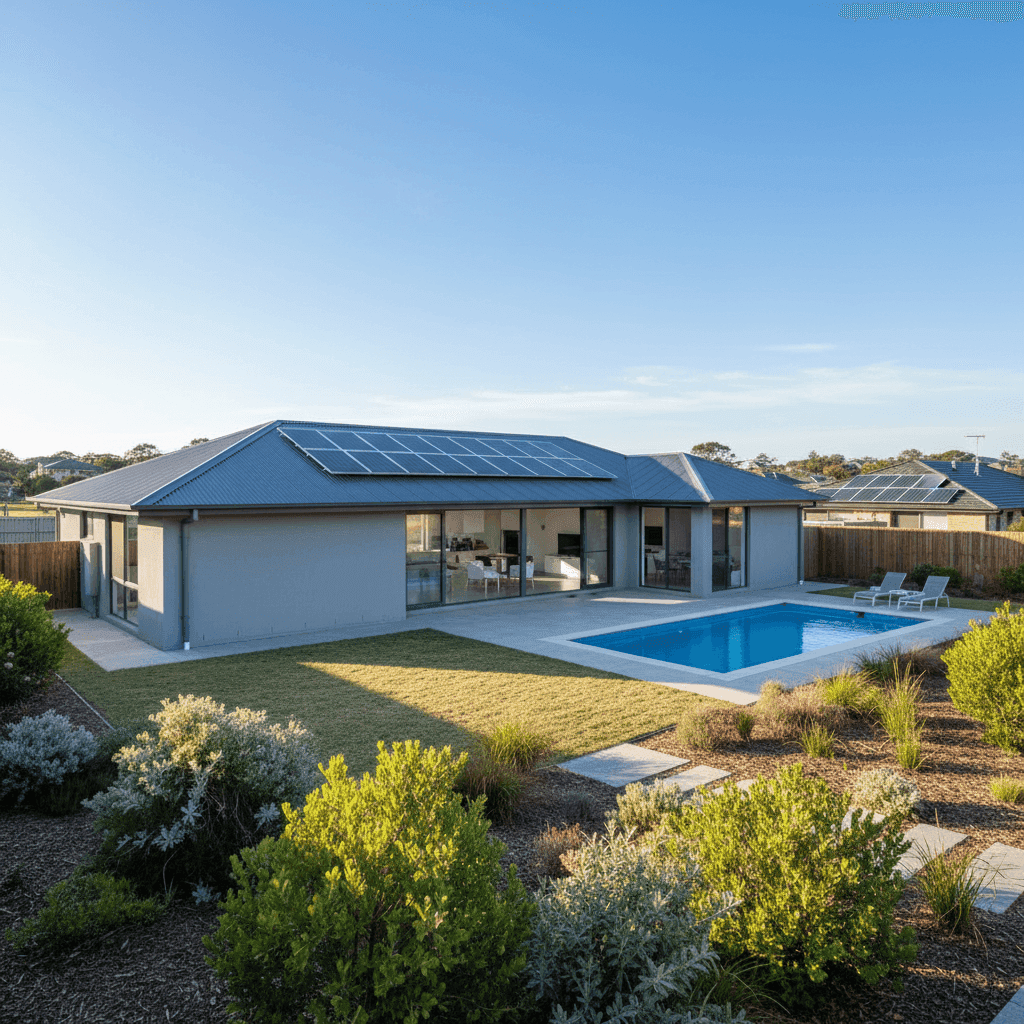

The swimming pool adds a modest amount to the premium — pools require their own structural cover and can be expensive to repair after storm or subsidence events. Similarly, the solar panel system needs to be accounted for in the building sum insured, as panels are generally considered part of the building structure. At 169 sqm, this is a comfortably sized home, and the 2006 construction year means it was built to relatively modern building codes, which is generally a positive from an insurer's perspective.

---

Tips for Homeowners in Umina Beach

1. Review your sum insured regularly Building costs have risen sharply in recent years. A sum insured of $500,000 may have been appropriate at policy inception, but with construction costs increasing across NSW, it's worth checking whether your coverage still reflects the true cost of rebuilding. Many insurers offer a rebuild cost calculator to help.

2. Shop around at renewal time The wide spread of premiums in Umina Beach — from $1,646/yr at the 25th percentile to $5,356/yr at the 75th — shows that there's significant variation in what insurers charge for similar properties. Don't assume your renewal price is the best available. Compare quotes at CoverClub to see what else is on the market.

3. Consider your excess carefully A $1,000 excess is standard, but increasing it to $2,000 or more can meaningfully reduce your annual premium. If you have the financial buffer to cover a higher out-of-pocket cost in a claim scenario, this can be a smart way to lower ongoing costs.

4. Ensure your solar panels and pool are correctly listed Both solar panels and swimming pools need to be specifically covered under your policy. Check your product disclosure statement (PDS) to confirm these are included and that the sum insured accounts for their replacement value. Some policies have specific sub-limits or exclusions for these items.

---

Compare Your Home Insurance Quote

Whether you're a long-term Umina Beach local or new to the area, it pays to make sure you're not overpaying for cover. CoverClub makes it easy to compare building insurance quotes from multiple insurers in one place — so you can see exactly how your current premium stacks up.

Get a home insurance quote for your Umina Beach property and find out if you could be paying less for the same level of protection.