If you own a free standing home in Umina Beach, NSW 2257, you've probably wondered whether you're paying a fair price for home insurance — or whether there's a better deal waiting to be found. This article breaks down a real home and contents insurance quote for a five-bedroom property in the area, comparing it against suburb, state, and national benchmarks so you can make a more informed decision.

---

Is This Quote Fair?

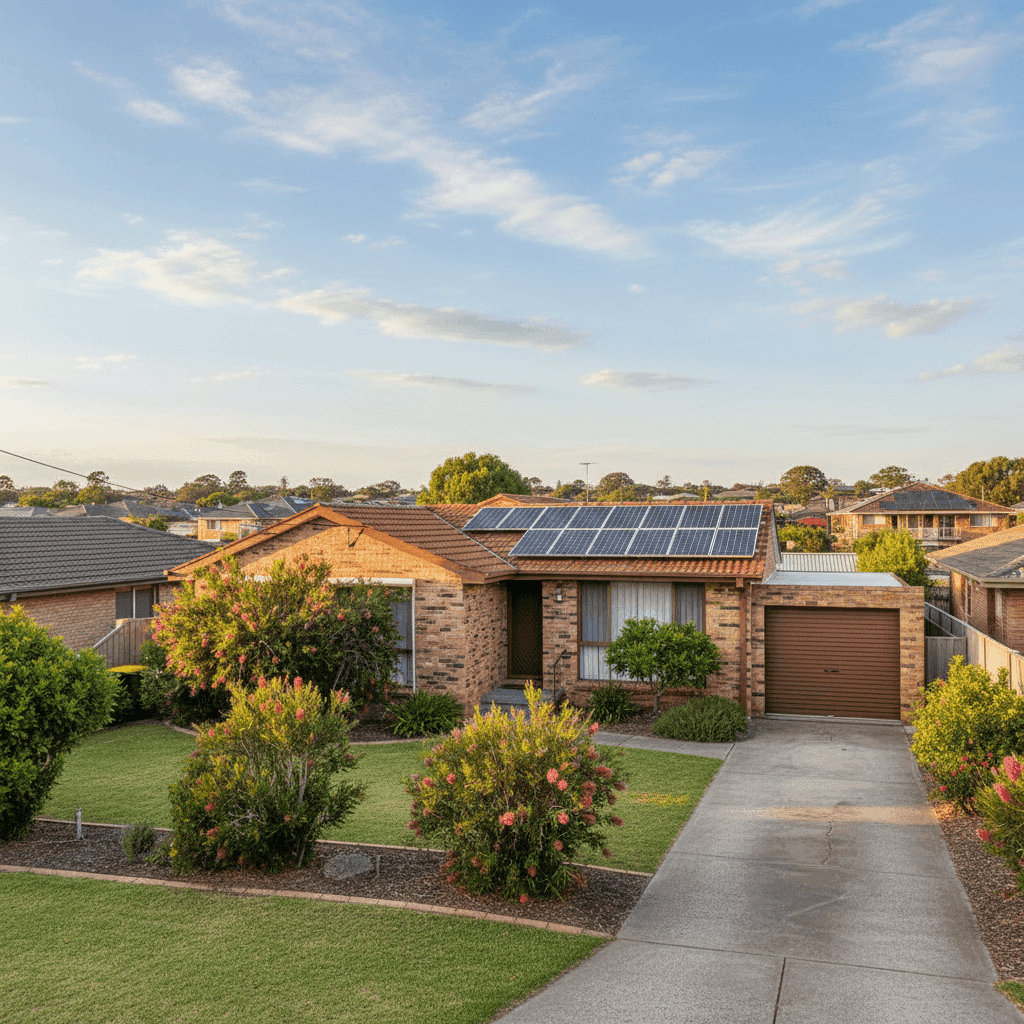

The quote in question sits at $3,476 per year (or $340 per month) for combined home and contents cover, with a building sum insured of $750,000 and contents valued at $150,000. Both the building and contents excess are set at $1,000 each.

Our price rating for this quote is FAIR — around average.

That assessment holds up when you dig into the numbers. The suburb average premium for Umina Beach is $3,353 per year, meaning this quote comes in just $123 above the local average — a difference of roughly 3.7%. That's well within the margin you'd expect given the specific characteristics of this property, including its size (305 sqm), age (built in 1975), and features like solar panels and ducted climate control.

In short: you're not being overcharged, but there may still be room to sharpen the price with the right insurer.

---

How Umina Beach Compares

Understanding where Umina Beach sits in the broader insurance landscape is useful context for any homeowner.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Umina Beach (NSW 2257) | $3,353/yr | $2,587/yr |

| NSW (State) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Central Coast LGA | $8,387/yr | — |

(Based on a sample of 24 quotes for the Umina Beach postcode. [View full suburb stats →](https://coverclub.com.au/stats/NSW/2257/umina-beach))

A few things stand out here. The NSW state average of $9,528 per year is dramatically higher than what Umina Beach homeowners typically pay — though that figure is heavily skewed by high-risk and high-value properties elsewhere in the state. The state median of $3,770 is a more representative comparison, and it actually sits above this quote, suggesting the pricing here is genuinely competitive relative to NSW as a whole.

Nationally, the average premium across Australia is $5,347 per year, with a median of $2,764. Umina Beach's median of $2,587 tracks closely to the national median, which tells us this is broadly a mid-range suburb when it comes to insurance risk and pricing.

The Central Coast LGA average of $8,387 is notably higher than the Umina Beach suburb average, which suggests that some parts of the Central Coast carry significantly elevated risk profiles — but Umina Beach itself appears to be a more affordable pocket within the region. You can explore more NSW insurance data here.

It's also worth noting the wide spread within the suburb itself: the 25th percentile sits at $1,646/yr while the 75th percentile reaches $5,356/yr. This range of over $3,700 illustrates just how much individual property characteristics and insurer pricing models can vary — even within the same postcode.

---

Property Features That Affect Your Premium

Several features of this particular home are worth examining through an insurance lens.

Brick veneer construction with a tiled roof is generally viewed favourably by insurers. Brick veneer offers solid fire resistance and structural durability, while tiled roofs are considered lower risk than metal or fibrous cement alternatives. Together, these materials can help keep premiums more competitive.

Stump foundations are common in older Australian homes, particularly those built in the 1950s–1970s. While stumps can be more susceptible to movement, subsidence, and pest damage than slab foundations, they're well understood by insurers and don't necessarily attract a significant loading — particularly in coastal areas where elevated homes are the norm.

Timber and laminate flooring is worth noting from a contents perspective. These materials can be costly to repair or replace after water damage or flooding, so it's important to ensure your contents and building sums insured adequately reflect replacement costs.

Solar panels are an increasingly common feature on Australian homes, and this property is no exception. Most standard home insurance policies cover solar panels as part of the building, but it's always worth confirming this with your insurer — particularly for systems with high-value inverters or battery storage.

Ducted climate control adds meaningful value to the building and is another item that should be factored into your sum insured. Ducted systems can be expensive to repair or replace, and underinsurance is a real risk if this isn't properly accounted for.

At 305 sqm, this is a sizeable home, and the $750,000 building sum insured needs to reflect the full cost of rebuilding — not just the market value of the property. Given construction costs in coastal NSW, this figure warrants periodic review to guard against underinsurance.

---

Tips for Homeowners in Umina Beach

1. Review your sum insured annually Construction costs have risen sharply in recent years across Australia, and coastal NSW is no exception. A sum insured that was adequate two or three years ago may no longer cover a full rebuild today. Use a building cost calculator or speak with a quantity surveyor to get an up-to-date estimate.

2. Check your solar panel coverage If you have solar panels — as this property does — confirm with your insurer exactly what's covered. Some policies include panels as part of the building sum insured automatically; others require them to be listed separately. Also check whether your policy covers damage from storms, hail, or electrical faults.

3. Consider the impact of your excess Both the building and contents excess on this quote are set at $1,000. Opting for a higher excess (say, $2,000 or $2,500) can meaningfully reduce your annual premium. If you have the financial buffer to absorb a larger out-of-pocket cost in the event of a claim, this is often a smart trade-off.

4. Compare quotes before renewing With a 25th–75th percentile range of $1,646–$5,356 in this postcode alone, there's clearly significant variation in what different insurers will charge for the same property. Don't let your policy auto-renew without checking what else is on the market — you could save hundreds of dollars a year without reducing your level of cover.

---

Compare Home Insurance Quotes in Umina Beach

Whether you're reviewing an existing policy or shopping for cover on a new property, comparing quotes is the single most effective way to ensure you're getting value. At CoverClub, we make it easy to see how your premium stacks up against real data from your suburb and beyond. Get a home insurance quote today and find out whether you're paying a fair price — or whether it's time to switch.