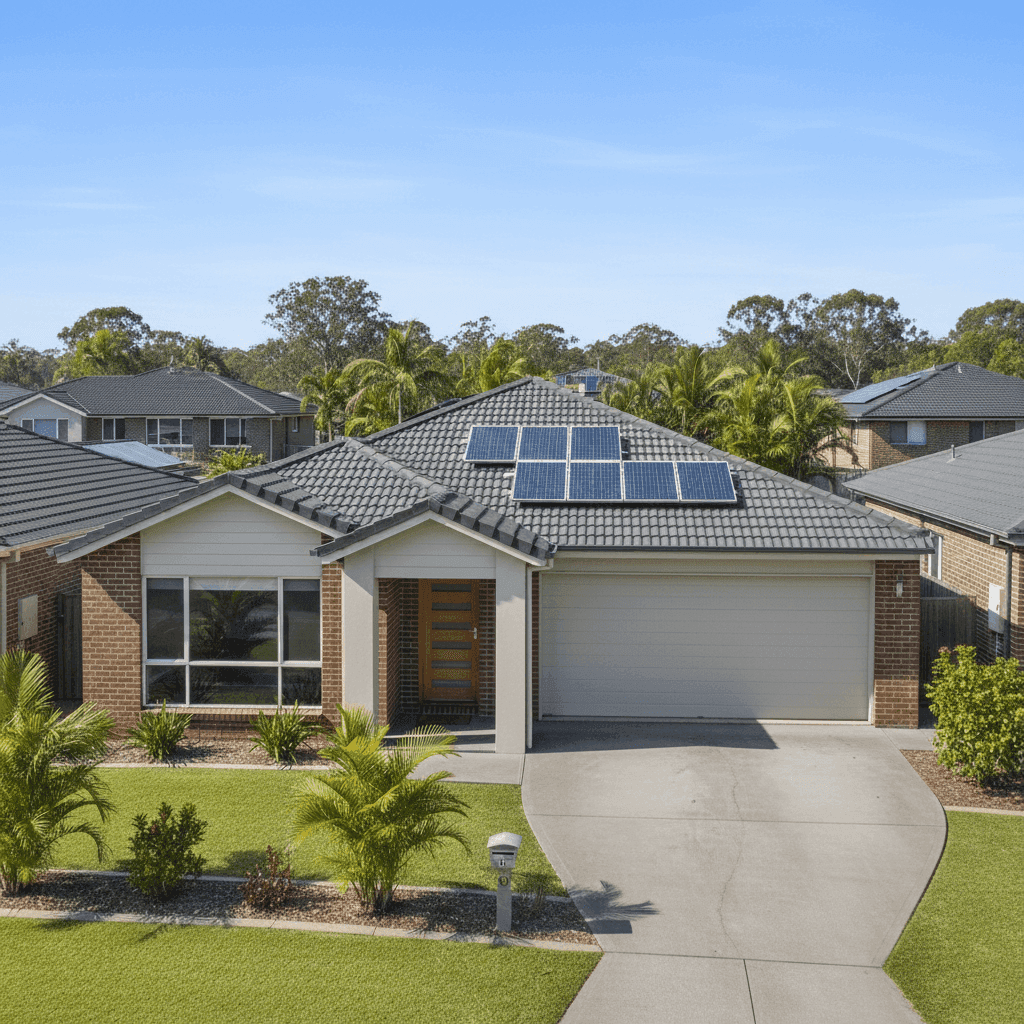

Upper Coomera is one of South East Queensland's fastest-growing suburbs, sitting in the heart of the Gold Coast's northern corridor. With its mix of modern family homes, proximity to theme parks, and strong infrastructure investment, it's no surprise that homeowners here are paying close attention to the cost of protecting their biggest asset. This article breaks down a recent home and contents insurance quote for a four-bedroom, brick veneer free standing home in Upper Coomera — and puts the numbers into context so you can judge whether you're getting a fair deal.

---

Is This Quote Fair?

The quote in question comes in at $2,253 per year (or $216 per month) for combined home and contents cover, with a building sum insured of $600,000 and contents valued at $115,000. Both the building and contents excess are set at $1,000.

Our independent price rating for this quote is Fair — Around Average.

That's a reasonable outcome for a well-built modern home. The property was constructed in 2010, which means it benefits from building codes introduced after major weather events reshaped Queensland's construction standards. Brick veneer walls and a tiled roof are both considered low-to-moderate risk materials by most insurers, and a slab foundation in a non-cyclone zone ticks the right boxes for competitive pricing.

That said, "fair" doesn't necessarily mean "the best available." It means this quote sits comfortably within the expected range for this type of property in this suburb — neither a standout bargain nor an overpriced outlier.

---

How Upper Coomera Compares

To understand what this quote really means, it helps to look at the broader picture. Based on data from 87 quotes collected for Upper Coomera (postcode 4209):

| Benchmark | Premium |

|---|---|

| Suburb 25th percentile | $1,822/yr |

| This quote | $2,253/yr |

| Suburb median | $2,606/yr |

| Suburb average | $3,117/yr |

| Suburb 75th percentile | $3,693/yr |

At $2,253, this quote sits below the suburb median of $2,606 and well below the suburb average of $3,117. That's a meaningful saving — it places this quote closer to the cheaper end of what Upper Coomera homeowners are typically paying.

The contrast with broader benchmarks is even more striking. According to Queensland state-wide insurance data, the average home insurance premium across QLD is a hefty $9,129 per year, with a median of $3,903. The Gold Coast LGA average sits at $8,161 per year — significantly higher than what this property is attracting.

At the national level, the average premium is $5,347 per year, with a national median of $2,764. This quote comes in just below the national median, which is a strong result for a property of this size and value.

Why the gap between Upper Coomera and the broader Queensland and Gold Coast averages? Much of Queensland's premium pool is dragged upward by high-risk coastal and cyclone-prone areas — think Far North Queensland, the Whitsundays, and flood-affected inland regions. Upper Coomera, sitting inland from the Gold Coast coastline and outside designated cyclone risk zones, benefits from a comparatively benign risk profile.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour when it comes to insurance pricing:

Brick veneer construction is well regarded by insurers. It offers solid structural integrity and reasonable fire resistance compared to lightweight cladding or weatherboard alternatives. Combined with a tiled roof, the home sits in a material category that typically attracts mid-range to competitive premiums.

Slab foundation is standard for Queensland homes of this era and doesn't introduce the subfloor risks associated with older stumped or timber-framed foundations.

Built in 2010, the property falls under post-2000 building codes, which incorporated improved wind and weather resistance standards — particularly relevant in South East Queensland where severe storms are a seasonal reality.

Solar panels are worth noting. While they add value to the property, they can also add a small amount of complexity to an insurance claim (particularly in storm or hail events), and some insurers factor this into their pricing. It's important to confirm with your insurer that solar panels are explicitly covered under your policy — both the panels themselves and any damage they might cause to the roof.

Ducted climate control is a higher-value fixed fixture that contributes to the building sum insured. At $600,000, the building cover is substantial but appropriate for a 244 sqm home with quality fixtures in a growing Gold Coast suburb.

No pool simplifies liability considerations, and the standard fittings quality keeps replacement cost estimates grounded — avoiding the premium uplift that can come with high-end or custom finishes.

---

Tips for Homeowners in Upper Coomera

1. Review your sum insured regularly Upper Coomera has seen strong property and construction cost growth in recent years. The cost to rebuild a 244 sqm brick veneer home has risen considerably since 2020 due to labour shortages and materials inflation. Make sure your $600,000 building sum insured reflects current rebuild costs — not what it cost to build the home in 2010.

2. Confirm solar panel coverage explicitly Don't assume your solar system is automatically covered. Ask your insurer whether the panels are included under building cover, what the claim process looks like for storm or hail damage, and whether there are any exclusions related to inverter failure or electrical faults.

3. Get multiple quotes — even when your current price seems fair A "fair" rating means this quote is competitive, but the spread in Upper Coomera is wide: from $1,822 at the 25th percentile to $3,693 at the 75th percentile. There's real money to be saved by comparing. Run a comparison at CoverClub to see what other insurers would charge for the same property.

4. Consider your excess strategically Both the building and contents excess on this policy are set at $1,000. Opting for a higher excess (say, $1,500 or $2,000) can reduce your annual premium meaningfully — and if you haven't made a claim in years, it may be a worthwhile trade-off. Just ensure the excess remains affordable in a genuine emergency.

---

Ready to Compare?

Whether you're renewing your policy or shopping around for the first time, it pays to know where your quote stands. CoverClub makes it easy to benchmark your premium against real data from your suburb, your state, and across Australia.

Get a home insurance quote and compare your options at CoverClub — it takes just a few minutes and could save you hundreds every year.