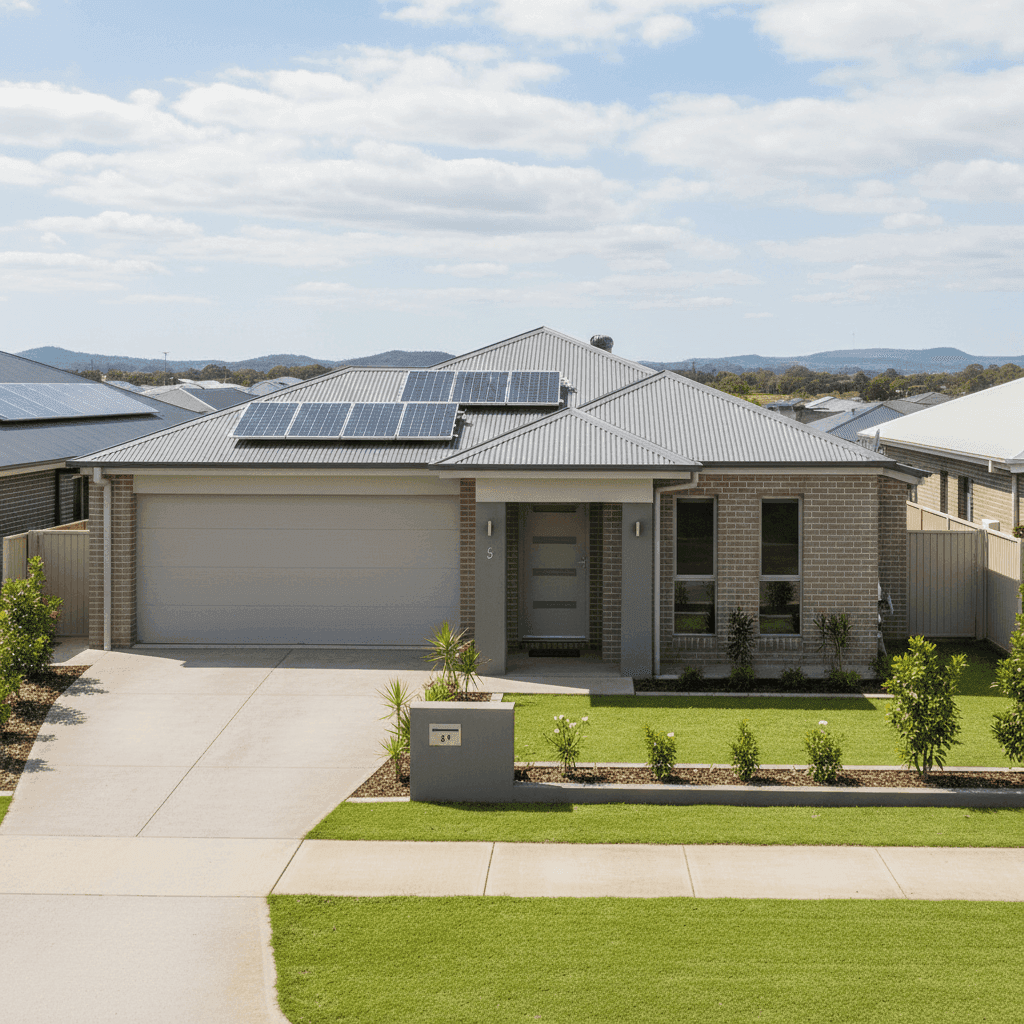

If you own a four-bedroom free standing home in Upper Coomera, QLD 4209, you're probably curious about whether you're paying a fair price for your home and contents insurance. This article breaks down a real quote for a property in this suburb — a 214 sqm brick veneer home built in 2006 — and puts the numbers in context using suburb, state, and national benchmarks. Whether you're shopping around for the first time or reviewing your renewal, understanding what drives your premium is the first step to making a smarter decision.

---

Is This Quote Fair?

The quote in question comes in at $2,765 per year (or $258/month) for combined home and contents cover, with a building sum insured of $599,000 and contents valued at $82,000. Both the building and contents excess are set at $1,000 each.

Our pricing analysis rates this quote as FAIR — Around Average. That's not a bad result. It means the premium is competitive without being suspiciously cheap, and it sits comfortably within the normal range for this type of property in this location. For homeowners who haven't compared their policy in a while, "around average" can actually be a meaningful win — plenty of people are paying well above the going rate simply due to loyalty inertia.

That said, "fair" doesn't mean you can't do better. It's worth understanding exactly where this figure lands relative to the broader market.

---

How Upper Coomera Compares

To put the $2,765 annual premium in perspective, here's how it stacks up against local Upper Coomera data, the Queensland state average, and national benchmarks:

| Benchmark | Premium |

|---|---|

| This quote | $2,765/yr |

| Suburb average (Upper Coomera) | $3,117/yr |

| Suburb median (Upper Coomera) | $2,606/yr |

| Suburb 25th percentile | $1,822/yr |

| Suburb 75th percentile | $3,693/yr |

| Gold Coast LGA average | $8,161/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

Based on 87 quotes collected for the Upper Coomera suburb.

A few things stand out here. First, this quote is below the suburb average of $3,117 and very close to the national median of $2,764 — almost exactly in line. Second, the Gold Coast LGA average of $8,161 and the Queensland state average of $9,129 look eye-wateringly high by comparison. This is largely because Queensland's insurance market is heavily skewed by high-risk coastal and cyclone-prone areas, which pull the averages upward significantly. Upper Coomera, sitting inland from the coast, benefits from a more moderate risk profile.

The suburb's 25th percentile of $1,822 shows that cheaper quotes do exist — but those may reflect lower sum insured amounts, fewer features covered, or higher excesses. It's important to compare policies on equal terms, not just price.

---

Property Features That Affect Your Premium

Every element of a home's construction, size, and features plays a role in how insurers calculate risk. Here's how the key characteristics of this property are likely influencing the premium:

Brick Veneer Walls & Colorbond Roof Brick veneer is generally viewed favourably by insurers — it's durable, fire-resistant, and widely used in Australian suburban construction. Paired with a steel Colorbond roof, this home has a solid combination that typically attracts reasonable premiums. Colorbond is low-maintenance and performs well in storms, which is a plus in South East Queensland's storm-prone climate.

Slab Foundation & Tiled Flooring A concrete slab foundation is the standard for homes of this era and is considered low-risk by most insurers. Tiled flooring throughout is also a practical choice in Queensland's climate — and from an insurance perspective, tiles are more resistant to water damage than carpet or timber, which can slightly reduce the cost of a contents or building claim.

Built in 2006 At roughly 18–20 years old, this home is relatively modern. Homes built after 1990 generally meet stricter building codes and are constructed with better materials, which can translate to lower rebuild costs and fewer structural risks. This works in the homeowner's favour when it comes to premium pricing.

Solar Panels Solar panels are listed as a feature of this property. Insurers treat solar installations differently — some include them automatically under building cover, while others require them to be specifically noted. It's worth confirming with your insurer that your panels (and any battery storage) are fully covered under the building sum insured of $599,000.

Ducted Climate Control Ducted air conditioning is a significant fixed asset and forms part of the building's value. Its inclusion is one reason the building sum insured needs to be set accurately — underinsuring a home with premium fixtures can leave you short at claim time.

No Pool, No Cyclone Risk Zone The absence of a pool removes a common source of liability and maintenance-related claims. And while Upper Coomera sits within Queensland — a state with significant cyclone risk in its northern regions — this suburb is not classified as a cyclone risk area, which is a meaningful factor in keeping premiums more manageable.

---

Tips for Homeowners in Upper Coomera

1. Check that your solar panels are explicitly covered Don't assume your solar system is automatically included in your building cover. Ask your insurer directly whether panels, inverters, and any battery storage are covered — and for how much. Given the cost of solar installations, this is one area where a gap in cover can be costly.

2. Review your sum insured annually Building costs in South East Queensland have risen considerably over recent years. A sum insured of $599,000 may have been appropriate when the policy was first taken out, but it's worth reassessing whether it still reflects the true cost of rebuilding your home — including the ducted air conditioning, solar system, and any renovations you've made.

3. Understand your excess before you claim Both the building and contents excess on this policy are set at $1,000. A higher excess generally reduces your premium, but make sure you're comfortable covering that amount out of pocket if you need to make a claim. Some insurers allow you to adjust your excess to find the right balance between upfront savings and claim-time costs.

4. Compare at renewal, not just once The insurance market changes every year. Even if this quote is fair today, your insurer may apply a significant increase at renewal. Set a reminder to compare quotes before your policy renews — it takes only a few minutes and can save you hundreds of dollars.

---

Ready to Find a Better Deal?

Whether you're happy with your current cover or looking to switch, it pays to see what else is out there. Compare home and contents insurance quotes at CoverClub and find out if you can get the same level of protection for less. With data from dozens of quotes across Upper Coomera and beyond, CoverClub makes it easy to see exactly where you stand.