Home insurance in Queensland can be a complex puzzle — premiums vary dramatically depending on where you live, what your home is made of, and what extras you need to cover. This article takes a close look at a real home and contents insurance quote for a three-bedroom, two-bathroom free standing home in Urangan, QLD 4655, comparing it against suburb, state, and national benchmarks to help you understand what's driving the cost — and whether there's room to save.

---

Is This Quote Fair?

The annual premium for this property came in at $2,151 per year (or $210/month), covering both building and contents. The building is insured for $676,000 with a $2,000 excess, while contents are covered for $50,000 with a $600 excess.

Our price rating for this quote is FAIR — Around Average.

What does that mean in practice? It means the premium isn't a bargain, but it's not overpriced either. Sitting comfortably within the middle range of what Urangan homeowners are paying, this quote reflects a reasonable market rate for the property type and cover level. That said, "average" doesn't mean you can't do better — and understanding the numbers behind the rating is the first step toward making a smarter decision.

---

How Urangan Compares

To put this quote in context, here's how it stacks up against Urangan suburb averages, Queensland state figures, and national benchmarks — based on data from real quotes collected by CoverClub.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Urangan (4655) | $3,284/yr | $2,925/yr |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out here. At $2,151, this quote sits well below the Urangan suburb average of $3,284 and even below the suburb's 25th percentile of $1,788 is close — meaning roughly three-quarters of comparable quotes in the area cost more. It also comes in significantly under the Queensland state average of $4,547, which reflects just how expensive home insurance has become across much of regional and coastal QLD.

Compared to the national average of $2,965, this quote is about $814 cheaper per year — a meaningful saving. Queensland homeowners typically pay a steep premium over the national average due to the state's exposure to severe weather events, including flooding, storms, and cyclones. The fact that this particular quote lands below both the suburb and state medians suggests the insurer has assessed the specific property risk favourably.

For further context, the suburb's interquartile range runs from $1,788 (25th percentile) to $3,932 (75th percentile), based on a sample of 79 quotes — a reasonably solid dataset. This spread tells us there's significant variability in what Urangan homeowners pay, and shopping around can make a real difference.

---

Property Features That Affect Your Premium

Several characteristics of this home are worth examining through an insurance lens.

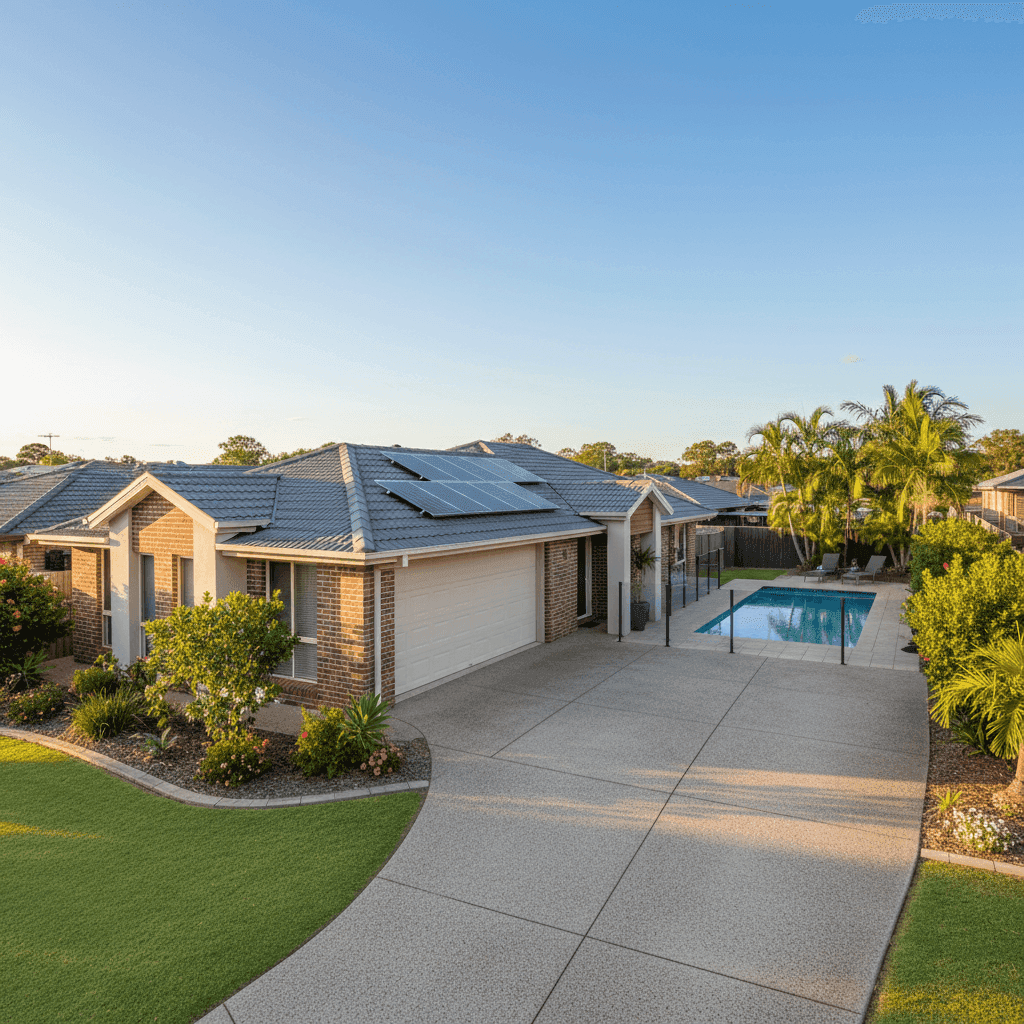

Brick Veneer Walls & Tiled Roof Brick veneer construction paired with a tiled roof is generally viewed favourably by insurers. These materials offer solid fire resistance and durability compared to timber weatherboard or Colorbond alternatives. Homes built with these materials typically attract more competitive premiums, which may be contributing to the below-average quote here.

Slab Foundation A concrete slab foundation is common in Queensland builds from the 1990s and is generally considered a stable, low-risk foundation type. It's less susceptible to subsidence than pier-and-beam foundations and doesn't carry the same moisture-related risks.

Construction Year: 1996 At nearly 30 years old, the home is mature but not aged. Properties built in the mid-1990s generally comply with reasonable building standards, though they predate some of the more stringent cyclone-proofing codes introduced after Cyclone Larry (2006) and Cyclone Yasi (2011). However, with this property assessed as not in a cyclone risk area, that's less of a concern here.

Swimming Pool A pool adds liability exposure and can nudge premiums upward. Insurers factor in the cost of potential damage to pool infrastructure — pumps, fencing, and the pool shell itself — as well as public liability considerations if a third party is injured on the property.

Solar Panels Solar panels are an increasingly common feature in Queensland homes, but they do add to the replacement cost calculation. If panels are damaged by a storm or hail, the repair or replacement bill can be substantial. It's worth confirming with your insurer that your solar system is explicitly included in your building sum insured.

Ducted Climate Control Ducted air conditioning systems are expensive to repair or replace. This feature adds to the overall replacement value of the home and is a legitimate driver of a higher sum insured — in this case, $676,000 for a 214 sqm home.

Standard Fittings Standard-quality fittings mean the home doesn't carry the premium replacement costs associated with high-end finishes. This keeps the rebuild estimate more predictable and can work in the homeowner's favour when it comes to pricing.

---

Tips for Homeowners in Urangan

1. Review your sum insured annually With building costs rising across Australia, it's easy for your sum insured to fall behind the actual cost of rebuilding your home. At $676,000 for a 214 sqm brick veneer home in Urangan, the current figure equates to roughly $3,159 per square metre — broadly in line with current construction costs in regional Queensland, but worth verifying with an independent building cost calculator each year.

2. Confirm solar panels and pool equipment are covered Don't assume these are automatically included in your building cover. Ask your insurer directly whether solar panels, inverters, pool pumps, and associated equipment are covered — and for what events. Some policies exclude storm damage to solar panels or have sub-limits for pool-related claims.

3. Shop around at renewal time Even with a FAIR-rated quote, there may be better value available. The wide spread in Urangan premiums (from $1,788 to $3,932) shows that different insurers assess the same suburb very differently. Comparing at least three quotes before renewing is a straightforward way to avoid overpaying.

4. Consider your excess settings carefully This policy carries a $2,000 building excess and a $600 contents excess. A higher excess generally lowers your premium, but make sure you can comfortably cover that amount out of pocket if you need to make a claim. If cashflow is a concern, a lower excess with a slightly higher premium might be the smarter trade-off.

---

Compare Your Home Insurance with CoverClub

Whether you're renewing your existing policy or taking out cover for the first time, it pays to compare. CoverClub makes it easy to see what other homeowners in Urangan are paying and to get quotes tailored to your property. Start comparing home insurance quotes today — it only takes a few minutes and could save you hundreds of dollars a year.