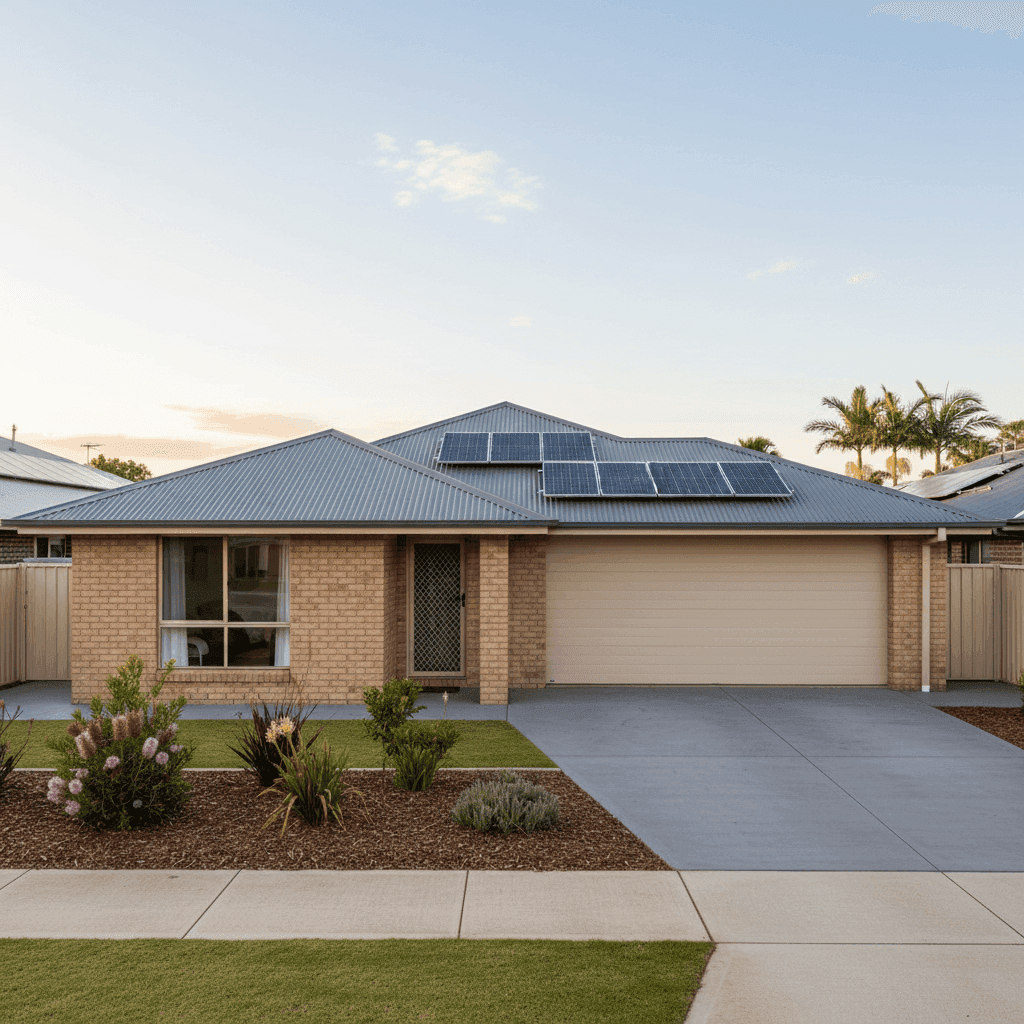

If you own a free standing home in Urangan, QLD 4655, you'll know that finding the right home insurance at a fair price takes a bit of legwork. Urangan sits on the shores of Hervey Bay — a relaxed coastal community that's grown steadily in popularity, but one where insurance premiums can vary enormously depending on the property and insurer. This article breaks down a real home and contents insurance quote for a 3-bedroom, 2-bathroom brick veneer home in the suburb, and puts the numbers into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The short answer: yes — this is an excellent result.

The quote in question comes in at $1,722 per year (or $169 per month) for combined home and contents cover, with a building sum insured of $397,000 and $30,000 in contents cover. Both the building and contents excess sit at $1,000, which is a standard and reasonable level.

Our pricing model rates this quote as CHEAP — below average for the area. To put that in plain terms: based on 137 quotes collected for Urangan, the suburb average premium is $3,727 per year, and the median sits at $2,798 per year. This quote comes in at less than half the suburb average — a genuinely strong outcome for the homeowner.

Even against the 25th percentile (meaning only 25% of Urangan quotes are cheaper), the figure is $2,034 per year. At $1,722, this quote beats even the cheapest quarter of the market — a clear sign that the insurer has priced this property very competitively.

---

How Urangan Compares to QLD and Australia

To fully appreciate this result, it helps to zoom out and look at the broader picture.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Urangan (4655) | $3,727/yr | $2,798/yr |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

The Queensland state average of $9,129 per year is strikingly high — a reflection of the significant weather and natural disaster risks that affect much of the state, particularly in cyclone-prone and flood-affected regions. The national average of $5,347 per year also sits well above what this homeowner is paying.

Interestingly, Urangan's median premium of $2,798 is actually slightly above the national median of $2,764 — suggesting the suburb carries a modest risk premium relative to the broader Australian market, even if it's far more affordable than the Queensland average. This makes sense given Hervey Bay's coastal location, though Urangan itself is not classified as a cyclone risk area, which is a significant factor in keeping premiums manageable.

At $1,722 per year, this quote sits 54% below the Urangan suburb average and 81% below the Queensland state average — an outstanding result by any measure.

---

Property Features That Affect Your Premium

Several characteristics of this particular property likely contribute to its competitive premium. Here's how each one plays a role:

🧱 Brick Veneer Walls

Brick veneer is one of the most common and well-regarded external wall materials in Australia. Insurers generally view it favourably — it's durable, fire-resistant, and less susceptible to storm damage than timber weatherboard. This construction type typically attracts lower premiums compared to less robust materials.

🏠 Steel / Colorbond Roof

Colorbond steel roofing is highly regarded by insurers for its resilience. It handles hail, wind, and rain exceptionally well, and doesn't degrade the way older roofing materials (like terracotta tiles) can. A well-maintained Colorbond roof is a genuine asset when it comes to insurance pricing.

🏗️ Slab Foundation

A concrete slab foundation is considered low-risk by most insurers. It's stable, resistant to termite ingress (compared to raised timber floors), and less prone to movement in varying soil conditions. Combined with tile flooring throughout, this property presents a solid and low-maintenance risk profile.

☀️ Solar Panels

The property has solar panels installed. It's worth noting that solar systems are not always automatically covered under a standard home insurance policy — some insurers include them as part of the building sum insured, while others treat them as a separate item. Homeowners should confirm with their insurer exactly how solar panels are covered, and ensure the building sum insured reflects their replacement cost.

❄️ Ducted Climate Control

Ducted air conditioning systems are a fixed building improvement and are typically covered under the building sum insured. Their presence doesn't usually increase premiums significantly, but homeowners should ensure the $397,000 building sum insured accounts for the cost of replacing this system if damaged.

📅 1988 Construction

At around 37 years old, this home sits in a middle ground — old enough that some components (wiring, plumbing, roofing) may be approaching the end of their service life, but not so old as to attract the surcharges sometimes applied to heritage or pre-1970s properties. Regular maintenance is key to keeping premiums stable as the home ages.

---

Tips for Homeowners in Urangan

Whether you're reviewing your existing policy or shopping around for the first time, here are four practical steps to help you get the most from your home insurance in Urangan.

1. Double-check your building sum insured The cost of rebuilding a home is not the same as its market value — and underinsurance is a serious risk. Use a building cost calculator to verify that $397,000 is sufficient to cover a full rebuild of your 139 sqm home in today's market, factoring in labour, materials, and professional fees.

2. Confirm your solar panel coverage Solar panels represent a meaningful investment. Contact your insurer to clarify whether your panels are included in the building sum insured, and whether accidental damage or inverter failure is covered. If not, ask about adding them explicitly.

3. Review your contents cover annually $30,000 in contents cover is a relatively modest figure. If you've made significant purchases — furniture, appliances, electronics — since your policy was last updated, it's worth doing a quick audit to ensure you're not underinsured on the contents side.

4. Compare quotes at renewal Even a great price today can be beaten at renewal. Insurers regularly adjust their pricing models, and loyalty doesn't always pay. Use a comparison tool at renewal time to make sure you're still getting a competitive rate — especially as Urangan premiums can vary significantly between providers.

---

Ready to Compare Your Own Quote?

Whether you're a long-time Urangan resident or new to the area, it pays to know what the market looks like before you commit to a policy. CoverClub makes it easy to compare home and contents insurance quotes side by side, so you can see exactly how your premium stacks up.

Get a quote at CoverClub today and find out if you're paying a fair price — or if there's a better deal waiting for you.