Victoria Point is a leafy bayside suburb on the Redland Peninsula, southeast of Brisbane — a popular spot for families drawn to its waterfront lifestyle, quiet streets, and relative affordability compared to inner-city Queensland. For homeowners here, understanding what a fair home insurance premium looks like can be the difference between leaving money on the table and getting genuinely good value.

This article breaks down a real home and contents insurance quote for a 3-bedroom, 2-bathroom free-standing home in Victoria Point (postcode 4165), benchmarking it against suburb, state, and national data to help you understand where it sits — and what's driving the price.

---

Is This Quote Fair?

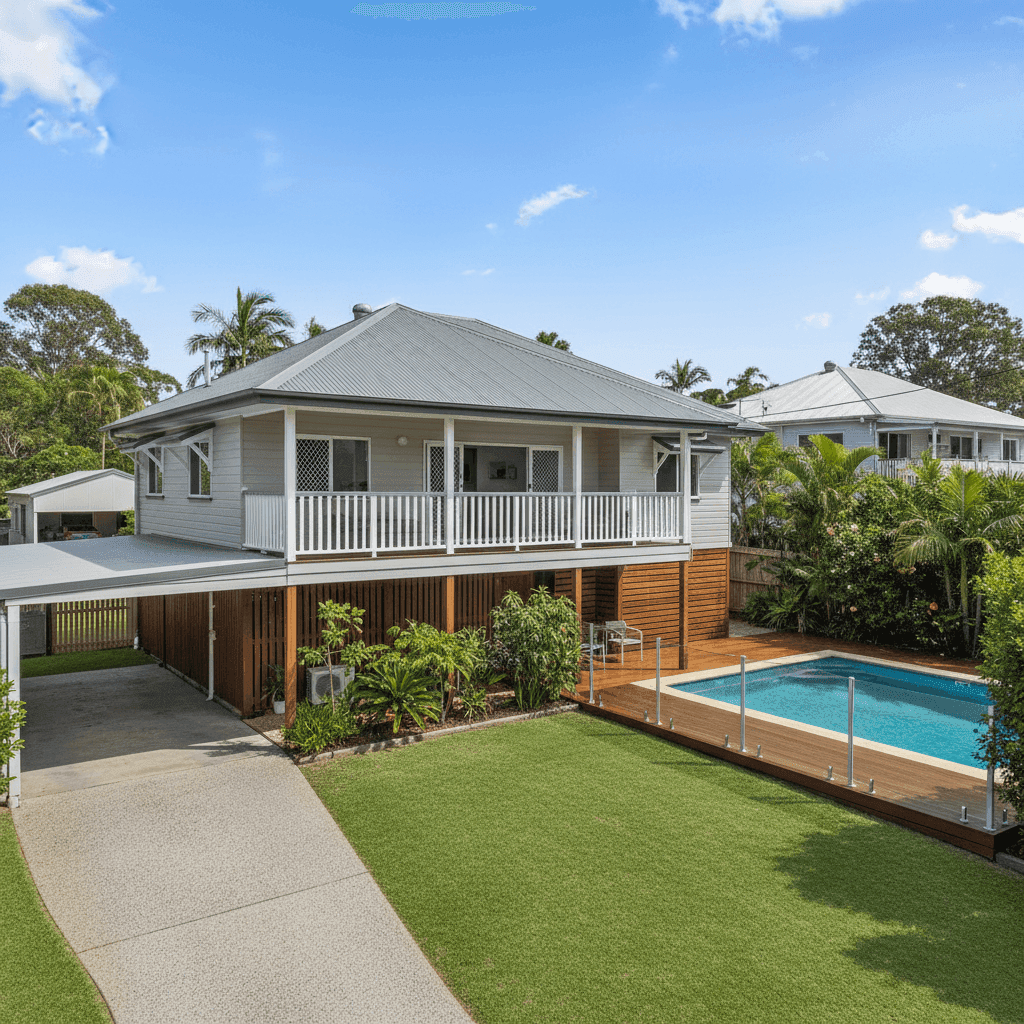

The annual premium for this property came in at $1,153 per year (or around $110 per month), covering both building (sum insured: $450,000) and contents ($85,000). Our rating? Cheap — well below average.

To put that in perspective: the average home and contents premium across Victoria Point is $3,494 per year, and the median sits at $3,043. This quote lands below even the 25th percentile for the suburb, which is $1,659 — meaning it's cheaper than at least 75% of quotes we've seen in the area. That's a significant saving, potentially over $2,300 per year compared to what many local homeowners are paying.

For a property built in 2022 with a solid construction profile and a pool on site, this represents genuinely strong value. Of course, the excess structure matters too — the building excess is $2,000, which is on the higher side and does help bring the premium down. The contents excess of $600 is more moderate. It's worth weighing whether the lower ongoing premium justifies accepting a larger out-of-pocket cost if you ever need to make a building claim.

---

How Victoria Point Compares

Victoria Point sits in an interesting position when you look at the broader insurance landscape. Check out the Victoria Point suburb insurance stats for the full picture, but here's a quick snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Victoria Point (4165) | $3,494/yr | $3,043/yr |

| Queensland (state) | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

Victoria Point premiums are notably lower than the Queensland state average — by around $1,053 per year on a median basis — but sit above the national median. This is consistent with broader trends across southeast Queensland, where proximity to flood-prone areas, storm risk, and the general cost of rebuilding in Queensland push premiums higher than in many southern states.

You can explore Queensland-wide insurance data and national home insurance benchmarks to see how your own situation compares across different regions.

Within the Redland LGA, the average premium sits at $3,312 per year — slightly below the suburb average for Victoria Point, suggesting some variation across the broader council area depending on exact location, flood mapping, and proximity to the bay.

---

Property Features That Affect Your Premium

Several characteristics of this particular property work in favour of a lower premium:

Modern construction (2022 build) Newer homes are generally cheaper to insure. A 2022 build means the property complies with current building codes, uses modern materials, and is far less likely to have ageing infrastructure issues like deteriorating wiring or old plumbing — all factors that increase claim risk.

Hardiplank/Hardiflex cladding Fibre cement cladding like Hardiplank is a popular choice in Queensland for good reason — it's durable, fire-resistant, and holds up well in humid coastal climates. Insurers tend to view it more favourably than timber weatherboards, which carry higher fire and rot risk.

Steel/Colorbond roof A Colorbond steel roof is one of the most insurer-friendly roofing materials available in Australia. It's lightweight, highly resistant to wind uplift, non-combustible, and requires minimal maintenance. In a region that experiences significant storm activity, this is a meaningful risk reducer.

Stump foundation Homes on stumps (also known as timber or concrete pier foundations) are common in Queensland. They allow airflow under the floor — important in a humid climate — and can be easier to inspect and repair than slab-on-ground foundations. However, they can be more susceptible to certain types of storm and flood damage, so insurers do factor this in.

Swimming pool The property includes a pool, which adds to the contents/liability risk profile and can nudge premiums upward. Pool-related liability (particularly in homes with children or visitors) is a genuine consideration, and the cost to repair or replace pool equipment can be significant.

Ducted climate control Ducted air conditioning systems are a notable contents item — they're expensive to replace and can be damaged in storm events. Their inclusion in the sum insured is important to get right.

No cyclone risk zone Victoria Point falls outside designated cyclone risk areas, which is a meaningful premium advantage compared to properties further north in Queensland. Cyclone loading requirements significantly increase both construction costs and insurance premiums.

---

Tips for Homeowners in Victoria Point

1. Review your building sum insured regularly With a 2022 build and 139 sqm of floor space, the $450,000 sum insured may be appropriate today — but construction costs in Queensland have risen sharply in recent years. Underinsurance is a real risk: if rebuild costs exceed your sum insured after a major event, you'll bear the difference. Consider using an independent building cost estimator annually.

2. Check your flood mapping Parts of Victoria Point and the broader Redland area have varying flood classifications. Even if your specific property isn't in a high-risk zone, it's worth confirming your policy's flood cover provisions and whether your insurer's definition of "flood" aligns with your actual risk.

3. Don't over-optimise for a lower premium by inflating your excess This quote carries a $2,000 building excess. While a higher excess does reduce your premium, make sure you could comfortably cover that amount out of pocket in the event of a claim — otherwise, you may find yourself underprotected when it matters most.

4. Compare quotes at renewal time The home insurance market in Queensland is competitive, and premiums can vary enormously between providers for the same property. The spread in Victoria Point — from the 25th percentile at $1,659 to the 75th at $5,860 — shows just how wide that range can be. Shopping around at renewal could save you thousands.

---

Ready to See What You Could Pay?

Whether you're a new homeowner in Victoria Point or simply overdue for a comparison, CoverClub makes it easy to benchmark your premium against real data from your suburb, state, and across Australia. Get a home insurance quote today and find out if you're paying a fair price — or if there's a better deal waiting for you.