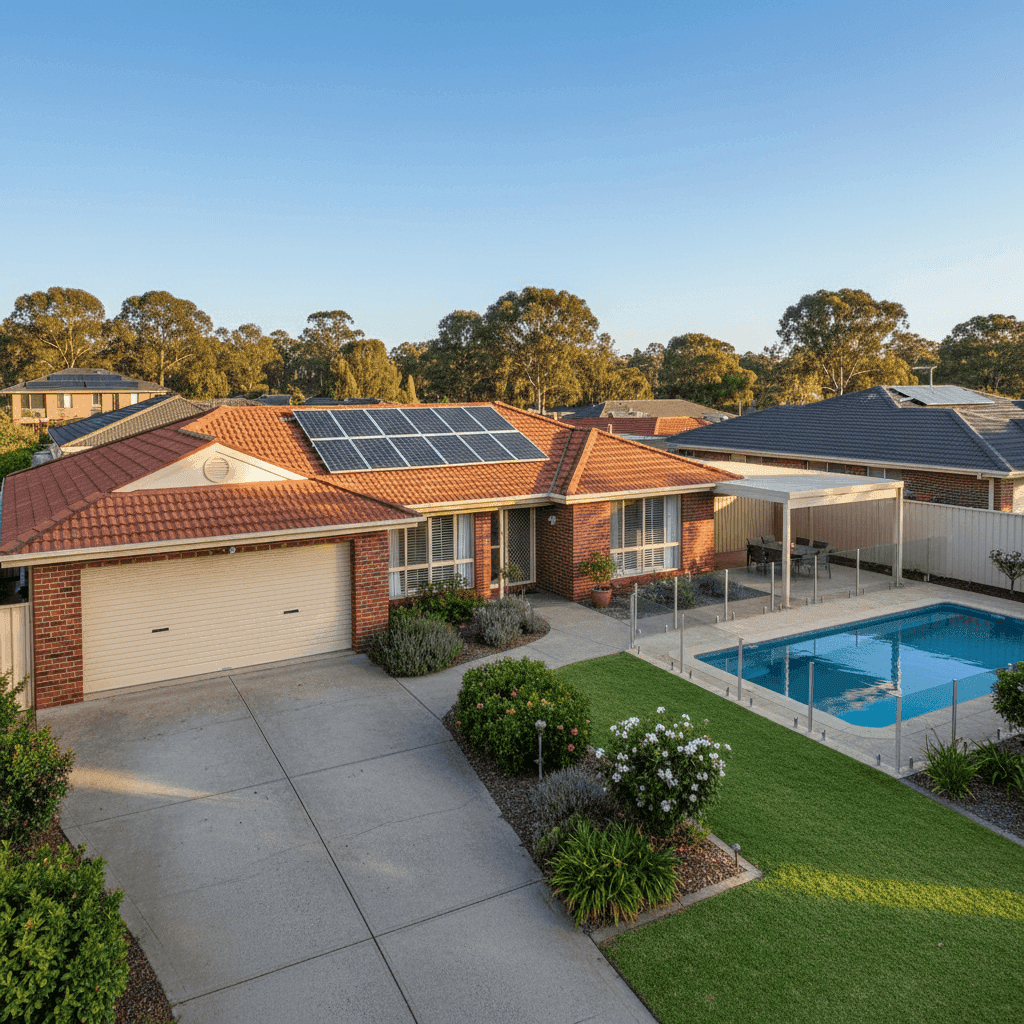

Home insurance premiums can vary enormously depending on where you live, what your home is made of, and what extras you have on the property. In this article, we take a close look at a real home and contents insurance quote for a three-bedroom, free-standing home in Vineyard, NSW 2765 — a semi-rural suburb sitting on the north-western fringe of Greater Sydney, within the City of Hawkesbury. With a growing population and a mix of established homes and newer estates, Vineyard is an increasingly popular spot for families — and understanding the true cost of protecting your home here is more important than ever.

---

Is This Quote Fair?

The annual premium on this quote comes in at $2,651 per year (or roughly $247 per month), covering a building sum insured of $488,000 and contents valued at $101,000, each with a $1,000 excess.

Our pricing analysis rates this quote as FAIR — Around Average, and the data backs that up. The suburb average premium for Vineyard sits at $2,868 per year, while the median is $2,803. This quote lands comfortably below both figures, placing it in the lower half of the local pricing range. The suburb's 25th percentile is $2,567 and the 75th percentile is $3,221, meaning this quote falls right in the middle of what most Vineyard homeowners are paying — not a bargain, but certainly not overpriced.

For a property with a pool, solar panels, and ducted climate control — all of which can push premiums upward — landing near the suburb average is a reasonably solid outcome. There may still be room to sharpen the price by comparing across more insurers, but this quote is unlikely to raise any red flags.

---

How Vineyard Compares

To put this quote in proper context, it helps to zoom out and look at the broader pricing landscape.

| Benchmark | Premium |

|---|---|

| This Quote | $2,651/yr |

| Vineyard Suburb Average | $2,868/yr |

| Vineyard Suburb Median | $2,803/yr |

| LGA (Penrith) Average | $2,220/yr |

| NSW Average | $9,528/yr |

| NSW Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. The NSW average premium of $9,528 looks startling at first glance, but this figure is heavily skewed by high-risk and high-value properties — particularly in flood-prone, bushfire-affected, and coastal areas across the state. The NSW median of $3,770 is a more representative benchmark, and this quote comes in well below it.

Compared to the national median of $2,764, this quote is only marginally higher — a sign that Vineyard is broadly in line with typical Australian home insurance costs, rather than being an outlier in either direction.

It's also worth noting that the LGA average for Penrith ($2,220) is notably lower than Vineyard's suburb average. This may reflect differences in property types, risk profiles, and sum insured levels across the broader LGA. Vineyard's semi-rural character, larger blocks, and proximity to bushland and waterways can all contribute to slightly elevated premiums compared to more urbanised parts of the region.

Note: Suburb data is based on a sample of 19 quotes, so treat these figures as a useful guide rather than a definitive benchmark.

---

Property Features That Affect Your Premium

Several characteristics of this particular property are worth examining in terms of their impact on the insurance premium.

Brick Veneer Walls & Tiled Roof Brick veneer construction with a tiled roof is one of the more insurer-friendly combinations in Australia. Brick veneer offers good fire resistance and structural durability, while tiles are considered lower risk than materials like Colorbond or timber shingles. This combination typically attracts more competitive premiums compared to, say, a weatherboard home with a metal roof.

Slab Foundation A concrete slab foundation is standard for many homes of this era and is generally viewed favourably by insurers. It reduces the risk of subsidence and pest-related structural damage compared to elevated timber stumps or older pier-and-beam foundations.

Timber & Laminate Flooring The flooring type is primarily relevant for contents insurance and reinstatement costs. Timber and laminate floors are more expensive to replace than carpet, which can influence the overall building sum insured and, by extension, the premium.

Swimming Pool Pools add value to a property but also add complexity to an insurance policy. They increase the replacement cost of the home and can introduce liability considerations. Insurers factor this into their pricing, so it's worth confirming your policy explicitly covers pool-related structures and any associated liability.

Solar Panels Solar panels are increasingly common on Australian rooftops, but they're not always covered as a default under standard building policies. At 139 sqm, this home's roof would accommodate a modest system — but homeowners should verify whether their solar panels are included under the building sum insured and whether storm or hail damage is covered.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset and should be factored into your building sum insured. These systems can cost tens of thousands of dollars to replace, and underinsuring them is a common oversight.

No Cyclone Risk Vineyard falls outside designated cyclone risk zones, which removes one of the more significant premium loading factors that affect properties in northern Queensland and parts of Western Australia. This is a meaningful advantage for local homeowners.

---

Tips for Homeowners in Vineyard

1. Check your building sum insured reflects current costs Construction costs have risen sharply across NSW in recent years. A home built in 1985 may have been underinsured for years without the owner realising. Use an independent building cost calculator or speak with a quantity surveyor to confirm your $488,000 sum insured is still adequate for full reinstatement — including demolition, debris removal, and compliance with current building codes.

2. Confirm solar panels and pool equipment are covered Ask your insurer specifically whether solar panels are covered under the building section and whether pool pumps, filtration systems, and fencing are included. These items are sometimes excluded or subject to sub-limits that many homeowners don't discover until they make a claim.

3. Compare at least three quotes before renewing Even a "fair" quote can be beaten. With 19 quotes sampled in the Vineyard area, there's enough market activity to suggest meaningful price variation between insurers. A quick comparison at CoverClub could save you hundreds of dollars annually without reducing your cover.

4. Consider bushfire and flood risk in your policy review While Vineyard is not in a cyclone zone, parts of the Hawkesbury region are subject to bushfire and flood risk. Review your policy's specific inclusions and exclusions for these events — particularly if your property is near bushland corridors or low-lying areas close to South Creek or the Hawkesbury River floodplain.

---

Ready to Find a Better Deal?

Whether you're renewing your existing policy or shopping around for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. At CoverClub, we make it easy to see what multiple insurers would charge for your specific property — so you can make a confident, informed decision.