If you own a free standing home in Vineyard, NSW 2765, you're probably wondering whether the home insurance premium you've been quoted is actually reasonable — or whether you're leaving money on the table. This article breaks down a real quote for a 3-bedroom, 2-bathroom property in Vineyard, compares it against local, state, and national benchmarks, and highlights the property features most likely to be influencing the price.

---

Is This Quote Fair?

The quote in question comes in at $2,597 per year (or $237/month) for combined home and contents cover, with a building sum insured of $449,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our pricing engine has rated this quote as FAIR — Around Average, and the data backs that up. Based on 19 quotes collected for Vineyard (postcode 2765), the suburb average sits at $2,868/year and the median at $2,803/year. At $2,597, this quote lands just below both of those figures, placing it comfortably in the lower half of the local market — specifically between the 25th percentile ($2,567) and the median ($2,803).

In plain terms: you're not getting a bargain-bin deal, but you're also not being overcharged. The premium is slightly better than what most Vineyard homeowners are paying, which is a reasonable outcome for a property with the characteristics described.

---

How Vineyard Compares

Context matters enormously when evaluating insurance pricing. Here's how Vineyard stacks up against broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Vineyard (2765) | $2,868/yr | $2,803/yr |

| LGA (Penrith) | $2,220/yr | — |

| NSW State | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The NSW state average of $9,528 looks alarming at first glance, but that figure is heavily skewed by high-value properties and extreme-risk areas across the state — the median of $3,770 is a far more representative number for typical NSW homeowners. Even so, Vineyard's median of $2,803 sits well below the NSW median, suggesting the suburb carries a relatively moderate risk profile compared to many parts of the state.

Interestingly, Vineyard's suburb average is notably higher than the broader Penrith LGA average of $2,220/year. This could reflect a mix of property ages, construction types, or localised risk factors in the 2765 postcode that push premiums up relative to neighbouring suburbs.

When compared to national figures, Vineyard sits right around the national median of $2,764 — meaning homeowners here are paying roughly what you'd expect for a typical Australian home. That's a reassuring benchmark.

---

Property Features That Affect Your Premium

Insurance premiums aren't calculated in a vacuum — every detail about your home feeds into the risk assessment. Here's how the key features of this property are likely influencing the quote:

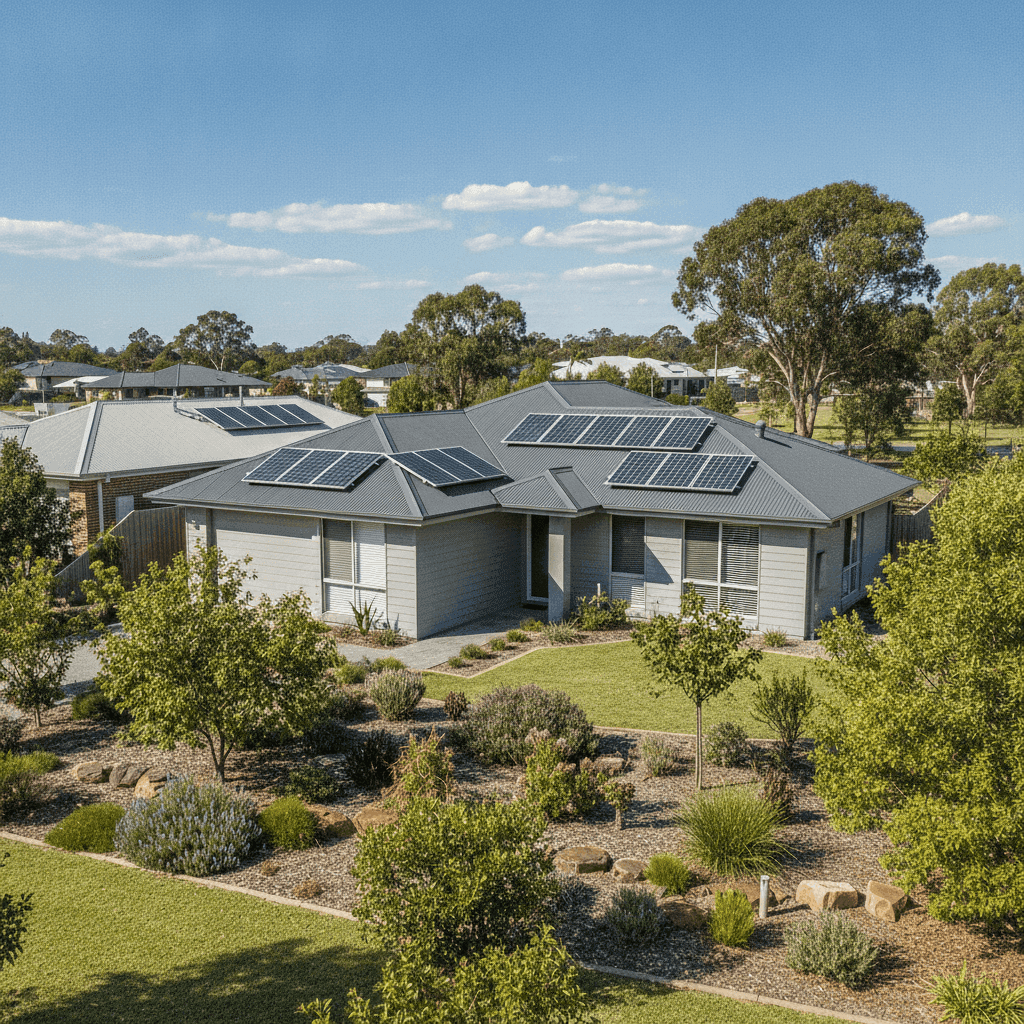

Construction year (1973): Homes built in the early 1970s are over 50 years old, which can raise flags for insurers around ageing electrical wiring, plumbing, and structural integrity. Older homes may cost more to repair or rebuild to modern standards, which can push premiums upward.

Hardiplank/Hardiflex external walls: Fibre cement cladding like Hardiplank is generally viewed favourably by insurers. It's durable, fire-resistant, and low-maintenance — all qualities that reduce the likelihood of a claim. This is likely a positive factor in keeping the premium reasonable.

Steel/Colorbond roof: Colorbond is one of the most insurer-friendly roofing materials in Australia. It's lightweight, highly durable, resistant to fire and pests, and performs well in severe weather. Homes with Colorbond roofs often attract lower premiums than those with terracotta tiles or older roofing materials.

Stump foundation: Homes on stumps (also known as pier or post foundations) are common in older Australian builds. While they allow for good airflow and can be advantageous in some flood-prone areas, they can also be more susceptible to movement, pest damage (particularly termites), and subfloor deterioration — factors insurers may weigh up.

Timber/laminate flooring: These flooring types are generally straightforward to repair or replace, but timber in particular can be vulnerable to water damage. Given the stump foundation, any subfloor moisture issues could compound this risk.

Solar panels: The presence of solar panels adds replacement value to the building sum insured and introduces a small additional risk (fire risk from inverters, for example). Insurers factor this in, though it's rarely a major premium driver.

Ducted climate control: A ducted system is a significant fixed asset and is typically included in building cover. Its presence is likely reflected in the $449,000 building sum insured rather than causing a direct premium loading.

No pool, no cyclone risk zone: Both of these are premium-friendly characteristics. Pools add liability and maintenance risk, while cyclone-rated areas in northern Australia can see premiums multiply dramatically. Neither applies here.

---

Tips for Homeowners in Vineyard

1. Review your building sum insured regularly. Construction costs have risen sharply in recent years. A sum insured of $449,000 for a 130 sqm home built in 1973 may be adequate today, but it's worth checking against a current rebuild cost estimator annually. Being underinsured at claim time can be a costly mistake.

2. Get multiple quotes before renewing. A "fair" rating means you're around the market average — but that doesn't mean a better deal isn't available. Use CoverClub to compare quotes and see whether another insurer will offer comparable cover at a lower price point.

3. Consider a pest inspection for your subfloor. With a stump foundation and timber flooring, termite activity is a genuine risk for homes in the Hawkesbury region. While standard home insurance doesn't cover termite damage, staying on top of inspections protects your home's structural integrity — and keeps your rebuild cost (and sum insured) from blowing out unexpectedly.

4. Ask about discounts for your Colorbond roof and Hardiplank walls. Some insurers offer pricing advantages for homes with fire-resistant or low-maintenance construction materials. It's worth asking your insurer directly whether your construction type qualifies for any discount, particularly if you're shopping around.

---

Ready to Compare?

Whether you're happy with your current quote or keen to explore your options, knowledge is your best tool. CoverClub makes it easy to see how your premium stacks up and compare offers from multiple insurers in one place. Get a home insurance quote today and make sure you're getting the right cover at the right price for your Vineyard home.

For more localised data on insurance pricing in your area, check out the Vineyard suburb stats page or explore NSW-wide insurance trends.