If you own a free standing home in Waaia, VIC 3637, you might be wondering whether you're paying a fair price for your home and contents insurance — or whether there's a better deal out there. In this article, we break down a real insurance quote for a three-bedroom weatherboard home in Waaia, compare it against local, state-wide, and national benchmarks, and share practical tips to help you get the most out of your cover.

---

Is This Quote Fair?

The quote in question comes in at $1,715 per year (or roughly $164 per month) for combined home and contents insurance, covering a building sum insured of $550,000 and contents valued at $50,000. The building excess is set at $5,000 and the contents excess at $1,000.

Our price rating for this quote? Cheap — well below average.

To put that in perspective, the suburb average for Waaia sits at $7,424 per year, with a median of $6,930. That means this quote is coming in at less than a quarter of what most Waaia homeowners are paying for similar cover. Even against the 25th percentile — the cheapest quarter of quotes in the suburb — this premium of $1,715 still undercuts the $5,975 mark by a significant margin.

In short: if you've received a quote in this range for a Waaia property, it's a genuinely strong result worth taking seriously.

---

How Waaia Compares

Waaia is a small rural locality in the Moira Shire, situated in northern Victoria near the Murray River floodplains. Insurance pricing in this region tends to be elevated compared to metropolitan Victoria, largely due to flood risk and the relative remoteness of the area.

Here's how the numbers stack up across different benchmarks:

| Benchmark | Average Premium |

|---|---|

| Waaia (suburb average) | $7,424/yr |

| Waaia (suburb median) | $6,930/yr |

| Moira LGA average | $4,020/yr |

| Victoria average | $3,000/yr |

| Victoria median | $2,718/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, Waaia's suburb average of $7,424 is substantially higher than both the Victorian state average of $3,000 and the national average of $5,347. This reflects the elevated risk profile of properties in the region — particularly around flood and water damage, which can push premiums up considerably for homes in low-lying parts of the Goulburn Valley.

Second, it's worth noting that the suburb sample size here is relatively small (9 quotes), so the averages should be treated as indicative rather than definitive. That said, the pattern is consistent with what we see across the broader Moira LGA, where the average sits at $4,020 — still well above the Victorian norm.

---

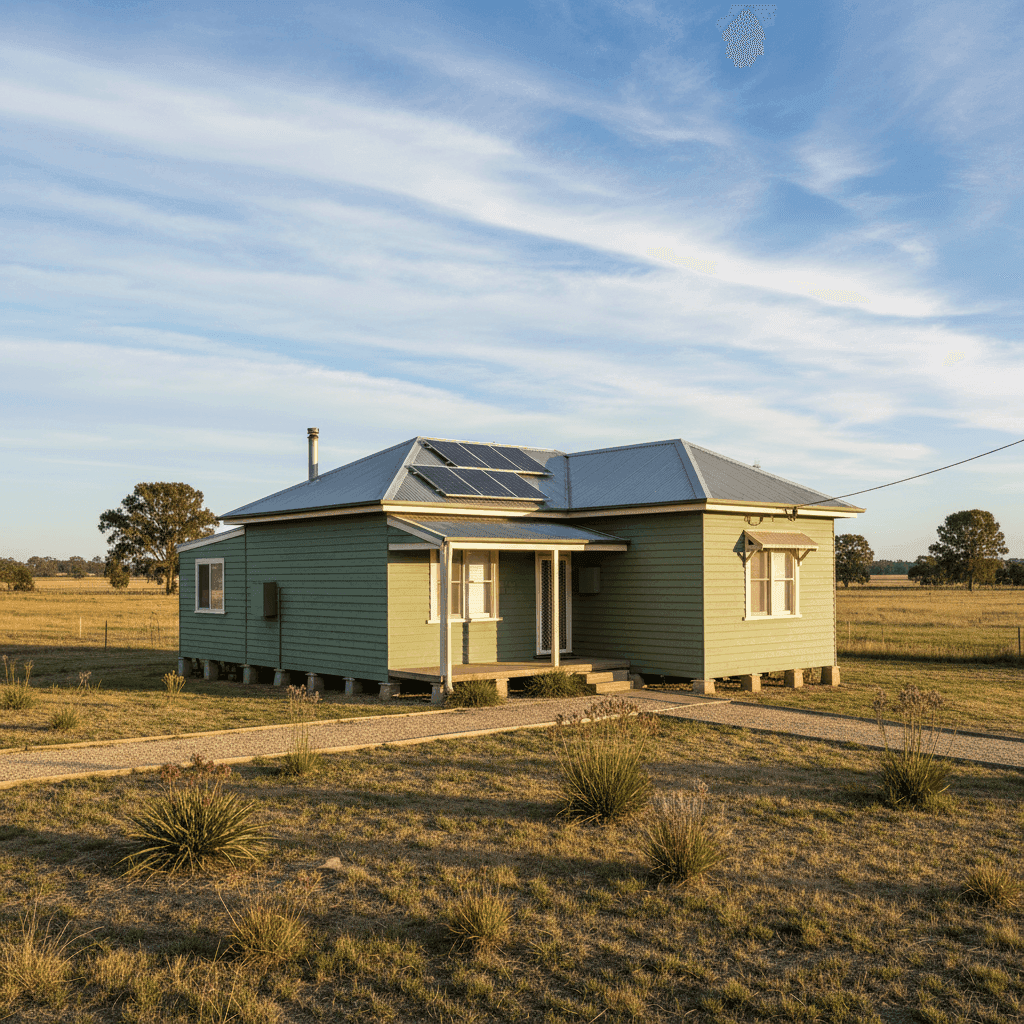

Property Features That Affect Your Premium

Several characteristics of this particular property play a meaningful role in how insurers assess and price the risk.

Weatherboard timber construction is one of the more significant factors. Timber-framed homes with weatherboard cladding are generally considered higher risk than brick veneer or double-brick homes, primarily due to fire susceptibility. Insurers often apply loadings to weatherboard homes, which can push premiums higher — making a competitive quote all the more noteworthy.

The 1963 construction year means this home is over 60 years old. Older homes can attract higher premiums due to ageing electrical wiring, plumbing systems, and structural elements that may be more costly to repair or replace. However, a well-maintained older home can still attract reasonable pricing, particularly if it has been updated over the years.

Stump foundations are common in regional Victoria, especially for homes of this era. While stumps can be re-levelled and replaced, insurers may factor in the additional complexity of repairs compared to slab foundations.

Solar panels are an increasingly common feature and are generally covered under building insurance as a fixed structure. However, homeowners should confirm that their policy explicitly includes solar panels and check whether inverter damage or storm-related panel losses are covered.

Ducted climate control adds to the overall replacement value of the home's fixtures and fittings, which is reflected in the building sum insured. Ensuring your sum insured accurately accounts for all installed systems — including ducting, compressors, and associated infrastructure — is important to avoid being underinsured.

Carpet flooring and standard fittings quality suggest a straightforward mid-range home, which generally helps keep premiums at a reasonable level compared to homes with high-end finishes or bespoke features.

---

Tips for Homeowners in Waaia

1. Review your flood cover carefully. Waaia and the surrounding Goulburn Valley region have a history of flooding. Make sure your policy explicitly includes flood cover — not just storm or rainwater damage — as these are often treated as separate events by insurers. Check the Product Disclosure Statement (PDS) closely, and if you're unsure, call your insurer directly.

2. Don't underinsure your building. A sum insured of $550,000 for a three-bedroom weatherboard home on stumps is a substantial figure, but rebuilding costs in regional areas can be higher than expected due to contractor availability and materials costs. Use a building cost calculator and review your sum insured annually to make sure it keeps pace with construction cost inflation.

3. Maintain your home proactively. Older homes benefit enormously from regular upkeep. Insurers may decline or reduce claims where damage is attributable to lack of maintenance — for example, a roof that was already in poor condition before a storm. Keeping your Colorbond roof, gutters, and stumps in good repair can also support your claim outcomes down the track.

4. Compare quotes at renewal time. Given how dramatically premiums vary in Waaia — from under $2,000 to well over $7,000 for similar properties — it pays to shop around every year. Don't assume your renewal premium is competitive just because it was good value last year.

---

Ready to Find Your Best Rate?

Whether you're insuring a weatherboard classic or a modern rural build, comparing quotes is the smartest move you can make. Head to CoverClub to get a personalised home and contents insurance quote for your Waaia property in minutes — and see exactly how your premium stacks up against the suburb, state, and national averages.