If you own a four-bedroom free standing home in Waikiki, WA 6169, you're probably curious whether you're getting a fair deal on home insurance — or quietly paying more than you need to. Located in the City of Rockingham, about 45 kilometres south of Perth's CBD, Waikiki is a well-established coastal suburb with a mix of modern homes and growing families. In this article, we break down a real home and contents insurance quote for a property in this suburb and put the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

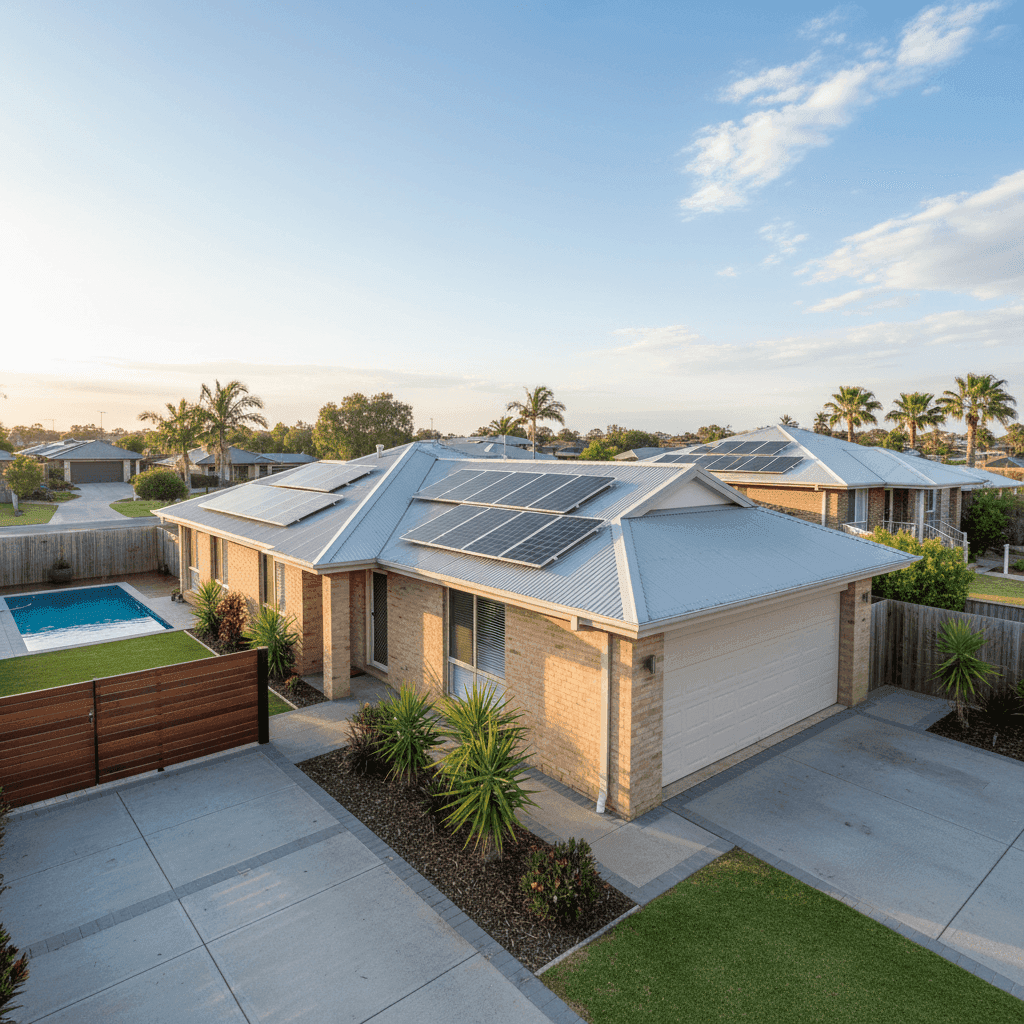

The quote under review comes in at $1,625 per year (or roughly $156 per month) for combined home and contents cover. The building is insured for $451,000 and contents are covered up to $20,000, with a $1,000 excess applying to both.

Our price rating for this quote is FAIR — around average. That assessment is based on how the premium stacks up against other quotes in the same suburb, across Western Australia, and nationally. It's not a bargain, but it's not an outlier either. For a property with features like a swimming pool, solar panels, and ducted climate control — all of which add to the replacement cost and risk profile — landing near the suburb average is a reasonable outcome.

That said, "fair" doesn't mean you can't do better. There's meaningful spread in the market, and shopping around can make a real difference.

---

How Waikiki Compares

To understand whether this quote is competitive, it helps to look at the broader pricing landscape. Based on data from 75 quotes collected for Waikiki (postcode 6169):

| Benchmark | Premium |

|---|---|

| This quote | $1,625/yr |

| Suburb average | $1,339/yr |

| Suburb median | $968/yr |

| Suburb 25th percentile | $682/yr |

| Suburb 75th percentile | $1,785/yr |

| LGA (Rockingham) average | $1,561/yr |

At $1,625, this quote sits just above the suburb average of $1,339 and comfortably within the 75th percentile of $1,785. That means roughly three-quarters of quotes in Waikiki come in cheaper — though it's worth remembering that not all quotes cover the same level of risk or the same property features.

Zooming out to the state level, the picture looks quite different. The Western Australia average home insurance premium is $2,811 per year, with a median of $2,127. The Waikiki quote is well below both figures, which reflects the relatively lower-risk profile of the southern Perth metro compared to regional WA — particularly cyclone-prone areas in the north of the state.

At the national level, the contrast is even starker. The Australian average premium sits at $5,347 per year, driven largely by high-risk regions in Queensland and northern Australia. The national median of $2,764 is still significantly higher than this Waikiki quote, reinforcing that Perth's southern suburbs remain among the more affordable areas to insure a home in Australia.

---

Property Features That Affect Your Premium

Every property is different, and insurers weigh up a range of characteristics when calculating your premium. Here's how the key features of this particular home are likely influencing the price.

Double Brick Construction Double brick is the dominant building material in Perth and is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well in storms. This is likely working in the homeowner's favour compared to properties with lightweight cladding or weatherboard exteriors.

Steel / Colorbond Roof Colorbond roofing is a popular choice in WA and is considered relatively low-risk. It's lightweight, corrosion-resistant, and performs well in high-wind events. Compared to older terracotta or concrete tile roofs — which can crack, leak, or become dislodged — a steel roof is generally a positive signal for insurers.

Slab Foundation A concrete slab is a straightforward and stable foundation type. It carries less risk of subsidence or moisture-related damage compared to pier-and-beam or older strip footings, which can be a factor in some Perth suburbs with reactive soils.

Swimming Pool Pools add to the insured value of the property and can also introduce liability considerations. Homeowners with pools should ensure their policy includes adequate coverage for the pool structure itself, as well as any associated equipment like pumps and filtration systems.

Solar Panels Solar panels are increasingly common in WA, but they do add to the replacement cost of a home. Some insurers include panels automatically under building cover; others treat them as a separate item. It's worth confirming exactly how your policy handles solar — especially if you have a battery storage system as well.

Ducted Climate Control Ducted air conditioning is a significant fixed asset. Like solar panels, it contributes to the overall replacement cost of the building and should be factored into your sum insured calculation to avoid being underinsured.

Timber / Laminate Flooring Flooring type can affect contents and building claims, particularly in the event of water damage. Timber and laminate floors can be costly to replace, so it's worth ensuring your building sum insured accounts for this.

---

Tips for Homeowners in Waikiki

Whether you're renewing your policy or shopping around for the first time, here are a few practical steps worth taking.

1. Review your sum insured regularly Construction costs have risen significantly in recent years. The $451,000 building sum insured on this quote may have been accurate when it was set, but it's worth recalculating using an independent building cost estimator to make sure you're not underinsured. Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Check exactly what's covered for your pool and solar Not all policies treat pools and solar panels the same way. Some include them automatically under building cover; others require you to list them separately or pay an additional premium. Read the Product Disclosure Statement (PDS) carefully, or ask your insurer directly.

3. Consider a higher excess to reduce your premium The current excess on this policy is $1,000 for both building and contents. If you're in a financial position to absorb a higher out-of-pocket cost in the event of a claim, increasing your excess to $1,500 or $2,000 can meaningfully reduce your annual premium.

4. Compare quotes before your renewal date Loyalty doesn't always pay in insurance. Premiums can vary significantly between providers for virtually identical cover. Using a comparison tool before your renewal date — rather than simply accepting the auto-renewal — is one of the easiest ways to ensure you're getting value for money.

---

Find a Better Deal on CoverClub

Whether this quote looks competitive or a little steep for your situation, it always pays to compare. At CoverClub, you can enter your property details and see how quotes stack up across multiple insurers — all in one place. It takes just a few minutes and could save you hundreds of dollars a year.