If you own a four-bedroom free standing home in Walligan, QLD 4655, you're probably well aware that insurance costs in Queensland can be a bit of a moving target. Situated in the Fraser Coast region, Walligan is a quiet residential area where property values — and the cost to protect them — vary considerably depending on a range of factors. This article breaks down a real home and contents insurance quote for a property in the suburb, benchmarks it against local, state, and national data, and offers practical tips to help you get the most out of your cover.

---

Is This Quote Fair?

The quote in question comes in at $2,532 per year (or $236 per month) for combined home and contents cover, with a building sum insured of $800,000 and contents valued at $53,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote? Cheap — below average. That's genuinely good news for the homeowner.

To put it in context: the suburb average for Walligan sits at $5,493 per year, with a median of $5,292. This quote comes in at less than half the suburb average — a significant saving of roughly $2,961 annually compared to what other Walligan homeowners are typically paying.

Even when stacked against the national average of $5,347 per year, this premium is well below the mark. The national median of $2,764 is the closest benchmark this quote approaches, and it still undercuts it by over $200 per year.

In short: if you're the homeowner holding this quote, it represents excellent value relative to what the market is charging for comparable properties in your area.

---

How Walligan Compares

Understanding where Walligan sits in the broader insurance landscape helps put individual quotes into perspective.

| Benchmark | Premium |

|---|---|

| This Quote | $2,532/yr |

| Walligan Suburb Average | $5,493/yr |

| Walligan Suburb Median | $5,292/yr |

| Walligan 25th Percentile | $4,490/yr |

| Walligan 75th Percentile | $6,170/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. First, the Queensland state average of $9,129 per year is extraordinarily high — more than three times this quote — largely driven by high-risk coastal and cyclone-prone postcodes in North Queensland. The state median of $3,903 is a more realistic reflection of what many Queensland homeowners pay, and this quote still beats it comfortably.

It's also worth noting that the suburb sample size is relatively small (7 quotes), so the Walligan averages should be interpreted with some caution. That said, the spread between the 25th percentile ($4,490) and 75th percentile ($6,170) suggests meaningful variation in what local homeowners are being quoted — and this property is sitting well below even the cheapest end of that range.

---

Property Features That Affect Your Premium

Several characteristics of this property likely contribute to its favourable premium. Let's unpack them.

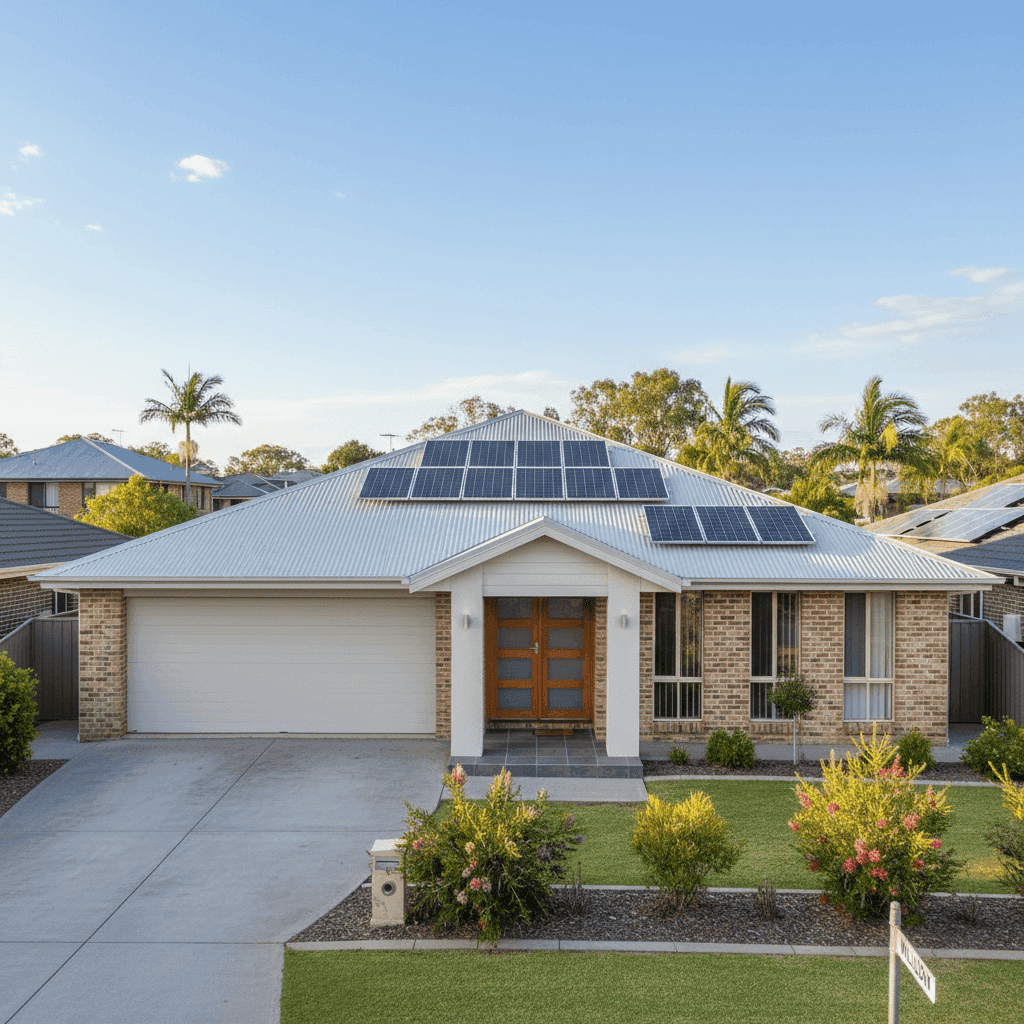

Brick Veneer Walls & Colorbond Roof Brick veneer construction is generally well-regarded by insurers for its durability and fire resistance. Combined with a steel Colorbond roof — one of the most resilient roofing materials available in Australia — this property presents a lower claims risk profile than homes built with timber frames and terracotta tiles, for example.

Slab Foundation A concrete slab foundation is considered low-maintenance and structurally sound in most Queensland soil conditions. It reduces the risk of subsidence and pest-related structural damage, both of which can drive up premiums.

Construction Year: 2006 Homes built in the mid-2000s generally comply with modern building codes that include improved cyclone, fire, and flood resilience standards. This is a sweet spot for insurers — not so old that the home has significant wear, and built to stronger standards than many older Queensland properties.

No Pool The absence of a swimming pool removes a common liability risk from the equation. Pools can add to both the replacement cost and the liability exposure of a property, so their absence tends to have a modest downward effect on premiums.

Solar Panels & Ducted Climate Control Solar panels and ducted air conditioning are both listed as features of this property. Solar panels add to the replacement value of the home and can increase the sum insured required — it's worth confirming these are covered under the building policy. Ducted climate control systems are similarly expensive to replace, so ensuring your sum insured adequately accounts for these features is important.

Not in a Cyclone Risk Area This is a significant factor. Much of Queensland's premium inflation is driven by cyclone-prone postcodes in the north of the state. Walligan's classification as outside a designated cyclone risk area means the property avoids the substantial loading that pushes many Queensland premiums into the thousands. This is arguably the single biggest reason this quote compares so favourably against the state average.

Standard Fittings Quality Standard-grade fixtures and fittings keep the replacement cost estimate grounded. High-end or custom fittings can significantly increase rebuild costs and, by extension, the premium required to adequately insure a property.

---

Tips for Homeowners in Walligan

Whether you're reviewing an existing policy or shopping around for the first time, here are four practical steps worth taking.

1. Review Your Sum Insured Annually With a building sum insured of $800,000 on a 214 sqm home, it's worth verifying this figure reflects current construction costs. Building costs in Queensland have risen sharply in recent years due to labour shortages and material price increases. Underinsurance is one of the most common — and costly — mistakes homeowners make. Use a building cost calculator or speak to a local builder to sense-check your figure each year.

2. Confirm Solar Panels Are Covered Solar panel systems can cost anywhere from $5,000 to $15,000 or more to replace. Check your policy wording carefully to confirm whether panels are covered under the building section, and whether the sum insured is sufficient to include them. Some insurers cover them automatically; others require them to be specifically noted.

3. Don't Over-Insure Contents — But Don't Under-Insure Either A contents value of $53,000 is relatively modest for a four-bedroom home. Walk through each room and make a realistic list of everything you'd need to replace — furniture, appliances, clothing, electronics, and personal items. Many homeowners are surprised to find their contents are worth significantly more than they estimated.

4. Compare Quotes Regularly Even if your current premium looks competitive, the insurance market shifts constantly. Insurers reprice based on claims data, reinsurance costs, and risk modelling updates. What's cheap today may not be next renewal. Get a fresh quote at CoverClub to make sure you're not leaving money on the table.

---

Compare Your Home Insurance Today

Whether this quote is yours or you're simply curious about what homeowners in Walligan are paying, CoverClub makes it easy to benchmark your premium against real market data. Visit coverclub.com.au to get a quote and see how your current cover stacks up — you might be surprised by what you find.