Wallington is a quiet residential suburb on Victoria's Bellarine Peninsula, sitting just outside Geelong and within easy reach of the surf beaches and coastal lifestyle that make this corner of the state so desirable. For owners of a four-bedroom, free-standing home in the area, protecting that asset with the right home and contents insurance is a serious financial decision — and the premium you pay can vary significantly depending on who you ask.

This article takes a close look at a recent home and contents insurance quote for a four-bedroom, three-bathroom free-standing home in Wallington (postcode 3222), breaking down whether the price stacks up and what local homeowners can do to make sure they're getting value for money.

---

Is This Quote Fair?

The quoted annual premium for this property comes in at $3,659 per year (or $344 per month), covering a building sum insured of $954,000 and contents valued at $311,000, each with a $1,000 excess.

Our price rating for this quote is Expensive — Above Average.

To put that in context: the suburb average for Wallington sits at $3,107 per year, and the suburb median is a notably lower $2,541 per year. This quote lands well above both benchmarks, and also above the 75th percentile for the suburb ($3,091/yr) — meaning it's pricier than roughly three-quarters of comparable quotes in the area.

Against the broader Victorian market, the picture is similar. The state average for VIC is $3,000 per year, with a median of $2,718 per year. Again, this quote exceeds both figures.

That said, it's worth noting that the building sum insured here ($954,000) is substantial, and the contents cover ($311,000) is also on the higher end. Higher insured values naturally push premiums up, so some of the price gap may reflect the scope of cover rather than the insurer simply charging more for the same thing.

---

How Wallington Compares

Understanding where Wallington sits in the broader insurance landscape helps put individual quotes into perspective. Here's a snapshot:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,659 |

| Wallington Suburb Average | $3,107 |

| Wallington Suburb Median | $2,541 |

| Wallington 25th Percentile | $2,236 |

| Wallington 75th Percentile | $3,091 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

| Greater Geelong LGA Average | $1,754 |

You can explore the full breakdown for this postcode at the Wallington suburb stats page, or compare it against national home insurance data.

One figure that stands out is the Greater Geelong LGA average of just $1,754 per year — considerably lower than both the suburb and state figures. This likely reflects the diversity of properties across the LGA, including smaller or lower-value homes that bring the average down. Wallington, as a more established suburb with larger homes, tends to attract higher premiums.

On the national scale, this quote is actually below the national average of $5,347 per year, which is driven upward by high-risk areas in Queensland and Western Australia — particularly cyclone-prone regions. For a Victorian homeowner, that national figure isn't the most useful comparison point, but it does serve as a reminder that insurance costs vary enormously across the country.

---

Property Features That Affect Your Premium

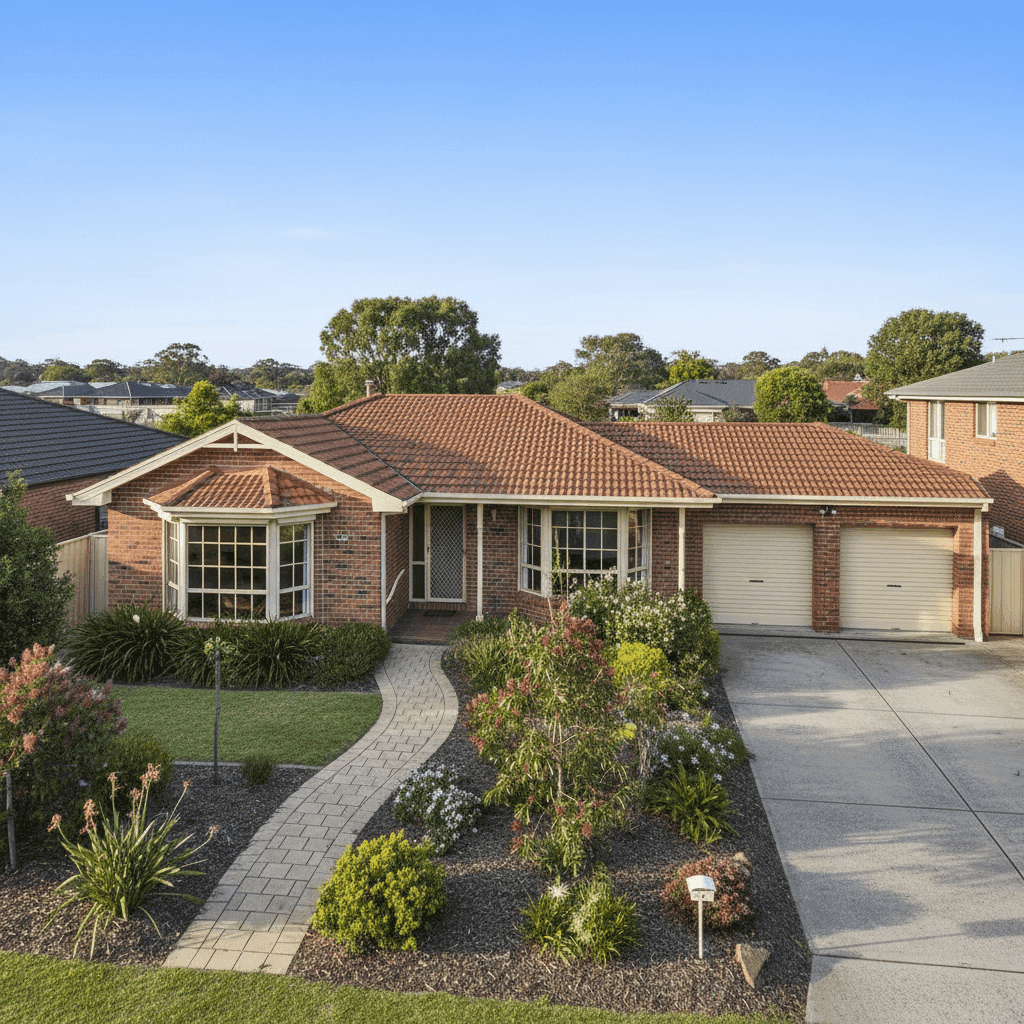

Several characteristics of this particular property have a meaningful influence on its insurance premium.

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability, which can help moderate premiums compared to weatherboard or other timber-framed exteriors. The tiled roof is similarly well-regarded — tiles are long-lasting and perform well in most weather conditions, unlike some metal or flat roofing options.

A slab foundation is standard for many Victorian homes built in the late 1980s and is considered low-risk from an insurer's perspective, as it doesn't carry the same subsidence concerns as older pier-and-beam setups.

The home was built in 1989, which places it in a middle ground — old enough that some components (roofing, plumbing, electrical) may be approaching the end of their serviceable life, but modern enough to meet building codes that weren't in place for pre-1970s construction. Insurers may factor in the age of the property when assessing risk.

Above-average fittings quality is a significant driver of both the building sum insured and the premium itself. Homes with higher-end kitchens, bathrooms, and finishes cost more to rebuild or repair to the same standard, which is reflected in the $954,000 building cover figure.

The property also features ducted climate control, which adds to the replacement value and is worth ensuring is explicitly covered in your policy. At 214 sqm, this is a generously sized home, and the combination of size, quality fittings, and three bathrooms all contribute to the higher-than-average sum insured.

---

Tips for Homeowners in Wallington

If you're a homeowner in Wallington looking to make sure you're getting the best deal on your home and contents insurance, here are some practical steps worth taking:

- Shop around and compare multiple quotes. The spread between the 25th and 75th percentile in Wallington is over $850 per year — meaning the market varies considerably for similar properties. Don't assume your renewal price is competitive without checking. Use CoverClub to compare quotes side by side.

- Review your sum insured carefully. Over-insuring your building or contents means you're paying more premium than necessary. Under-insuring, on the other hand, can leave you badly exposed at claim time. Consider getting a professional building valuation to make sure your $954,000 figure accurately reflects your home's rebuild cost — not its market value.

- Consider a higher excess to reduce your premium. Both the building and contents excess on this quote are set at $1,000. Increasing your voluntary excess can meaningfully lower your annual premium, particularly if you're unlikely to make small claims. Just make sure the excess remains affordable if you do need to claim.

- Check what's included for your ducted system and fittings. Policies vary widely in how they treat fixed appliances, built-in systems, and high-value fittings. Read the Product Disclosure Statement (PDS) carefully to confirm that your ducted climate control and above-average fixtures are covered for their full replacement value, not just a standard allowance.

---

Ready to Find a Better Rate?

Whether this quote is the right fit or you suspect you could do better, the smartest move is to compare. At CoverClub, we make it easy for Australian homeowners to see how their premium stacks up and explore alternatives — all in one place. Get a home insurance quote today and find out if you're paying more than you need to.