If you own a free standing home in Walterhall, QLD 4714, you've probably noticed that home insurance isn't cheap — and working out whether your quote is reasonable can feel like guesswork. This article breaks down a real building insurance quote for a 2-bedroom weatherboard home in the area, compares it against local, state, and national benchmarks, and highlights the property features most likely to be influencing the price.

---

Is This Quote Fair?

The quote in question comes in at $4,305 per year (or $413 per month) for building-only cover, with a $2,000 building excess and a sum insured of $380,000. Our price rating for this quote is FAIR — around average.

That "fair" rating isn't a rubber stamp of approval, but it is reassuring. It means the premium sits within a normal range for this type of property in this location — you're not being gouged, but there may still be room to find a better deal with a different insurer.

To put it in context: the suburb average for Walterhall sits at $4,079 per year, with a median of $4,374. At $4,305, this quote lands just below the suburb median and slightly above the suburb average — squarely in the middle of the pack.

The interquartile range for Walterhall (25th to 75th percentile) runs from $3,174 to $4,887, which means roughly half of all quotes in the suburb fall within that band. This quote sits comfortably inside that range, which reinforces the "around average" assessment.

---

How Walterhall Compares

Understanding your premium in isolation only tells part of the story. Here's how Walterhall stacks up against broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Walterhall (suburb) | $4,079/yr | $4,374/yr |

| Rockhampton LGA | $4,824/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The Queensland state average of $9,129 is dramatically higher than the median of $3,903 — a sign that QLD premiums are heavily skewed by high-risk coastal and cyclone-prone areas, which pull the average up significantly. Walterhall, sitting inland near Rockhampton, doesn't carry the same coastal exposure, which helps keep premiums more moderate.

Compared to the national average of $5,347, this quote is notably cheaper. However, the national median of $2,764 is much lower, reflecting the large number of lower-risk, lower-cost properties across the country (particularly in southern states) that bring the midpoint down.

For a more relevant comparison, the Rockhampton LGA average of $4,824 is the most useful benchmark. At $4,305, this quote comes in around $519 below the LGA average — a meaningful saving that suggests the property's specific characteristics are working in the homeowner's favour to some degree.

You can explore more detailed Queensland insurance statistics here or view national home insurance benchmarks for a broader picture.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining when it comes to understanding the premium:

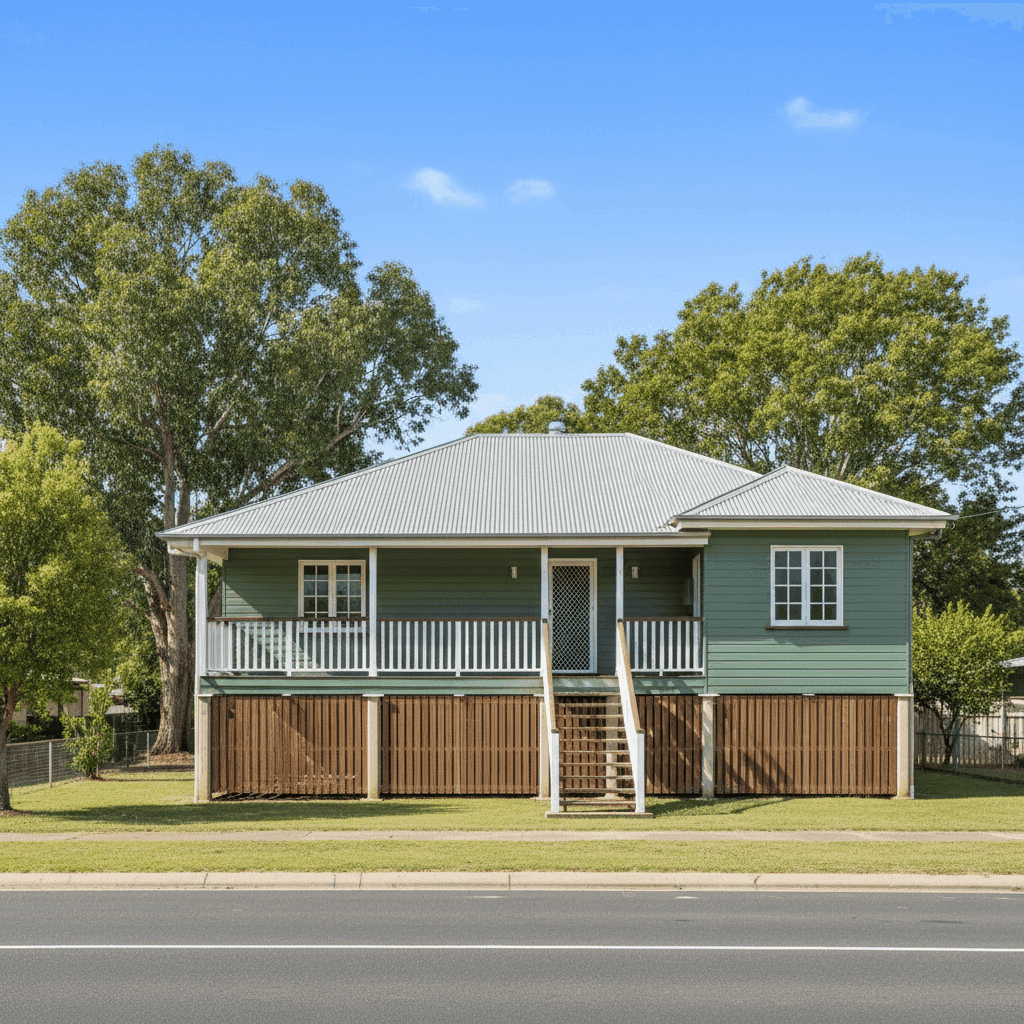

Weatherboard Timber Walls

Weatherboard wood construction is one of the most common wall types in older Queensland homes, but it does carry a higher risk profile than brick or cavity brick. Timber is more susceptible to fire, termite damage, and general wear — all factors that insurers price into their calculations.

Elevated on Stumps

This home is elevated by at least one metre on stumps — a classic Queenslander-style foundation. The good news is that elevation can actually reduce flood risk, as water is less likely to reach the living areas during heavy rain events. However, stumped foundations do introduce their own risks, including structural movement and the potential for subfloor damage.

Steel/Colorbond Roof

A Colorbond steel roof is generally viewed favourably by insurers. It's durable, fire-resistant, and performs well in high-wind events — all positives from a risk-assessment perspective. Compared to older terracotta or asbestos roofing, this is a relatively low-risk material.

Construction Year: 1940

Age matters in insurance. An 84-year-old home may have ageing electrical wiring, plumbing, and structural elements that increase the likelihood of a claim. Insurers typically apply a loading for older homes, and this property's 1940 construction date is likely contributing to the premium.

Ducted Climate Control

The presence of ducted climate control adds to the sum insured and the overall rebuild cost — systems like these are expensive to replace. It's a relatively minor factor, but worth noting.

No Pool, No Solar

The absence of a pool and solar panels simplifies the risk profile slightly. Both features can add complexity to a claim and occasionally attract a small premium loading, so their absence is a mild positive.

---

Tips for Homeowners in Walterhall

1. Review Your Sum Insured Regularly

At $380,000 for a 105 sqm home, the sum insured reflects the cost to rebuild — not the market value of the property. Construction costs have risen sharply in recent years, so it's worth revisiting this figure annually to make sure you're not underinsured. Many insurers offer a building calculator to help.

2. Consider Raising Your Excess

The current building excess is $2,000. If you're comfortable covering smaller claims out of pocket, opting for a higher excess (say, $2,500 or $3,000) can meaningfully reduce your annual premium. Just make sure the saving is worth the trade-off.

3. Maintain Your Weatherboard Exterior

Insurers can reduce or deny claims if a loss is attributed to lack of maintenance. Keeping your weatherboard in good condition — painted, sealed, and free from rot — not only protects your home but also protects your ability to claim. Regular checks under the house for termite activity are equally important.

4. Shop Around at Renewal Time

With a sample of only 6 quotes in the Walterhall area, the local market is relatively thin. That makes it even more important to compare quotes from multiple insurers rather than simply renewing with your current provider. Premiums can vary by hundreds — or even thousands — of dollars for the same property.

---

Find a Better Deal on CoverClub

Whether you're happy with your current quote or looking for something more competitive, it always pays to compare. At CoverClub, you can benchmark your premium against real data from properties just like yours and explore options from a range of Australian insurers.

Get a home insurance quote today and see how your premium stacks up — it only takes a few minutes.