Wangi Wangi is a relaxed lakeside suburb on the western shores of Lake Macquarie in NSW — a sought-after location known for its waterfront lifestyle, leafy streets, and strong community feel. For owners of a free standing home in this area, understanding what you should be paying for home and contents insurance is just as important as finding the right policy. This article breaks down a real insurance quote for a 3-bedroom, 2-bathroom brick veneer home in Wangi Wangi, and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,950 per year (or $283/month) for combined home and contents cover, with a building sum insured of $577,000 and contents valued at $100,000. Both the building and contents excess are set at $500 — a fairly standard arrangement.

Based on our pricing data, this quote is rated CHEAP — meaning it sits meaningfully below the average for comparable properties in the Wangi Wangi area. To put that in perspective, the suburb average premium is $3,876/year and the median sits at $3,597/year. This quote falls below even the 25th percentile of $3,049/year for the suburb, which means it's cheaper than at least 75% of quotes we've seen for this postcode.

That's a strong result. For a property with a pool, solar panels, and ducted climate control — all of which can nudge premiums upward — landing below the suburb's lower quartile is genuinely impressive. Whether you're reviewing your current policy or shopping around for the first time, this benchmark gives you a useful anchor point.

---

How Wangi Wangi Compares

Understanding your premium in isolation only tells part of the story. Here's how Wangi Wangi (NSW 2267) stacks up against broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Wangi Wangi (suburb) | $3,876/yr | $3,597/yr |

| Lake Macquarie LGA | $11,064/yr avg | — |

| NSW (state) | $9,528/yr avg | $3,770/yr |

| National | $5,347/yr avg | $2,764/yr |

A few things stand out here. The NSW state average of $9,528/year looks alarming at first glance, but it's heavily skewed by high-risk and high-value properties across the state — the median of $3,770/year is far more representative of what most NSW homeowners actually pay. Similarly, the Lake Macquarie LGA average of $11,064/year reflects a wide spread of property types and risk profiles across a large and diverse council area.

Compared to the national median of $2,764/year, Wangi Wangi's suburb median of $3,597/year is moderately higher — not unusual for a lakeside NSW location where some flood or storm exposure can factor into pricing. The quote analysed here, at $2,950/year, sits comfortably between the national median and the suburb median, suggesting it represents genuine value for this type of property.

Our suburb data is drawn from a sample of 47 quotes for the Wangi Wangi postcode, giving a solid basis for comparison.

---

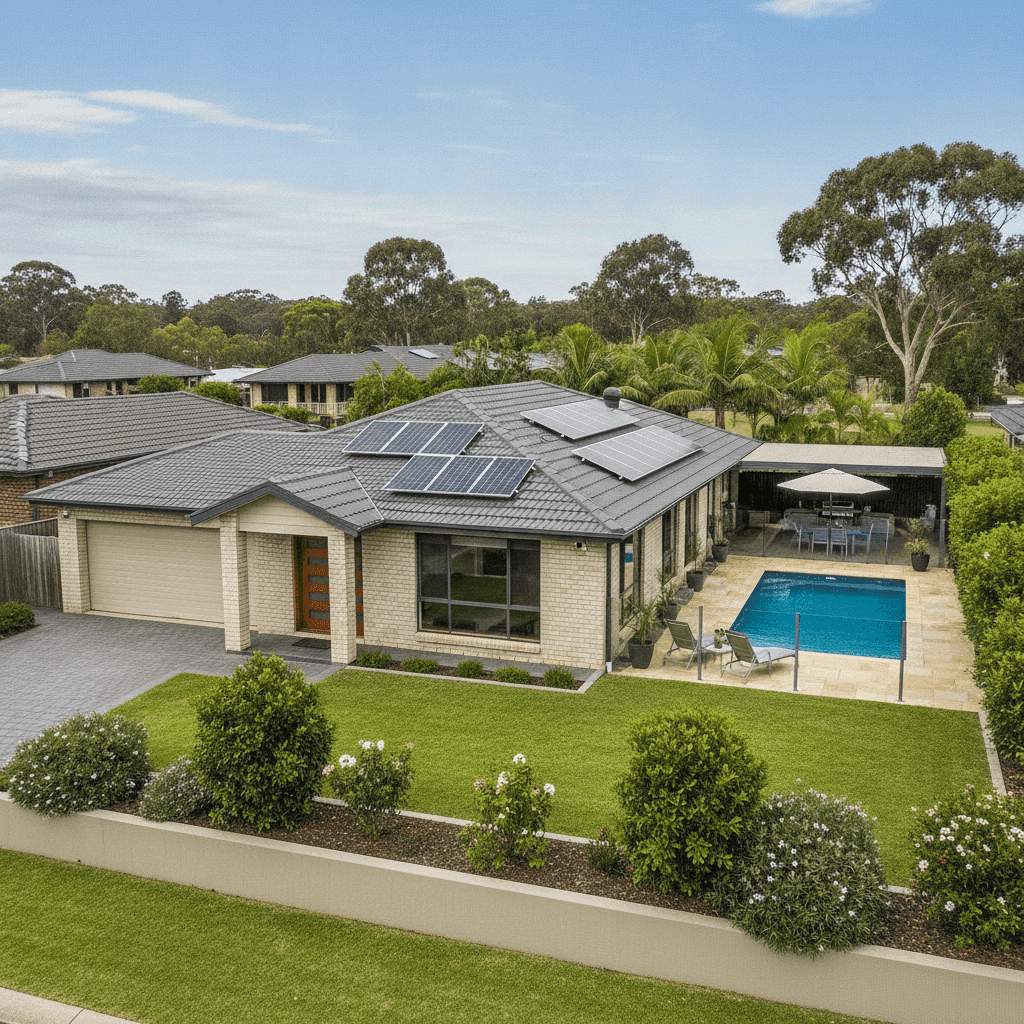

Property Features That Affect Your Premium

Every property is different, and insurers price risk based on a combination of location, construction, and features. Here's how the key characteristics of this property are likely influencing the premium:

Brick Veneer Walls & Tiled Roof Brick veneer construction with a tiled roof is generally viewed favourably by insurers. These materials offer solid fire resistance and durability compared to timber weatherboard or metal cladding, which can contribute to a more competitive premium.

Stump Foundation & Timber/Laminate Flooring The property sits on stumps — a common foundation type in older NSW homes, particularly in areas with reactive soils or where ventilation beneath the floor is beneficial. While this foundation type is generally well-understood by insurers, it can occasionally attract closer scrutiny. Timber and laminate flooring is a standard finish and unlikely to significantly affect pricing.

Built in 1993 At around 30 years old, this home sits in a comfortable middle ground — old enough to have some character, but not so old that insurers become wary of ageing wiring, plumbing, or structural concerns. Homes built in the 1990s typically meet reasonable building standards and are straightforward to insure.

Swimming Pool A pool adds liability exposure and increases the overall replacement cost of the property, both of which can push premiums up. It's worth ensuring your sum insured accounts for the full cost of pool reinstatement.

Solar Panels Solar panels are an increasingly common feature, but they do add to your building's replacement value. Make sure your sum insured of $577,000 factors in the cost of reinstating your solar system — a quality ducted system and panels can add tens of thousands to a rebuild cost.

Ducted Climate Control Ducted air conditioning is a significant fixed asset. Like solar panels, it forms part of the building and should be captured in your sum insured. Under-insurance is a real risk for homes with premium fixtures and fittings.

No Cyclone Risk Wangi Wangi falls outside designated cyclone risk zones, which removes one of the more significant premium loading factors that affect properties in northern Queensland and parts of WA. This contributes to the relatively competitive pricing available in this area.

---

Tips for Homeowners in Wangi Wangi

1. Review your sum insured annually With construction costs rising across NSW, the cost to rebuild your home can increase significantly year on year. A sum insured of $577,000 for a 139 sqm brick veneer home with a pool and solar panels is worth validating with a quantity surveyor or online calculator. Being under-insured at claim time can leave you seriously out of pocket.

2. Check your contents cover reflects reality $100,000 in contents cover is a reasonable starting point, but it's easy to underestimate the cumulative value of furniture, electronics, appliances, clothing, and personal items. Do a room-by-room audit every year or two to make sure your contents sum is keeping pace.

3. Consider your flood and storm exposure While Wangi Wangi isn't classified as a cyclone risk area, properties near Lake Macquarie can be exposed to localised flooding and storm surge events. Check whether your policy includes flood cover as standard or as an optional extra — and review the definition of "flood" carefully, as it varies between insurers.

4. Compare quotes at renewal time The fact that this quote is rated cheap relative to the suburb average is a good reminder that premiums vary significantly between insurers — even for the same property. Loyalty doesn't always pay in insurance. Running a comparison at renewal takes only a few minutes and can save hundreds of dollars a year.

---

Ready to See What You Could Pay?

Whether you're a first-time buyer or a long-term Wangi Wangi local, comparing home insurance quotes is one of the simplest ways to make sure you're not overpaying. CoverClub makes it easy to see real quotes for your specific property in minutes. Get a quote today and find out where your premium sits relative to your neighbours.