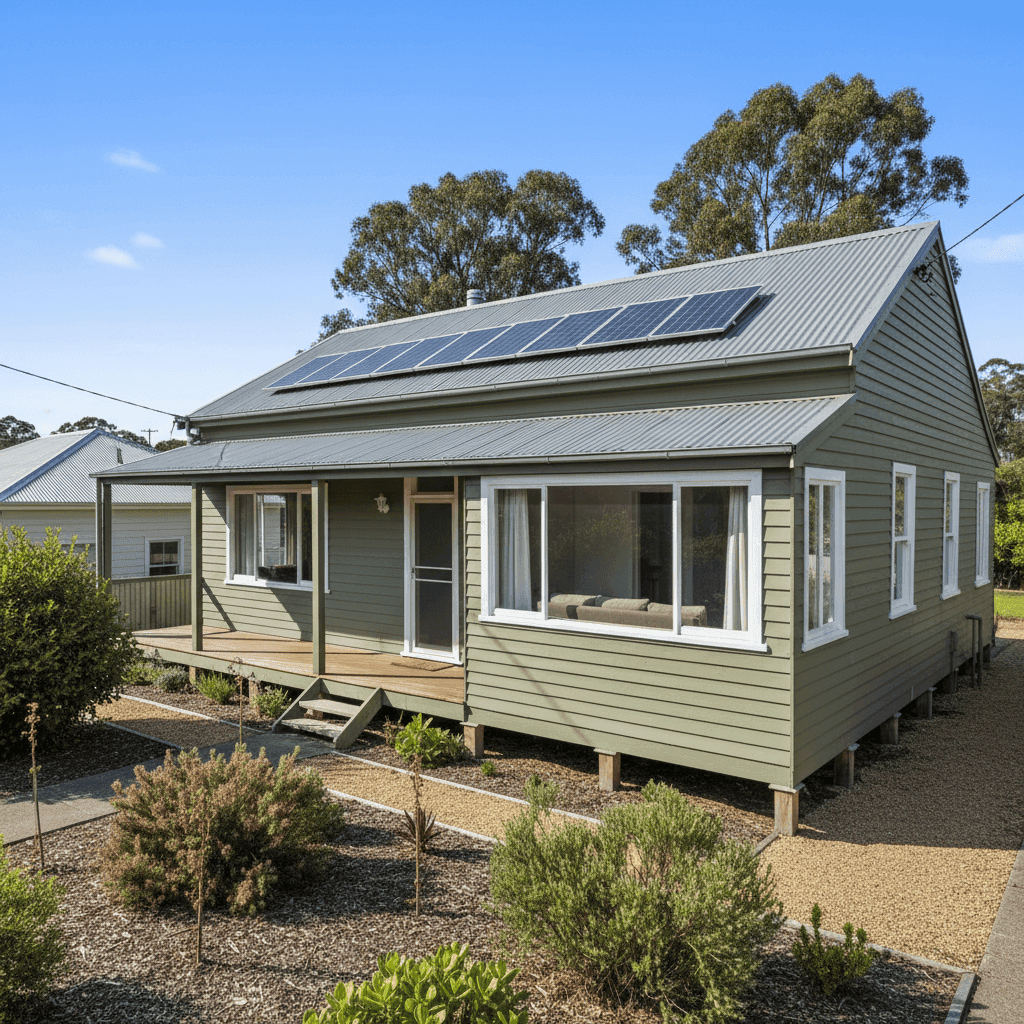

Waratah is a small historic township in Tasmania's rugged north-west, sitting in the Kentish local government area and surrounded by dense bushland and the West Coast Ranges. It's the kind of place where homes carry real character — and this 2-bedroom, 1-bathroom semi detached property, built in 1975, is no exception. But character comes with complexity when it comes to insuring older homes, and this particular quote of $6,485 per year (or $621 per month) for combined home and contents cover warrants a closer look.

---

Is This Quote Fair?

The short answer: this quote is rated Expensive — above average for the area, and significantly above most benchmarks we'd expect for a property of this type in Waratah.

The building is insured for $452,000 and contents for $85,000, which are reasonable sums for a well-fitted home of 105 sqm with above-average fittings quality. However, the annual premium of $6,485 sits well above what most comparable properties in the suburb are paying. With a building excess and contents excess of $1,000 each, the policyholder is already shouldering meaningful out-of-pocket risk before the insurer steps in — which typically pushes premiums down, not up. The fact that this quote remains this high despite those excesses is a signal worth investigating.

There are several property-specific factors that could be driving the cost upward (more on those below), but homeowners in this situation should absolutely be shopping around before accepting this figure as the market rate.

---

How Waratah Compares

To put this quote in context, here's how it stacks up against suburb, state, and national benchmarks:

| Benchmark | Premium |

|---|---|

| This quote | $6,485/yr |

| Waratah suburb average | $2,538/yr |

| Waratah suburb median | $2,847/yr |

| Waratah 75th percentile | $3,478/yr |

| TAS state average | $2,814/yr |

| TAS state median | $2,326/yr |

| Kentish LGA average | $2,013/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

Even measured against the national average of $5,347, this quote is elevated. Compared to the Tasmanian state average of $2,814, it's more than double. And against the Waratah suburb average of $2,538, it's nearly 2.6 times what neighbours are typically paying.

It's worth noting that the suburb sample size here is relatively small (8 quotes), so averages can shift with a few outliers. Still, even the 75th percentile for Waratah sits at $3,478 — meaning this quote exceeds the most expensive quarter of the local market by nearly $3,000. That's a substantial gap that deserves scrutiny.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium, some of which are inherently higher-risk from an insurer's perspective.

Weatherboard timber construction is one of the most significant factors. Older timber-framed homes — particularly those built in the 1970s — are considered higher risk for fire, rot, and structural deterioration. Insurers often apply loading to premiums for weatherboard exteriors, especially when combined with an older construction year like 1975.

Stump foundations add another layer of complexity. Elevated homes on stumps can be more vulnerable to underfloor moisture, pest damage, and movement over time. While this property is only elevated by less than 1 metre, the foundation type alone can trigger additional scrutiny from underwriters.

A steel/Colorbond roof is generally viewed favourably — it's durable, low-maintenance, and performs well in adverse weather. This likely works in the homeowner's favour and may be moderating the premium to some degree.

Solar panels are an increasingly common feature but do add to the replacement cost of a building. Depending on how the policy treats solar systems (some cover them under building, others require separate endorsement), this could be contributing to the higher sum insured.

Ducted climate control also adds to the building's replacement value and is consistent with the above-average fittings quality noted in the property details. Higher-quality fittings mean higher rebuild costs, which flow directly into the premium calculation.

Carpet flooring is a contents consideration — wall-to-wall carpet can be expensive to replace after water damage or fire, and insurers factor this into contents risk assessments.

Taken together, this is a property with a number of features that individually push premiums upward. The combination of older timber construction, stump foundations, solar panels, and premium fittings creates a compounding effect that helps explain — though perhaps not fully justify — the quote received.

---

Tips for Homeowners in Waratah

If you're looking at a quote like this and wondering what you can do, here are some practical steps:

- Compare multiple insurers. This is the single most impactful thing you can do. Premiums for the same property can vary by thousands of dollars between providers. Get a comparison quote through CoverClub to see what other insurers are offering for your specific property profile.

- Review your sum insured carefully. A building sum insured of $452,000 for a 105 sqm semi detached in Waratah is worth validating against a current building cost calculator. Over-insuring drives premiums up unnecessarily, while under-insuring leaves you exposed. Make sure your figure reflects realistic rebuild costs — not market value.

- Ask about premium discounts for security and safety upgrades. Many insurers offer reductions for properties with monitored alarm systems, deadbolts, smoke detectors, and other risk-mitigation features. If your home has these, ensure they're declared correctly on your application.

- Consider whether your excess level is optimised. With both building and contents excesses already set at $1,000, you're taking on meaningful risk. Some insurers allow you to increase this further in exchange for a lower premium — worth exploring if you have a solid emergency fund and rarely make small claims.

---

Ready to Find a Better Rate?

A premium of $6,485 per year is a significant household expense, and given how far it sits above the local and state averages, there's a strong case for shopping around. At CoverClub, you can compare home and contents insurance quotes from multiple Australian insurers in minutes — tailored to your property's specific features. Don't pay more than you need to. See what the market is actually offering for a home like yours in Waratah.