Nestled in the Upper Yarra Valley at the foothills of the Victorian Alps, Warburton is a picturesque township that attracts buyers seeking a tree-change lifestyle. But living in a lush, forested setting comes with its own insurance considerations. This article breaks down a real home and contents insurance quote for a free standing home in Warburton (postcode 3799), and puts it into context against suburb, state, and national pricing data so you can judge whether you're getting a fair deal.

---

Is This Quote Fair?

The quote in question comes in at $3,515 per year (or $337/month) for combined home and contents cover, with a building sum insured of $659,000 and contents valued at $30,000. Both the building and contents excess are set at $5,000.

Based on our pricing data, this quote is rated CHEAP — below the suburb average — which is genuinely good news for this homeowner. Given Warburton's elevated bushfire risk profile and the age of the property (built in 1950), securing a below-average premium is a meaningful outcome.

The $5,000 excess on both building and contents is notably high, and it's worth acknowledging that this almost certainly plays a role in keeping the annual premium down. A higher excess means the insurer carries less risk on smaller claims, which they reward with a lower upfront cost. Homeowners should be comfortable self-funding losses up to that threshold before this policy kicks in.

---

How Warburton Compares

The pricing data for Warburton tells a striking story. According to suburb-level statistics for Warburton VIC 3799, drawn from 59 quotes:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,515 |

| Suburb 25th Percentile | $4,911 |

| Suburb Median | $6,253 |

| Suburb 75th Percentile | $11,225 |

| Suburb Average | $20,658 |

| LGA (Yarra Ranges) Average | $5,600 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things jump out immediately. The suburb average of $20,658 is extraordinarily high — nearly six times the national average — which signals that some properties in Warburton are attracting extremely steep premiums, likely due to severe bushfire risk classifications, high rebuild costs, or a combination of both. The median of $6,253 is a more representative figure for a typical Warburton property, and this quote sits well below even that marker.

Compared to the broader Victorian state average of $3,000/year, this quote is broadly in line, though slightly above. Against the national average of $5,347, it's actually quite competitive — roughly 34% cheaper.

The wide spread between Warburton's 25th and 75th percentiles ($4,911 to $11,225) underscores just how variable premiums are in this area. Small differences in a property's bushfire risk rating, construction type, or proximity to water courses can dramatically shift what insurers charge.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining through an insurance lens:

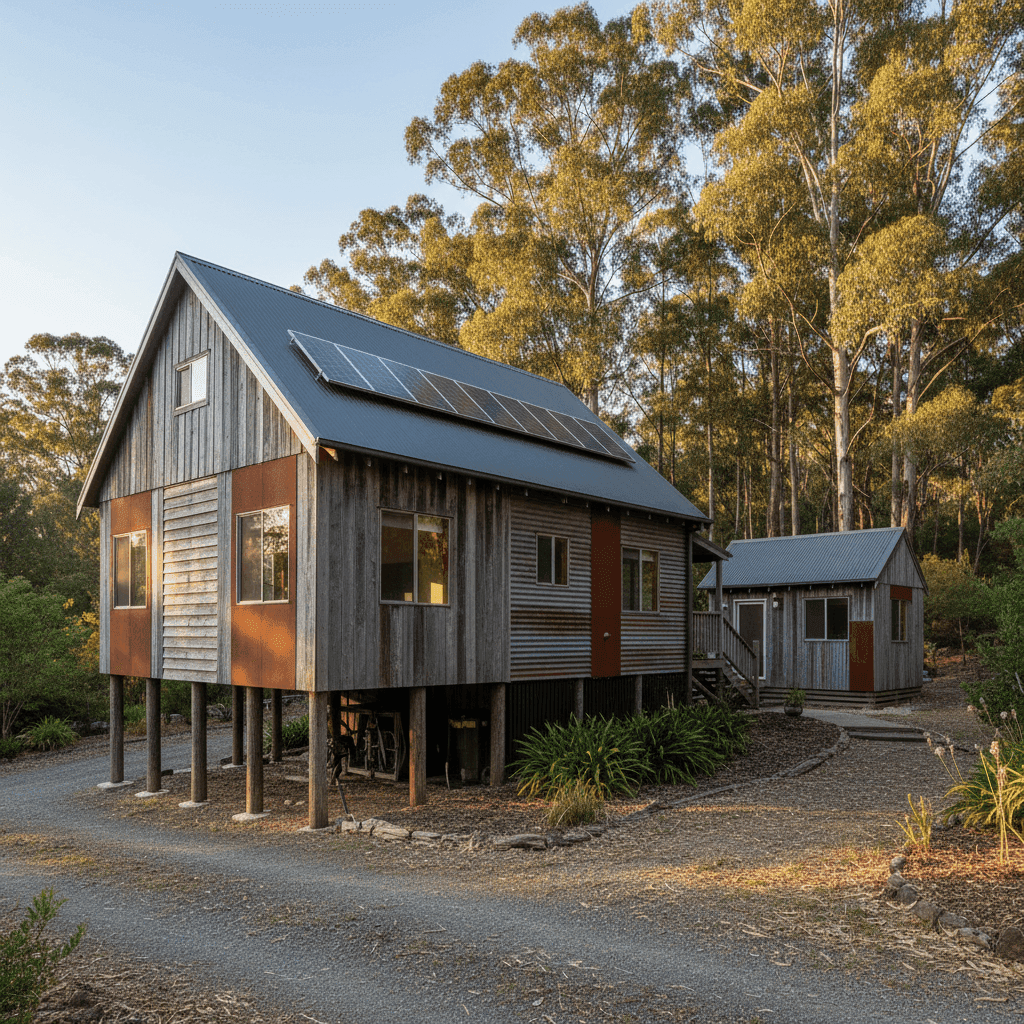

Age and Construction (Built 1950) At over 70 years old, this home predates modern building codes by decades. Older homes can be more expensive to insure due to the cost of sourcing period-appropriate materials and the likelihood of outdated wiring, plumbing, or structural elements. However, the steel/Colorbond roof is a significant positive — it's fire-resistant, durable, and far less susceptible to ember attack than older corrugated iron or timber shingles.

Stump Foundation and Elevated Design The home sits on stumps and is elevated by less than one metre. This style of construction is common in older Victorian homes and offers some natural ventilation benefits, but stumps can deteriorate over time and may require inspection and replacement. From an insurance perspective, the slight elevation can offer modest protection against surface water flooding.

External Walls Listed as "Other" Non-standard wall construction materials can sometimes attract higher premiums, as they may be harder or more costly to repair or replace. It's worth confirming with your insurer exactly how they classify and price this construction type.

Solar Panels The presence of solar panels adds to the insured value of the property. Panels are generally covered under building insurance, but it's worth verifying that your sum insured of $659,000 adequately accounts for their replacement cost, particularly as panel and inverter prices have shifted considerably in recent years.

Ducted Climate Control and Granny Flat Ducted climate control systems are a meaningful addition to rebuild cost calculations. Similarly, the granny flat on the property adds both value and complexity — homeowners should confirm with their insurer whether the granny flat's structure and any contents within it are explicitly covered under the policy.

Carpet Flooring and Standard Fittings Carpet throughout and standard-grade fittings suggest a mid-range contents and fit-out value, which aligns with the relatively modest $30,000 contents sum insured. Homeowners should periodically review this figure, as contents values can creep up over time.

---

Tips for Homeowners in Warburton

1. Review Your Bushfire Preparedness Annually Warburton sits in a high bushfire risk zone. Insurers assess Bushfire Attack Level (BAL) ratings when pricing premiums, and properties with active ember guards, maintained vegetation clearance, and compliant construction may attract more favourable terms. Check your property's BAL rating and ensure your home meets current standards.

2. Confirm Your Granny Flat Is Fully Covered Many standard home insurance policies have specific conditions around secondary dwellings. Make sure your insurer explicitly covers the granny flat — both the structure and any liability associated with it, especially if it's rented out.

3. Reassess Your Sum Insured Regularly Building costs in regional Victoria have risen sharply. A home built in 1950 may have a deceptively low market value but a high rebuild cost due to labour, materials, and compliance with modern building codes. Use an independent building cost calculator or speak to a quantity surveyor to validate your $659,000 sum insured.

4. Weigh Up the $5,000 Excess Carefully A high excess keeps your premium down, but it means you're effectively self-insuring for anything under that threshold. Consider whether you have the financial buffer to cover a $5,000 out-of-pocket expense in the event of a claim — if not, it may be worth requesting quotes with a lower excess to compare the premium difference.

---

Compare Your Options with CoverClub

Whether you're renewing your existing policy or shopping for the first time, it pays to compare. Insurance pricing in Warburton varies enormously — as the data above clearly shows — and the difference between the cheapest and most expensive quotes in this suburb can run to tens of thousands of dollars per year. Get a home insurance quote through CoverClub to see how your property stacks up and make sure you're not paying more than you need to.